Pros and Cons: My Experience Earning Interest with BlockFi

Updated August 3rd, 2021

Now that we’re close to halfway into 2021, I thought it would be as good a time as any to look back at BlockFi’s slew of updated offerings to compare where they started off and how they stand now.

But first, let’s start here. For the last couple of years, I’ve been searching for ways to increase my passive income — stacking sats with a hands-off approach. That’s when I found out about Celsius and BlockFi.

Like many of you, I’ve traditionally held my cryptocurrencies secured in various wallets and on exchanges to execute trades (sometimes for longer than is recommended, I’ll admit). But the idea of taking my idling crypto and putting it to work has always been an attractive idea and what inspired me to do a deep dive into available platforms that might meet my needs.

All these platforms basically bring two traditional financial services to the crypto space — interest accounts and loans — disrupting the financial sector by enabling users to earn interest on their digital assets as well as borrow funds by using their cryptocurrency holdings as collateral.

Some people are curious about how BlockFi offers such attractive lending rates. The short of it is, they lend coins to hedge funds, exchanges, institutional traders, and by issuing asset-backed loans to retail customers. They haven’t made a list of companies public but have mentioned their investors do overlap with their institutional borrowers. You can find a list of their investors HERE and more about how their business works HERE.

I’ll do my best to keep this article updated with new information as things progress, but feel free to reach out if you ever have questions or further inquiries. Also, if you prefer to double-check any of the information in this article, feel free to visit BlockFi to see their most current offerings.

So without further adieu, let’s take a closer look at some of BlockFi’s Pros and Cons!

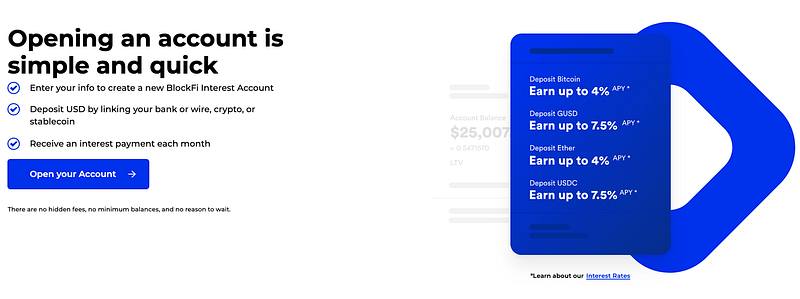

If you’re interested in creating a BlockFi Interest Account use my link HERE and receive up to $250 BTC bonus. Deposit $100, Receive $15 BTC and more!

What I Like about BlockFi (Pros):

