Rachel Bought Her House One Year After Jackie — And the Results Were Unbelievably Worse

Part 1. What could have made such a difference? Exactly how different was it for for the two women? And who ended up being happy for Rachel?

Related

• 4 Things Smart Homebuyers Do If Their Mortgage Rate Is Over 5% • Part 2: How Can Rachel Avoid Getting Totally Screwed by Her 7% Mortgage Interest Rate? • What Do U.S. Housing Price Predictions for 2023–2024 Look Like and Why? • Q&A on Housing Price Predictions for 2023 and 2024 • Why Are Chinese People Smarter About Mortgages than Americans? • Is the Stock Market Really in a Bear Market? Maybe. Maybe Not. • When Is a Stock Market Crash Not Really a Stock Market Crash? • Mortgage Borrowing for YOUR Benefit: 1. Pay Less Interest 2. Interest Savings Over First 5 Years

Recent

• When Did this Safeway in San Francisco Turn Into Dangerway? • How the Al Dente App Eliminates the MacBook Battery Life Problem • Savvy MBA: Which of the 4 Apple iPhone 14 Models Is the Smart Buy? • The Social Contract Broke in the U.S. Years Later Than in Japan • The Ultimate Question for Starting a Conversation Between Two People

Potential to Change the Way You Think

• Life Expectancy vs. Healthcare Costs in the U.S. and Other Countries • Why Should You Vote “Blue No Matter Who” When Centrist Dems Never Play to Win? • Six Behavioral Barriers That Prevent You from Changing the Status Quo — Part 5. Smart Man’s Disease

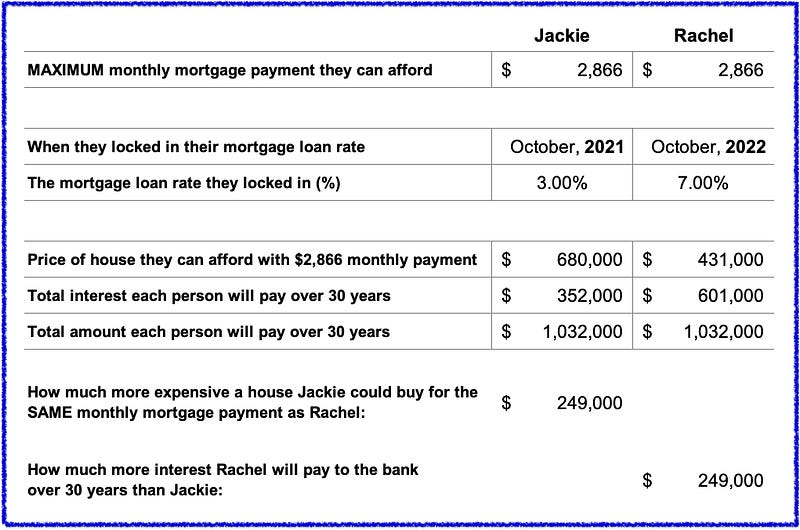

Jackie bought her house a year ago in early October 2021.

And Rachel just bought her house last week in early October 2022 — almost exactly one year after Jackie.

Coincidentally, each woman could only afford to spend $2,866 per month on their mortgage payment.

Not a penny more.

Yes, Rachel is making a little bit more money this year salary-wise, but inflation for food, gas, the used car she had to buy, etc. has more than eaten up her small salary bump. She is actually behind where she was last year. So $2,866 per month for a mortgage payment is actually more of a stretch today for Rachel than it was for Jackie last year.

Same monthly payment, and they’re buying their homes only 12 months apart from each other.

Probably worked out just about the same for each woman, right?

Wrong.

The results for the two women could not be more different.

Jackie was lucky enough to have gotten a 30-year fixed-rate mortgage at 3.00%.

It meant that Jackie’s $2,866 monthly payment would be enough to purchase a $680,000 house.

And that’s exactly what Jackie did back in October 2021.

