Nvidia due for correction, 3M at a 10-year low

And other opportunities in the current stock market

Let’s be clear. 90% of my investing gains are made by investing regularly in the S&P 500. I’m not an expert, not a trader, I just like looking at data, finding patterns, and analyzing complex systems. That’s why I like the stock market.

I don’t execute 90% of the ideas I have. I look at the scenarios play out, and when it doesn’t go like I said I think to myself “Phew, good thing I didn’t bet on that idea”. When it does go as I said, I think to myself “Damn it, I could have made a 40% return on this, why didn’t I do it!”. And the answer to the question “Why didn’t I do it?” is always the same: the ratio between the amount of certainty of the event happening and the amount of money I stand to lose if I’m wrong is just not good enough. Of course, an investment is only lost once you sell, and you can always hold onto it until the stock recovers. But I try to only do long-term investing in the S&P 500, the rest is short to medium-term trades (usually month to month).

In this article, I want to present you with some of my latest investment ideas. Again, I am not an expert, none of this should be considered investment advice, most traders lose money. I also don’t look a lot at fundamentals, which many investors will tell you is a big no-no. I just gather data from the internet, sometimes run it through my little Python scripts, and make “informed” decisions based on that. I also really like patterns because human behaviour is predictable, and people on the stock market (human brains) tend to often react the same way to the same patterns. That being said, at the end of the day, investing is still gambling.

Idea #1 — 3M, because it’s at a 10-year low and has a 6% dividend yield

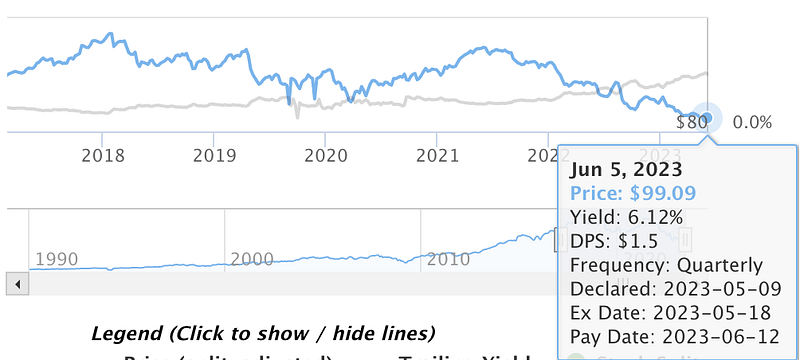

A dividend king is a stock with 50 or more consecutive years of dividend increases. In the case of 3M, they’ve raised their dividend every year for 66 years, and due to the falling stock price, the yield is very attractive right now.

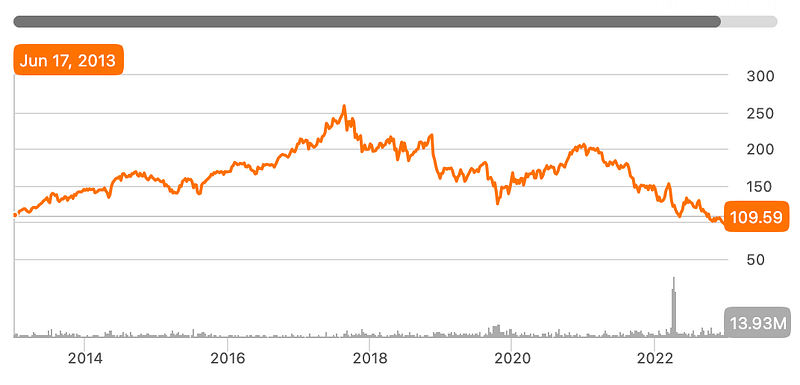

On top of that, 3M is currently trading at a decade low and dropped all the way to $93 in May.

You can find higher-yielding, cheaper stocks, but you won’t find higher yields without greater risk than 3M currently brings to the table. This is a solid company that is over 100 years old, owns more than 100,000 patents and has been part of the S&P 500 since the inception of the index.