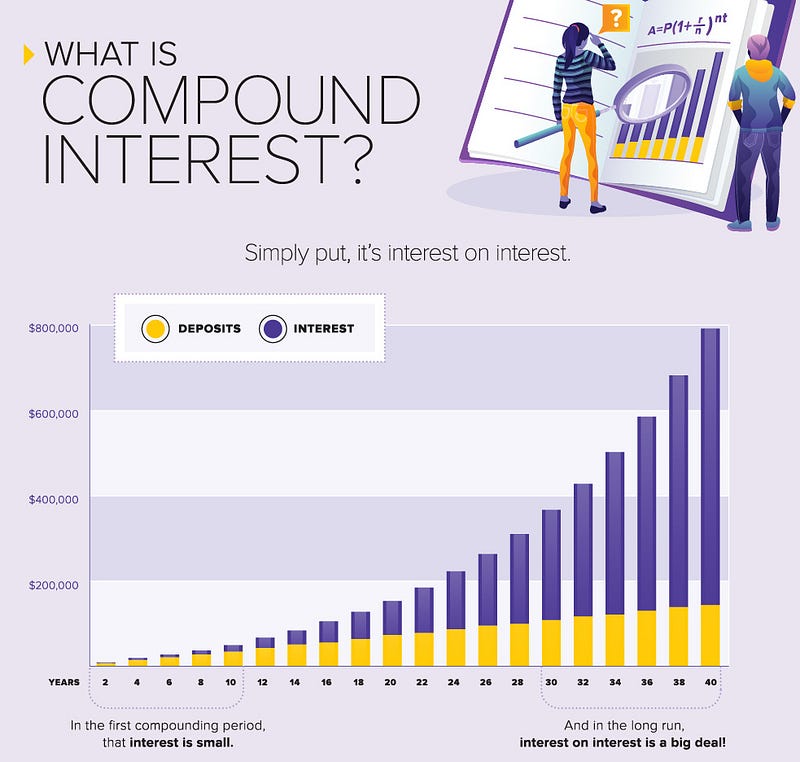

- Compound Interest — BlockFi was one of the first lending platforms to provide monthly compound interest before others caught on (What is Compound Interest?). Although it may seem like nothing special now since all the competition has reverted to the same model, it’s one of the reasons I first opted for BlockFi personally. Compound interest for those who aren’t familiar is where the interest you earn will also earn interest the following month. This means that if you earn interest in Month 1, your next interest payment will be calculated off of your new total balance (old balance + interest payment from Month 1). So if you deposit 1 BTC and earn 0.0051 BTC the first month, you will earn interest on the combined 1.0051 BTC the following month and so on and so forth. This is the best part of BlockFi’s Interest Accounts and a great way to build wealth exponentially over time.

- ACH & Wire Transfers—US users are now able to make ACH & Wire Transfers directly into their BlockFi accounts. ACH transfers are FREE but banks generally charge a processing fee for Wires (usually reserved for larger transfers & process quicker than ACH). For most users, ACH will be the most useful feature as it allows direct deposits of USD into your account at no charge and is now instantly available in your account earning interest and able to trade. Deposits are converted into GUSD at 1:1 for every dollar and made available in the depositors’ account. You can then convert it to USDC or PAX for free or redeem them back into your bank (in USD) as required. ACH transfers take 2–5 days to complete.

- No Early Withdrawal Penalty — Users are no longer subject to early withdrawal penalties which means you’ll be free to withdraw your funds at any time without taking a hit.

- Two Free Withdrawals per Month — Having the ability to withdraw funds for free is a welcomed feature — even if that’s only two per month (1 crypto/1 stablecoin). This will at least give those who have been looking to test out BlockFi’s product the opportunity to deposit a small amount of crypto to try it out for themselves. I hope they soon offer completely free withdrawals (however unlikely it may be).

