Reacting To This Redditor’s $93K Dividend Portfolio

What I would do if I were him.

In my last month of writing on Medium, I learned that one of the best ways to develop ideas is by reading other people’s articles.

The different perspectives you read are fantastic and often lead to new revelations you have not thought of before.

Due to the tremendous success of bouncing ideas off other people, I decided to test the same principle when investing by spending more time reading about other people’s investing strategies and portfolios.

As I read, a lightbulb went off in my head.

What if I reacted to some of these strategies and practiced what I learned? Hence, I decided to write this article.

Today, I’ll look at a Redditor’s $93,500 Roth IRA and talk about what I would do if I were in his shoes.

A $93K Dividend Portfolio

First, background information.

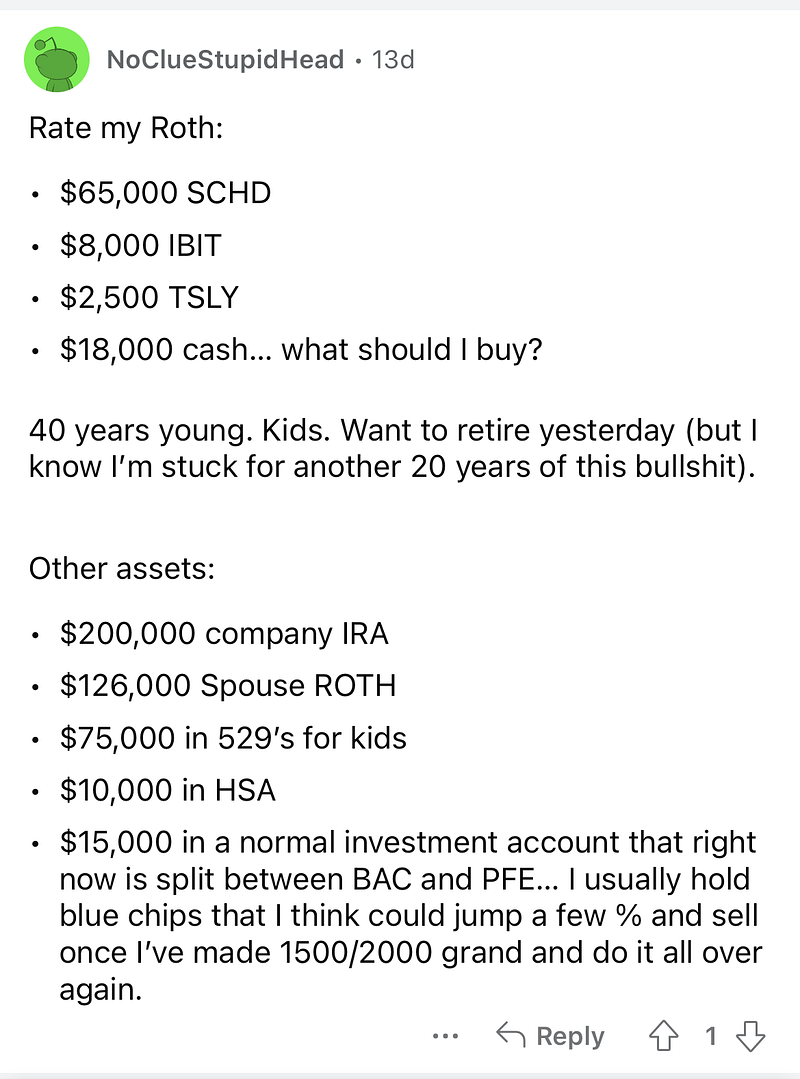

The Redditor is a married 40-year-old with kids and has $93,500 in his Roth IRA.

His holdings consist of:

- $65,000 SCHD — Schwab U.S. Dividend Equity ETF

- $8,000 IBIT — iShares Bitcoin Trust ETF

- $2,500 TSLY — YieldMax TSLA Option Income Strategy ETF

- $18,000 in cash

He also has $200k in a company IRA, $75k in 529 plans, $10k in a HSA, and $15k in a non-tax-advantaged investment account where he specifies a strategy of buy-and-sell blue-chip stocks.

That non-tax-advantaged account is currently split between Bank of America (BAC) and Pfizer (PFE). His spouse also has $126k in another Roth account.

I’ve included a screenshot of the post and a link to it in the caption:

Breaking Down His Holdings and What I Would Do

Since the post is in a dividend thread, I have assumed that dividend investing is the Redditor’s goal. Holding more than 60% of his portfolio’s money in SCHD is also a good indicator.

Let’s break down each holding and discuss what I would do if I were him.

SCHD — Hold and Reinvest

I am a big fan of SCHD. This is one of the best ETFs to buy if you want consistent dividend growth over the long term.

In fact, if you put $100k in SCHD in 2012, you would have over $400k today and earn more than $10k per year from dividends.

SCHD’s low fees and many holdings make it a phenomenal choice as a core holding.

I don’t mind putting $65k out of $93k in SCHD and would continue reinvesting dividends and about half of the new contributions into the fund.

