Startups: Stop Waiting for the Return of 2021 and Get Real

Early-stage investments are way down in 2023. What you need to do if you want investment.

Although the final totals for venture investment for the year won’t be published for a while, there’s no doubt 2023 was a painfully slow year.

According to a Crunchbase report, seed and angel funding in 3Q23 was down 27% in dollars from the previous year. The number of deals fell even more dramatically by over 40%. Dollars and deals invested have continued to decline every quarter since the beginning of 2022.

Outside of life sciences, the startup landscape was a wasteland for both founders and investors.

In a typical year, I invest in 6–8 startups. In 2023, I invested in 2. The two angel groups I’m involved in together usually invest in around 15 companies per year. This year, we invested in 7, almost all in life sciences.

In my portfolio of around 150 investments, it’s been more than a year and half since I’ve had a positive exit. That means any new investments have to come out of my retirement savings instead of reinvesting the winnings. The bar is obviously higher now than when I’m playing with house money.

However, I’m ready to invest in the right opportunities. My angel groups have funds sitting in the bank ready to deploy. Nevertheless, it’s hard to find anything we want to invest in.

2021 Was a Bubble. It’s Over.

Yes, I hear you. Tens of thousands of founders waving their arms, screaming as loud as they can, “Over here, look at us, invest in us, we’re ready to take your money.”

I hate to break it to you, but most of you are not ready. The ones that are ready are not offering attractive terms.

In 2021, the stock market was on a tear. The SPAC bubble meant any company could go public with an absurd valuation. NFTs and Web3 made random doodles worth millions.

Companies were getting acquired or going public at crazy valuations. Every exit meant hundreds of millions of dollars to reinvest in new startups. Big companies were setting up billions dollar venture investing arms. Retirement funds and family offices were throwing money at venture capital firms. Every fresh MBA was raising their own $100M venture fund to focus on impact investing.

With all that cash looking for startups to invest in, FOMO was the word of the year. Valuations didn’t matter because there’d be someone willing to acquire the company at 10x higher. Founders could set outrageous terms and still find investors willing to write cheques.

We invested in organic ciders, protein bars, AR/VR, and SaaS for anything and everything. We invested in beer pouring machines, garden hose nozzles, and space trash tracking systems. We invested in good ideas with inexperienced founders and great founders with no idea of their market. We invested in scientists with no business skills and businesspeople building hardtech products without a CTO.

We invested millions in pre-revenue startups at $20M valuations. We invested in startups with no boards. We invested in uncapped SAFEs and convertible notes. Because if we didn’t invest at those terms, somebody else would. If we wanted in, we had to hold our nose, swallow hard, and sign the docusign.

Mostly we swallowed our skepticism and accepted those claims of billion dollar opportunities and $100M in revenues within 5 years. For garden hose nozzles. It didn’t happen. It was a wild, drunken party, and investors lost our shirts.

2021 was a bubble. 2021 isn’t coming back. Welcome to 2024.

2021 is Over. Founders Haven’t Gotten the Memo

The startup party is over. Investors have sobered up. We won’t invest again in a revolution in garden hoses. Or even a new roof tiles with a $20M pre-money valuation.

The problem is founders don’t seem to have gotten the memo. We’re still being pitched on $20M valuations for pre-revenue startups, or worse — no cap at all. We’re still being asked to invest $10M in companies with no chance of reaching more than $5M a year in revenues. We’re still being pitched companies without an investor on the board. And founders are complaining they can’t find funding.

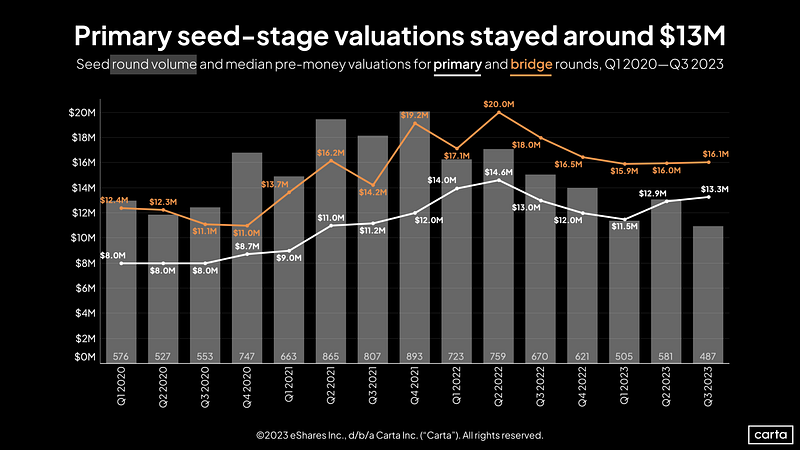

Seed-stage valuations rose from $8.0M at the beginning of 2020 to $14.6M in 2Q22. They’re holding steady now at around $13M. That’s great for the startups that can get funding, but at that valuation, most can’t. Valuations are staying high but the number of deals at that price is tanking.

Not only do early-stage valuations need to fall back to $8.0M, they need to fall even lower. Interest rates are high now, and the path to exit is hard and long. Investors are skittish now.

If you want to tempt us into investing, terms need to be attractive. Average valuations need to go back to $6M, which is where they were before the covid bubble. If you think you’re worth $13M, you’re probably worth $6M now.

In 2010–2012, after the financial crisis, there were deals to be had in venture investing as well as real-estate. Investors were offered not only attractive valuations but additional protections including warrant coverage and liquidation preferences. I’m not seeing any of that yet. Which is why few deals are getting done.

Instead, startups that can are doing small “bridge” raises, extending the terms of their previous rounds. The rest are holding on for dear life, hoping for good times to return.

The party is over. The good times aren’t coming back. That was a bubble; it’s gone, never to return. Valuations and terms in 2020–2022 were an anomaly. It’s time to get real.

What to do if you want funding

If you want to get funded here’s what to do:

Forget that 2020–2022 ever happened. Stop comparing yourself to other startups from that time, or even to your own last round.

Get back to fundamentals. If you don’t have revenues yet or at least serious customer traction, scrimp and save and do everything you can to get it before looking for investment. Apply for grants, win awards, do consulting work to stay afloat.

If you absolutely need investment, focus on friends and family and people in your network. Go back to existing investors. If they won’t support you, don’t expect strangers to.

Offer attractive valuation. Lower valuations to start with. Assume the average startup valuation is $6M and set your own expectations accordingly.

Set Investor-friendly terms. Offer preferred equity instead of a SAFE or convertible note. Give investors a seat on the board, along with information and pro-rata rights, and liquidation preferences on an early sale.

Show us how we make money. You’re selling stock in your business — show us why that’s a good investment. How will you break into a crowded market with entrenched competition? How much money will you need? How big is the market opportunity really? And be honest. If you’re successful, is there an exit with a big return for investors?

This one can’t fail. 90% of our investments fail. Don’t tell us why you’re the one that can succeed. Show us why you’re the one that can’t possibly fail.

Investors are still ready and willing to invest, but only if it makes financial sense. Unlike 2021, founders need to show us a good deal. Otherwise, we’re content to keep our cash in t-bills earning 5.5% risk free.