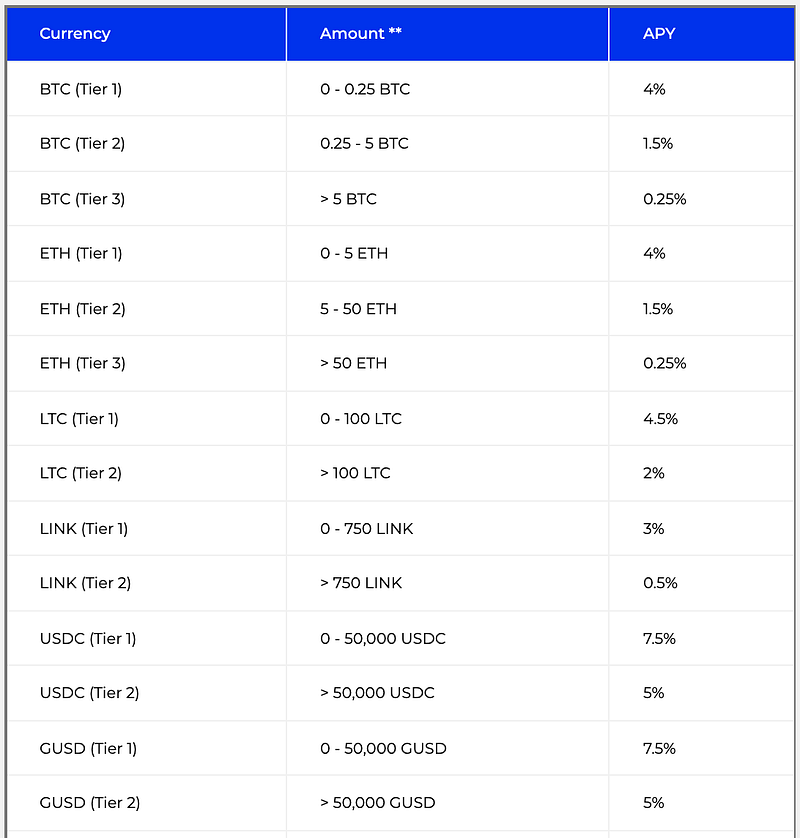

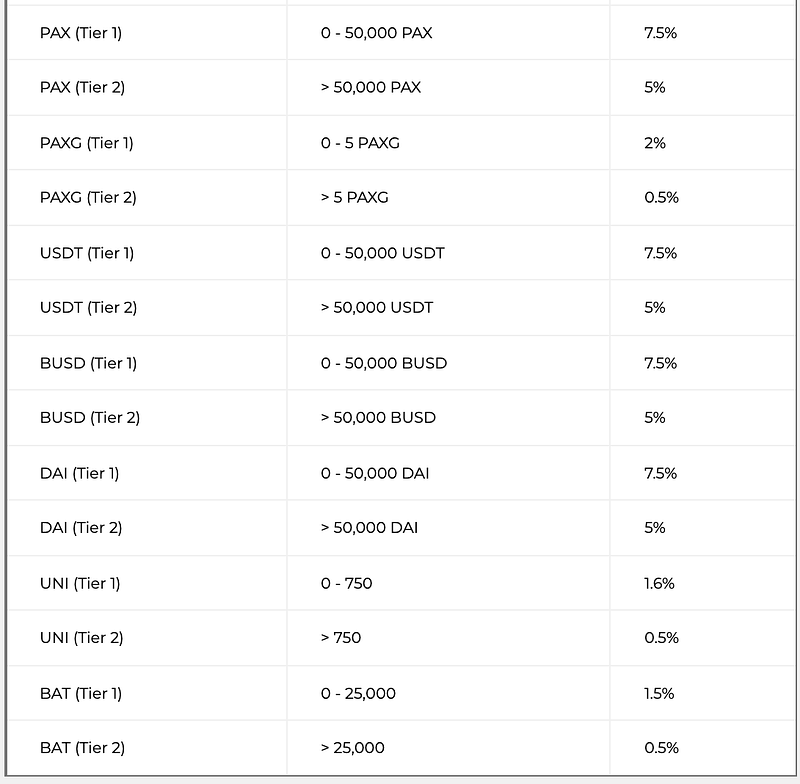

- USDC, LTC, LINK, BAT, UNI, PAX, PAXG, USDT, BUSD, & DAI Support — They’ve added support for several new assets including USDC, PAX, LTC, PAXG, USDT, BUSD, LINK, DAI, UNI, & BAT — allowing users to earn interest on additional assets. USDT is only available to non-US users.

- Zero-Fee Trading — BlockFi now offers a feature allowing users to seamlessly trade between their assets directly on the platform. There are also free stablecoin conversions which are very convenient! Another feature they added was repeat buys, so if you’re interested in dollar-cost averaging, this is a useful tool. You can designate a buy order for every day, week, 1st of the month, or 15th of the month. Keep in mind, you will be buying at a premium due to the spread similar to Coinbase, but it’s a nice feature for those interested in converting their funds into BTC or ETH more efficiently. (Read More)

- Earn In-Kind or Payment Flex— In-kind means you receive interest in the original asset invested, so you earn BTC if lending BTC and ETH if lending ETH. They now offer the ability to earn interest in an asset of choice (BTC, ETH, LTC, GUSD, USDC, PAX, BUSD, DAI, LINK, PAXG, BAT, or UNI) with Payment Flex. This means if you want to invest GUSD and earn your monthly interest in BTC, that is now possible. A pretty nifty feature, but keep in mind they charge 1% for this service!

- No Minimum Balance to Earn Interest — The BlockFi Interest Accounts no longer require a minimum balance to be eligible to earn interest, so what are you waiting for? Throwdown that $3.50, Mr. Buffett!

- No Balance Caps — BlockFi accounts have no maximum limits aside from tiered rates — whether that’s 1 ETH or 1 Million USDC, you can deposit as much as you want.