She closed on a $680,000 dream house and moved in shortly thereafter.

Fast-forward to October 2022, and Rachel is hoping to buy her dream house.

She was really excited for her friend, Jackie the year before when Jackie bought her dream house.

Now it’s Rachel’s turn.

Except . . . it’s not.

Interest rates in early October 2022 were around the 7.00% level versus the 3.00% level when Jackie bought her house a year earlier.

And that means that instead of her $2,866 monthly payment buying her a $680,000 dream house, the 7.00% interest rate and her $2,866 payments each month will only finance a $431,000 house!

But wait, that’s not the whole story.

Over the past 12 months, average house prices in the U.S. have gone up by probably at least 10%.

(The October numbers aren’t out yet, but based on price increases through Q2, it seems likely that the year-over-year 3rd Quarter increase will be at least 10%.)

So that means that Rachel’s effective buying power is an additional 10% less beyond what we have already calculated.

While Rachel will still be paying $2,866 per month, and she will still be buying a house with a price tag of $431,000, what she will be getting is a house worth 10% less, or about $388,000.

When you add everything together, Rachel is getting a house worth about 43% less than the one that Jackie bought just 12 months earlier for the same monthly mortgage payment.

Yikes!

Is there ANY good news at all in this?

Well, actually, there is.

Sort of.

Because Rachel has a 7.00% mortgage interest rate, that means that she will be paying her mortgage lending institution $249,000 more than Jackie will over 30 years.

So Rachel’s bank is really, really, really happy to be doing business with her.

But wait — why should the bank care one way or the other what interest rate Rachel is getting?

It’s not as though the bank has a “personal interest” in home borrowers having to borrow money at higher interest rates . . .

. . . is it?

Yeah, actually, the bank DOES have a huge financial interest in having their borrowers have to pay as high an interest rate as possible.

In Rachel’s case, they are making an extra $249,000 off of just her one home over the course of the 30 years.

So all the extra interest money from all of the other “Rachel’s” out there buying homes in October 2022 means that banker bonuses are going to be running at potentially historical highs.

It’s not just going to be a good time to be a banker, it’s going to be an effing great time to be a banker!

So the bankers have a message they would sincerely like to send all of the Rachel’s out there:

“Thank you, Rachel . . . and BOHICA!”

Related

• 4 Things Smart Homebuyers Do If Their Mortgage Rate Is Over 5% • Part 2: How Can Rachel Avoid Getting Totally Screwed by Her 7% Mortgage Interest Rate? • What Do U.S. Housing Price Predictions for 2023–2024 Look Like and Why? • Q&A on Housing Price Predictions for 2023 and 2024 • Why Are Chinese People Smarter About Mortgages than Americans? • Is the Stock Market Really in a Bear Market? Maybe. Maybe Not. • When Is a Stock Market Crash Not Really a Stock Market Crash? • Mortgage Borrowing for YOUR Benefit: 1. Pay Less Interest 2. Interest Savings Over First 5 Years

Recent

• When Did this Safeway in San Francisco Turn Into Dangerway? • How the Al Dente App Eliminates the MacBook Battery Life Problem • Savvy MBA: Which of the 4 Apple iPhone 14 Models Is the Smart Buy? • The Social Contract Broke in the U.S. Years Later Than in Japan • The Ultimate Question for Starting a Conversation Between Two People

Potential to Change the Way You Think

• Life Expectancy vs. Healthcare Costs in the U.S. and Other Countries • Why Should You Vote “Blue No Matter Who” When Centrist Dems Never Play to Win? • Six Behavioral Barriers That Prevent You from Changing the Status Quo — Part 5. Smart Man’s Disease

Want unlimited access to all Medium articles? Become a member!

Would you like me to cover a topic? Please post suggestions in the comments, and I’ll use your input to help prioritize my writing and research.

If you appreciate my writing, please share it on social media.

Again, thank you for reading, subscribing, clapping, and sharing — your time and attention are deeply appreciated!