The idea here is that even if the stock drops substantially, you’ll still be making passive income with the dividends. Plus, the current $100 stock price is a good “mental barrier” for investors, it could be a great support to pick back up from:

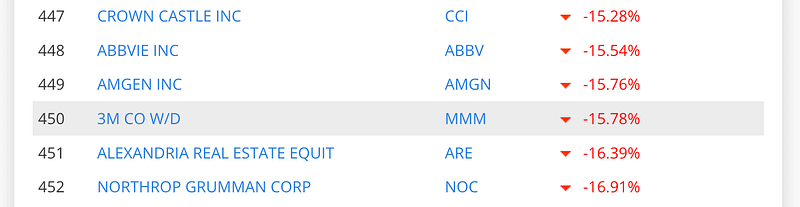

It’s also worth noting that 3M is currently one of the top-losing companies in the S&P 500. It’s down 18% since the beginning of the year, the 464th best-performing stock of the index (that’s very bad). Tables eventually turn, so we could be looking at a recovery in the near future.

The main con to investing in this stock is the lawsuits and legal woes the company is currently going through.

The biggest of these challenges is the class action lawsuit being levied by former users of its earplugs.

More than 200,000 veterans are suing the 3M subsidiary that makes them, claiming its product failed to prevent the noise-related hearing loss they were supposed to prevent. The matter could cost the company billions of dollars when all is said and done. — Source

3M is trying to avoid the legal liability of the parent company by declaring bankruptcy for the subsidiary that makes the earplugs, but this won’t necessarily work.

If the verdict ends up being losing for the company, it won’t necessarily go bankrupt, but the stock will definitely suffer, which would be a once in a decades opportunity to buy a great company at a discount.