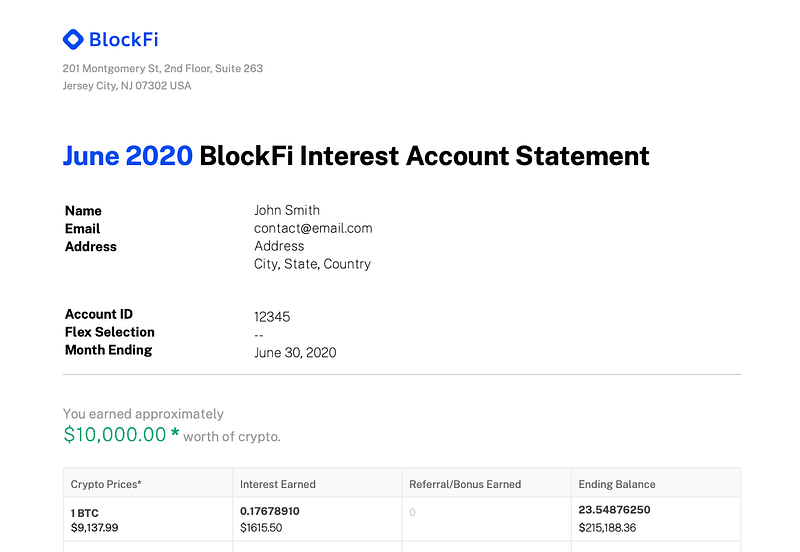

- Monthly Statements & Transaction History — They make record-keeping straightforward with monthly statements similar to what you would receive from a bank. It tells you how much you hold, how much you’ve earned, and how much you’re projected to make the following month. This used to be sent out in email form but now they’re available as pdf downloads in your account. You can also download CSV files for your trading and transaction history.

- Black Thursday Performance — The meltdown of the entire market in March of 2020 is a perfect window into how BlockFi expertly managed its risk. If any company was mismanaged and overleveraged, they would not have been able to survive such a sudden crash in my opinion. Not only did BlockFi come out the other end, but they were also largely praised by the community for saving individual borrowers from liquidation. It’s dark times like these that are the true test of the moral fiber and risk management of a lending company like BlockFi and they passed with flying colors.

- No Utility Tokens Required— Unlike the competition, BlockFi does not require utility tokens to take part in their service. Instead, all users are treated equally. This means you are not forced to trade/hold platform utility tokens which are often used by competing platforms to incentivize higher interest rates.

- Client Funds are Prioritized— BlockFi makes sure client funds are structured to be at the top of the capital stack even over BlockFi equity, and employee capital. This means if the worse case happens, BlockFi would take a loss before any client funds would take a hit. Still, keep in mind they are not FDIC or SIPC insured.

- Gemini Custodian Services— Your assets are securely stored at a unique wallet address generated by Gemini, a New York trust company licensed by the New York State Department of Financial Services. Gemini is a fiduciary under §100 of the New York Banking Law and held to specific capital reserve requirements and banking compliance standards. Gemini also has digital asset insurance coverage and is SOC 2 Type 1 security compliant on its exchange and custodian platform.

- Web & Mobile — They now offer mobile access in addition to web access. Their app is simple and easy to use with a simple, sleek UI. With biometric login features, you can quickly check your balance, make trades, and other transactions. BlockFi apps are available on both iOS and Android.

- Responsive Support — BlockFi support responds to user inquiries more promptly compared to my experience with Celsius and other platforms. Not to mention they have a phone number where you can speak to a live agent — something no other platform offers. The number for those curious is (646)779–9688.

- World’s First BTC Rewards Credit Card — They’ve announced the waitlist for the first BTC Credit Card ever — earning 1.5% in BTC on all purchases and now there’s no $200 annual fee! Keep in mind you will receive $250 if you spend more than $3,000 in the first 3 months. I hope to see improved terms in the future, but it’s a step in the right direction!

- Beneficiary Services — They will be incorporating this feature into the dashboard this year, but you can assign a beneficiary to your account on the backend in the event anything should happen to the account holder. For many users concerned about their crypto holdings getting lost, this will ensure you can pass down your hard-earned crypto as you intended. Follow the link to set this up. (Read More)

- Community/Outreach —I had previously stated their community outreach as being lacking, but they have been actively improving their exposure to the online community since I first wrote this article. They hold interviews with BlockFi staff on their youtube page and are more actively promoting their services on social media while building a surprising amount of online engagement on Twitter.

Up to $250 BTC Deposit Bonus — If you’re signing up with BlockFi they are offering free BTC with your first deposit. You can deposit as little as $100 worth of funds and receive $15 BTC or up to $250 BTC with more using this eligible LINK.

Things to Consider (Cons):

- Withdrawal Times — Your withdrawal request has a 1 business day hold (for security purposes) so expect withdrawals to be processed the following day — but keep in mind their hours of operation since pushing through withdrawals on the weekend may not go as planned. If you request a withdrawal on Friday you’ll receive your funds the following Monday as they are closed on weekends, so plan ahead! BlockFi also reserves up to 7 days to process a client withdrawal, but according to BlockFi, they’ve never exercised this right so far.

- Interest Rate Changes — In the past their rates have been fairly consistent compared to other platforms. That being said, they have continued to exercise their right (as indicated in their ToS) to change their interest rates. We always get a heads up the previous month on any upcoming changes. These adjustments have meant many depositors need to move their coins to other platforms or back to their wallets if they deem the new terms undesirable. But keep in mind, these changes are a positive sign that BlockFi is doing the responsible thing by offering realistic interest rates that adjust to the demand in the market. I still prefer BlockFi compared to dealing with weekly fluctuating APYs at Celsius.