IBIT — Don’t Mind a Little Crypto

The second holding in this Redditor’s portfolio is IBIT. This is iShares Bitcoin ETF, which gives the Redditor exposure to cryptocurrency.

While I personally wouldn’t buy into crypto, I don’t mind this purchase.

I don’t dabble in cryptocurrency mainly because I don’t know enough. I don’t have an opinion on whether cryptos would go up or down.

This sentiment would change if I spent time researching, but that’s how things are now.

For the Redditor, however, as long as he believes in Bitcoin and its prospects, I have no problems with this purchase.

It’s honestly a great holding to have, considering that he is still 40 years old.

If he retires at the standard age of 65, he still has 25 years to go. More growth in this portfolio would be beneficial.

TSLY — Sell For Your Own Good

The first two investments have been good so far, but the third just doesn’t make sense.

If I were this Redditor, I would sell out of TSLY. I wrote an article in June last year talking about why I stay away from TSLY:

In short, finding a place for the fund isn’t easy.

Tesla (TSLA) offers much better growth, and there are far better alternatives for income.

TSLY’s current yield of 86.91% is enticing, but it’s bait.

The high yield is coupled with long-term NAV depletion and eroding distributions. This is not a fund you want to hold long-term.

Unless the Redditor makes short-term plays and bets using TSLY, I would get out of this fund.

$18k In Cash — What To Do?

For the final piece of the portfolio, things get interesting. The Redditor holds $18k in cash and asks people what he should buy.

Here’s what I would do.

First, I would trim my cash position to about 2% of the portfolio. This means leaving aside about $1,870.

Half of that will go to HIGH, the Simplify Enhanced Income ETF.

This fund holds short-term T-bills and sells call and put spreads on various stocks and bonds. It’s a cash equivalent that allows you to put your money to work with little to no volatility.

The idea is to have some cash on hand to buy dips on other holdings like SCHD and IBIT.

If the Redditor doesn’t plan to follow any funds or stocks, then there is merit in investing everything and leaving no cash in the portfolio.

Regardless, after setting aside the cash, there’s about 16k left (18k if we sell the TSLY position).

My next few picks would include the following:

- QQQ — Invesco QQQ Trust ETF or JEPQ — JPMorgan Nasdaq Equity Premium Income ETF

- TLTW — iShares 20+ Year Treasury Bond Buywrite Strategy ETF, HYGW — iShares High Yield Corporate Bond Buywrite Strategy ETF, and/or LQDW — iShares Investment Grade Corporate Bond Buywrite Strategy ETF

- O — Realty Income Corporation

Assuming we have $18k left, $10k would go into QQQ or JEPQ, $4k into one or all three of the iShares bond buy-write funds, and $4k into O.

First, putting a good amount of money into QQQ or JEPQ would diversify the portfolio into technology and give the portfolio more opportunities to grow.

Both are good, but I’m leaning toward JEPQ to retain the dividend theme with JEPQ’s covered call distributions.

Next, we have the iShares bond buy-writes. I covered two of these funds already, and they all have similar benefits.

I’d go for the iShares bond buy-writes if the Redditor wants something super high-yielding. They’ll give exposure to bonds, and I also don’t mind the covered calls, as bonds don’t see the same capital appreciation as equities over the long term.

Finally, I have O or any other good REIT.

SCHD purposely excludes REITs, which include many companies that have consistently and reliably grown dividend payments over a long time.

An investment like O would be another good way to diversify while retaining the theme of dividends.

What Would You Do?

Of course, it’s difficult to say if the changes above are the right choice for this Redditor as I don’t know him personally or enough about his circumstances.

It is what I would do, however, if I had $93k in a Roth IRA and wanted to one day live off of dividends.

What would you do? Let me know in the comments below!

Want more investment news and analysis? Seeking Alpha is my first stop for all my research. Take a look at the Seeking Alpha platform here.

Financial Disclaimer: The views in this article are the author’s personal views. This commentary is provided for general informational purposes only. It does not constitute financial, investment, tax, legal, or accounting advice, nor does it constitute an offer or solicitation to buy or sell any securities referred to. Individual circumstances and current events are critical to sound investment planning; anyone wishing to act on this article should consult with their advisor. The information provided in this article has been obtained from sources believed to be reliable and is believed to be accurate at the time of publishing, but we do not represent that it is accurate or complete, and it should not be relied upon as such. Investing in stocks, bonds, exchange-traded funds, mutual funds, and money market funds involves the risk of loss. Their values change frequently, and past performance may not be repeated.

Affiliate Link Disclosure: You may assume all links in this article are affiliate links. If you purchase any product or service through the link, I may be compensated at no extra cost to you.

Visit us at DataDrivenInvestor.com

Subscribe to DDIntel here.

Have a unique story to share? Submit to DDIntel here.

Join our creator ecosystem here.

DDIntel captures the more notable pieces from our main site and our popular DDI Medium publication. Check us out for more insightful work from our community.

DDI Official Telegram Channel: https://t.me/+tafUp6ecEys4YjQ1