2023 Stock Market Preview (And Review Of 2022)

Look back for clues on how to move forward

(Not intended to be investment advice. Opinions are my own.)

In order to guess at where markets are headed, it helps to look back. Over longer periods of time stock markets, are driven by narratives and changing expectations around those narratives. Thinking about which narratives make sense and more importantly which ones are overpriced (and underpriced) into the market is critical to being a decent long-term investor. To help with that, one of my 2023 resolutions it is to put out (hopefully) insightful data on a regular basis. Today, let’s start off by looking at what happened in 2022 and what that might mean for where we are headed.

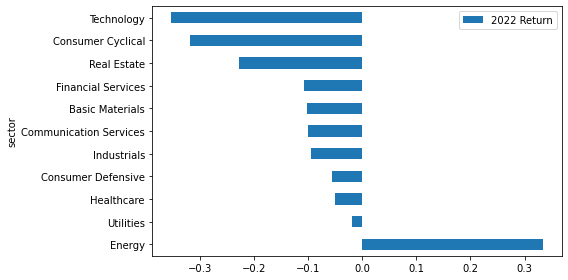

2022 was a year where all the things that had worked in 2020 and 2021 suddenly stopped working thanks to high inflation and rising interest rates. Looking at the overall sector performance of stocks traded on the NYSE and NASDAQ (see plot below), all sectors had negative returns except for energy.

And as expected during a period of monetary tightening and rising risk aversion, defensive sectors (e.g. healthcare, consumer staples) outperformed riskier ones (e.g. tech, consumer cyclicals). The exception to this rule was energy. As of the start of 2022, the energy sector had yet to recover its pre-pandemic peak (it was arguably cheap on a relative basis), but that all changed with Russia’s invasion of Ukraine. The war, which compromised a significant portion of the world’s energy and grain supply, pushed commodity prices up massively (especially energy related ones), creating massive windfalls for producers.

Baby thrown out with the bath water

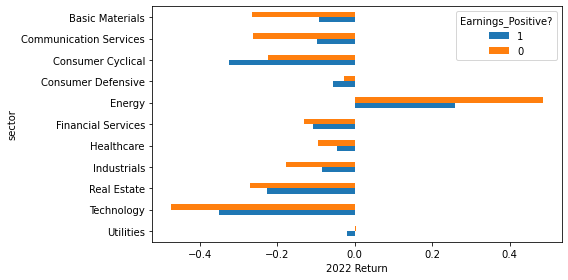

If we split each sector between companies that are currently profitable and ones that are not, we can take a look at whether the selloff was isolated to the lower quality, unprofitable companies in a given sector or whether it was broad-based (see picture below).

On average profitable companies fared a bit better than their unprofitable peers (with the exception of both consumer sectors and financial services). But not by much — in sectors like tech and consumer cyclicals, investors hit the sell button on everything regardless of profitability. For example, even profitable tech companies were down on average 35%.

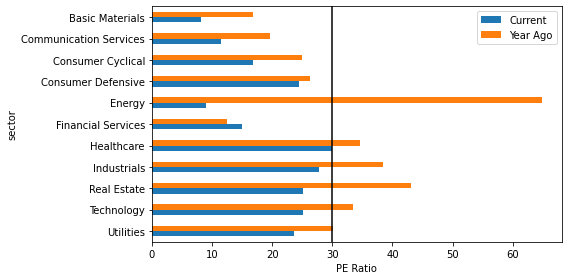

Part of the reason was lofty valuations (see picture below). At the start of 2022, stocks across most sectors were trading at very rich valuations, with many sectors sporting average PE ratios of 30 or more. That’s pretty high.

Energy is the exception — the energy sector’s year ago PE ratio appears so high because its earnings were extremely low in 2021. In 2022, the share prices of energy companies increased, but their profits increased even more, hence the drop in PE ratio. However for all the other sectors, valuations came down primarily due to share prices declining.

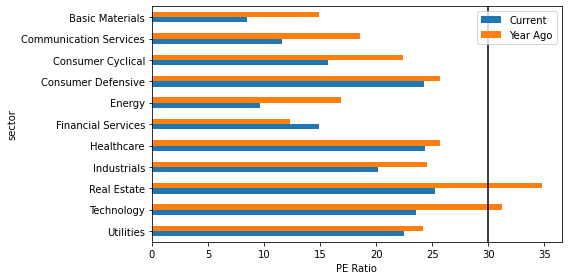

If we look at the valuations of just the profitable companies, we see a very similar picture (except for energy). The similarity between the plot below and the one previous implies that investors wanted out of stocks regardless of profitability.

Perhaps investors freaked out because interest rates were finally going up. Or perhaps investors expected even the profitable companies to suffer significantly during a recession. Regardless, the fact that they threw the baby out with the bath water creates opportunities for level-headed investors with a long-term horizon. High quality companies are significantly cheaper than they were — meaning their expected returns going forward should be significantly higher as well.