- Monthly Payouts — I prefer more frequent interest payments especially now that many competitors offer daily or weekly payouts. A month feels like a very long time to wait for your interest distributions. That being said, you will receive your interest on the 1st business day of every month, so don’t freak out if the 1st lands on a national holiday or weekend, your interest will be paid on the following business day.

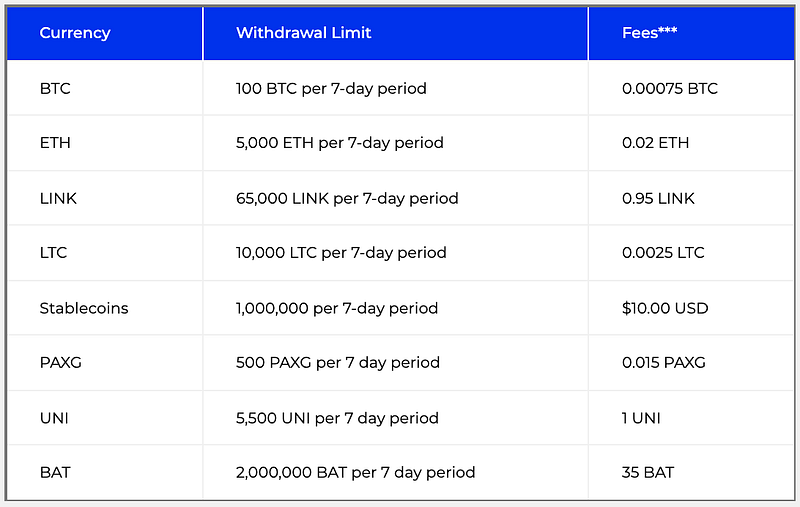

- Withdrawal Fees — Beyond the 2 free withdrawals every user receives every month, withdrawal fees will be charged. Many users noticed the high BTC fees initially which BlockFi has recently lowered from 0.0025 BTC to 0.00075 BTC. But it’s not all good news. Due to unprecedented congestion on the Ethereum network, ETH/Stablcoin fees have jumped up from a previous 0.0015 ETH and $0.25 to 0.02 ETH and $10, respectively. The more time passes, the less likely it seems we’ll ever see unlimited fee-less withdrawals. So if you’re looking to save on transaction fees, I highly suggest you limit your withdrawals best you can while taking advantage of your 2 free withdrawals every month.

- Adjustable Interest Rates —As mentioned above, you will need to keep in mind, BlockFi has the ability to adjust rates freely at their own discretion. They had initially promised 6.2% APY lending rates on all their digital assets; however, shortly thereafter lowered the ETH interest rates to 4% APY due to a stagnant ETH lending market with additional tier limits for all assets. But keep in mind this can go both ways as they raised the stablecoin rates to 8.6% (before most recently lowering their stablecoin rates for the first time in its history).

- Multiple Tier Rates—With their recent rate adjustment, users will need to track their tier limits for all assets and their tier-specific rates. To illustrate this point, let’s take a look at BTC. It is now split into 3 reward tiers. For tier 1, balances up to 0.25 BTC (lowered from the most recent 0.5 BTC cap) earn 4% while tier 2 earns 1.5% for balances between 0.25–5 BTC. LAstly, tier 3 earns 0.25% for all deposits over 5 BTC. To clarify, if you had 6 BTC in your BIA account, the first 0.25 BTC would earn Tier 1 interest at 4%, 4.75 BTC at Tier 2 with 1.5%, and the last 1 BTC Tier 3’s 0.25%. It’s unfortunate they’ve had to cap all asset tiers, but again, they’re adjusting to the market demand, and they are an early indicator of where rates in the entire space are headed, so this is clearly an industry-wide adjustment to the lowered demand for crypto — for now. Read more about their recent adjustments HERE.

- Limited Asset Options — They only offer BIAs for BTC, ETH, LTC, UNI, BAT, PAX, GUSD, USDC, BUSD, LINK, PAXG, BUSD & USDT while other platforms offer a larger variety. They mentioned they’ll be adding support for additional crypto, but they need to make sure there’s a healthy demand for a sustainable strategy. Unlike other platforms, they have been very methodical about approving new asset support which is promising.

