Quantitative Easing: An Introduction

Economic Theory Explained Simply

In this article, together, we will learn what Quantitative Easing is, and how all the different parts of the economy come together for it to work. Before we can explore quantitative easing, we first need to understand what a Central Bank is and what its functions are.

What is a Central Bank?

A Central Bank (CB) is an independent government institution, which is responsible for managing the overall health of the economy. The CB’s primary responsibilities are:

- Managing the country’s currency

- Money Supply in the economy

- Setting Interest Rates

- Regulating commercial banking

- Lender of last resort

Let us take a closer look at what all of these responsibilities mean.

Managing the country’s currency

Have you ever wondered where does the money come from? Yes, I’m talking about the physical notes and coins that you use every day. Well, the CB of each country is responsible for the design, creation, distribution, and management of the currency.

Management of the currency primarily refers to the central bank ensuring that the people have and continue to have confidence in the currency and its value. There are many ways to do that, and there many definitions of a currency (pegged, gold standard) and how its value is backed, but we will not be diving into that here.

Money Supply in the economy

Following suit from the ‘creation’ of the currency, the CB needs to figure out how much money is required in the economy. That is, how much money should be in circulation.

Too much or too little money available in circulation, and you might just end up with a severe problem in your hands for the overall economy, as money supply directly affects inflation.

Theoretically, the CB could print more or remove money from circulation to affect the money supply in the economy. In reality, and although this method has been tried historically, this is no longer a valid or practical use case (physical cash is not the only cash in the economy — deposits make up 97% of the money in the UK). The CB will mostly affect Money Supply by setting interest rates.

Setting Interest Rates

We are all aware of what interest rates are; when you deposit money at your bank, at the end of each month, you receive an interest payment based on some yearly (interest) rate. In other words, it is the amount of money someone is requesting to be paid to forego some liquidity.

So, how does the CB set interest rates?

As we have learned in ‘Flash Introduction to the Money Market,’ the inter-bank lending market is the Money Market (MM) where banks lend each other money for what is known as the inter-bank rate. The transfer of funds happens through all the different types of MM instruments that we have seen previously.

The CB is a crucial participant of the MM. With what is known as ‘Operational Standing Facilities,’ the CB allows banks to deposit or borrow funds (against high-quality collateral) at specified rates (known as Bank Rate). The difference between the deposit and borrow rate is often known as the ‘interest rate corridor.’ These rates act as a ceiling and a floor; banks would not want to lend at prices lower than they have borrowed (they would be losing money), and accordingly, the banks would not want to pay more interest than they are receiving.

Consequently, by changing the Bank rate, the CB can affect the Interest Rates.

Note: CBs also have a facility called Open Market Operations (OMO), where they engage in overnight repo trading with Banks to influence Market Rates if they diverge too far from the Bank Rate. Using the OMO, CBs can substantially smooth out day to day market rates.

So, how do interest rates affect the Money Supply?

Money creation in the modern economy primarily happens through the extension of loans. When a bank extends a loan to a consumer/business, that money then ends up as a deposit (new money!).

To destroy money in the economy, all you have to do is repay loans from deposits.¹ ²

As we discussed earlier in the article under ‘Money Supply In the Economy,’ the CB influences the money supply through interest rates. When the CB changes the Bank Rate, banks need to re-examine their profitability in terms of their loan extension practices. Keeping in mind that banks are constrained through regulatory requirements on reserves held and liquidity, by changing the Bank Rate, the CB is influencing the banking system in terms of extending loans or not.

Moreover, as Interest Rates change, consumers and businesses may decide to repay some or all of their debts.

¹: Although often introductory economic textbooks will talk about money creation through deposits driving loans, that is not what happens in reality. It is the opposite — it is loans that drive money creation through deposits.

²: Although consumers obtaining or repaying their loans is the most significant way to create/destroy money, it is not the only way. Buying and selling activity of assets within the banking sector (including the CB) will create or destroy money.

Regulating Commercial Banking

Central banks are responsible for regulating Commercial Banking on a significant number of items. Some of the critical elements are:

- CB is responsible for issuing banking licenses

- CB define the reserve requirements and then require the banks to follow it

- Define Capital-Adequacy requirements and monitor other risk measures

Lender of Last Resort

The CB is usually the Lender of Last Resort. That is, if a bank cannot obtain the necessary liquidity through the inter-bank market at any point, the central bank will step in and guarantee to provide it with the required funds.

Now that we have finally covered what a Central Bank is and what its different functions are, we are in a position to look into Quantitative Easing.

What is Quantitative Easing (QE)?

Quantitative easing is a tool that central banks can employ to inject money in the economy and consequently expand the money supply, with the ultimate goal of stimulating financial activity.

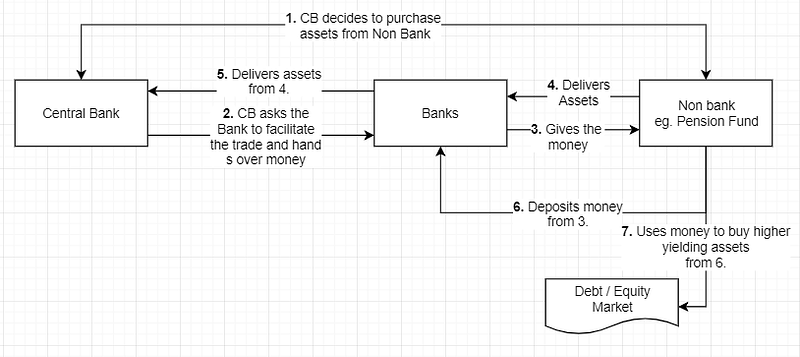

CBs use their unique ability to create money and then go in the market and participate in large asset purchases (mostly government bonds). CBs purchase these assets mainly from non-banks (such as pension funds or insurance companies) but use banks as an intermediary to help facilitate the deal.

Once the purchase deal goes through, the money ends up in the seller’s accounts as deposits. As part of their capital management practices, they will likely want to get rid off the excess cash. That implies that the sellers will then use this “new money deposits” to purchase higher-yielding assets from either the debt or equity markets. Consequently, this will raise the prices of the assets of these assets (due to increase demand), lowering the yields, implying that it then becomes cheaper for companies to raise funds, further leading to money creation and economic activity.

Note: When Interest Rates are already low, the CB is not in a position to lower them anymore. Therefore, the CB needs to employ a different way of increasing the money supply in the economy; Quantitative Easing.

When things do not go to plan

On the other hand, there is a possibility that the QE strategy of the CB may not go to plan. The scenario described above assumes that the sellers of the assets purchased by the CB will use the new funds to make further investments. However, there is a chance that they may use this money to settle existing loans, which would clearly ‘destroy’ money, rather than create more in the economy.

If you liked this article, you may also like:

Before you go, I often blog about finance and technology. If you want to stay up to date with my articles, don’t forget to follow me!