Idea #2: Nvidia, because it’s overvalued

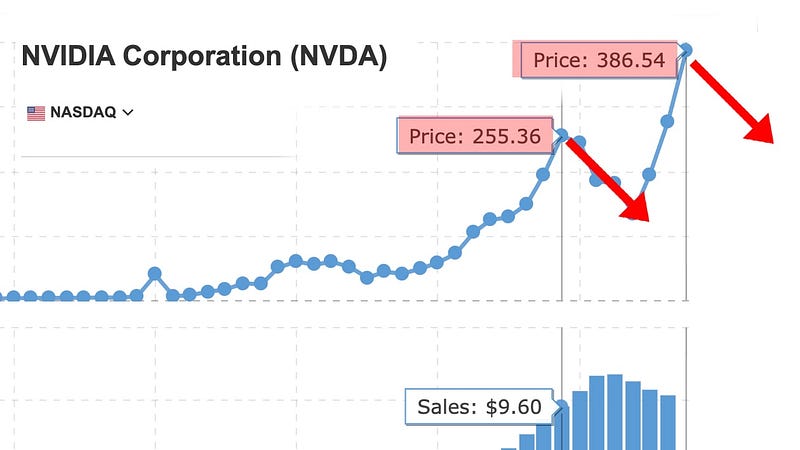

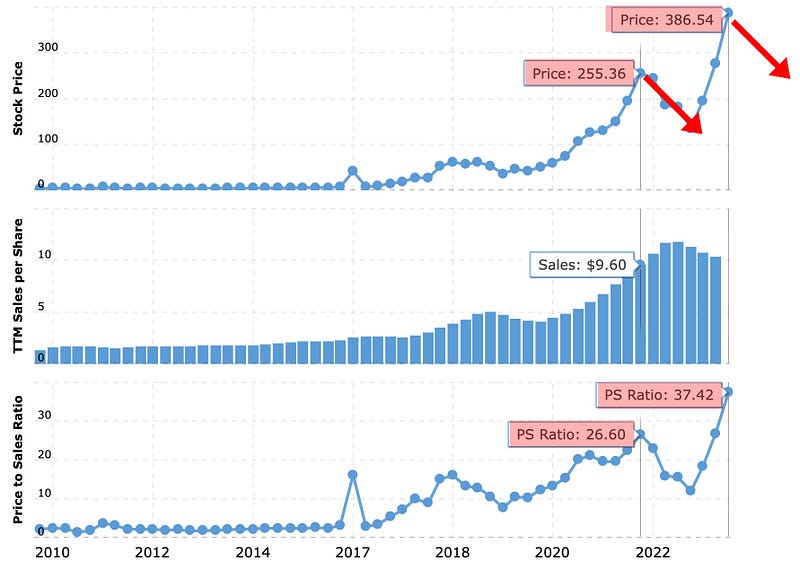

The recent surge in the popularity of AI has sent a lot of tech stocks soaring. Nvidia in particular has reached incredible heights because it has emerged as the biggest player in the field of AI chip production and research. The company briefly reached a $1 trillion valuation when its stock passed the $400 mark at the end of May, and it has lost almost 7% since then. Many say this is just the beginning of a big correction, with the company being aggressively overvalued.

The idea here is to wait for the value to drop and buy the dip. The company currently has a price-to-sales ratio of nearly 38, which is way too high. The only way to keep up with those metrics is to post better-than-expected sales result quarter after quarter, and the slightest decrease in performance will most likely send the stock spiraling down at least for a little bit. Even without a decrease in sales, the stock dropped in Q4 2022 when the P/S ratio hit 26.6:

Nvidia is also the top-performing company in the S&P 500 since the beginning of the year, with a 164% year-to-date return, another sign that the stock is red hot and investors might be getting ahead of themselves.

The biggest drop in price for the stock since the pandemic was in April 2022 when it lost 32%. I think a good entry point for Nvidia would be anywhere at or below a 20% drop, either month-to-month or more spread out.

Idea #3: Brookfield Asset Management, because growth

Brookfield Asset Management is part of Brookfield Corportation, a Canadian multinational company that is one of the world’s largest alternative investment management companies with over $800 billion of assets under management in 2023. One of the main ways the company makes money is through management fees, and that’s key to growth predictions.

The company’s investors have committed $37 billion of capital not currently earning management fees. This capital represents $370 million of future fee-earning revenue for the company as it deploys it into new investments. — Source

More revenue means happy investors and happy investors means rising stock price. BAM is also targeting to double the size of its business over the next five years, with fee-bearing capital growing to ~$1 trillion.

Example of a missed opportunity: the Google Bard panic sell

I thought it would be useful to include an example of a situation where I was 100% right but still didn’t execute, just to illustrate how rarely I actually follow my gut on the stock market. Again, 90% (if not more) of my gains are made with simple DCA investing in the S&P 500.

Back in February 2023, Google’s newly released Bard AI made a factual mistake during its first demo to the public. This blunder sent the stock spiraling down, and GOOGL lost almost 9% that month. I was 99% sure it was going to pick up again, for 3 main reasons:

- The AI wave was just getting started, so Google was going to have plenty of time to recover and surf the wave too.

- Tech stocks were and still are red hot, and the S&P 500 was starting the year in the green for the first time since 2021, so there was good momentum.

- Most importantly, this was a classic example of an irrational panic sell, and the result was an amazing tech stock at a discount. The drop had already wiped out $100 billion off Google’s market cap and was unlikely to continue.

I knew all this and really hesitated, yet I didn’t buy it. The stock is up almost 40% since the AI blunder. I still profited from the momentum through my stake in my S&P 500 ETF, but not as much as I could have.

Thanks for reading! If you want more investing ideas like this, I’m thinking of starting a newsletter on the topic, you can sign up here!

Subscribe to DDIntel Here.

Visit our website here: https://www.datadriveninvestor.com

Join our network here: https://datadriveninvestor.com/collaborate