- Lower Value Withdrawals— Any withdrawals under 0.003 BTC and 0.056 ETH could take up to 30 days to process.

- Must Pass KYC to Earn Interest — You can create an account, but in order to deposit funds and earn interest you must submit all required KYC information. If you’re someone who’s interested in keeping your identity hidden and big on blockchain privacy, this service is definitely not your cup of tea.

Can I trust BlockFi?

When people ask why I trust a company like BlockFi, I think my general response is, have you ever trusted any crypto exchange in the past? It really is no different. This being an unregulated space, there really are no assurances of any company acting in the users' best interest. Exchanges have been caught running fractional reserves and taking part in illicit activities in the past — leveraging depositors' funds as a slush fund for their own personal use and investing in high-risk schemes without user consent. So if you are willing to take on counterparty risk by keeping your crypto parked on an exchange (earning no interest), why wouldn’t you place your trust in a company like BlockFi that pays you interest for lending them your idling funds and specialize in putting that money to work on your behalf; a company that has large institutional backing from reputable companies like Coinbase, Consensys, Fidelity, Valar, Sofi, and Mike Novogratz’s Galaxy Digital; uses trusted and licensed custodial services like Gemini; who also is fully regulated with lending licenses and operates above board under Article 9 of the Uniform Commercial Code.

Another valid question is what happens when you deposit crypto with BlockFi? Basically, they are obligated to return the same amount of crypto with earned interest back to you. And in order to pay our interest every month, they do a few things. Many people overlook the high demand for client withdrawals which means they keep a significant chunk of crypto with their custody partners to meet such demands. That’s right, BlockFi can’t just lend out all our money, because they’re not like CDs with a lockup period — they can’t control when we deposit or withdraw our funds. They also make it known they purchase equities and futures from regulated markets and apply proper risk management to their lending activities with institutions. The credit risks to these companies are mitigated by a combination of credit due diligence and collateral in the form of cash, crypto, or other assets.

Basically, they do their homework and have so far passed with straight As.

Data Breach

I’ll be the first to admit I was not pleased to hear about the data breach in May 2020 — it was their marketing database holding customer information that was impacted. I was notified my information was compromised along with many other users. They quickly sent out an incident report to us detailing what had occurred. Thankfully, no funds were lost. But our data is something we take for granted that can have a large impact on our livelihood if we’re not careful.

To put things into perspective, Ledger had their users' details leaked in a similar fashion which led to phishing attempts of those users. Not to mention, there were two other financial institutions I do business with that suffered the same fate in May. These hacks are becoming more common and using sophisticated tactics along with long known social engineering tactics that many companies have simply overlooked for years. Companies need to do a better job of protecting our information. They need to adapt to the times and stay ahead of the new wave of hackers and phishing scams scouring for weaknesses in online databases.

At the end of the day, actions speak louder than words, and in BlockFi’s case, there’s no denying they took this incident very seriously. They promptly hired Adam Healy as their Chief Security Officer who has laid out a comprehensive roadmap to revamp their security protocols. He has held roles within the U.S. Intelligence Community and Department of Defense, Microsoft, Palantir Technologies, and in his previous role as CISO at Bakkt, he oversaw security operations for safeguarding institutional clients’ digital assets.

If anything, this should encourage new users to feel safer at BlockFi as I believe this is evidence they are more secure than they have ever been.

What about Rehypothecation?

Some critics in the past have mentioned the legalese in BlockFi’s Terms of Service (ToS) allowing “Rehypothecation” of user funds. This is where collateral for a loan is repurposed or churned for additional use and is a common mechanism used in finance by large institutions. BlockFi has responded to these concerns with this blog entry which clarifies their stance on the matter. This is what, at least in part, allows them to offer their high interest rates to depositors like us. They also push back against the idea that the 2008 financial crisis was caused by Rehypothecation — it was in their opinion bad underwriting, over-leveraged deals, and miscalculated risk that did us in.

For anyone that has read ToS and User Agreements for similar lending platforms, the language used in these contracts is strikingly similar and generally includes a “Rehypothecate/Rehypothecation” clause— yes, this includes the crypto community’s golden child of lending Celsius Network’s Terms of Service.

And if you’re uncomfortable with the idea of rehypothecation, you will likely be uncomfortable with all of the lending platforms as they all leverage similar structures.

Black Thursday

As mentioned previously, if you look to the “Black Thursday” event in March 2020, all markets spiraled out of the control and caused a major liquidation event. This sort of event is why risk management is so integral to the success of a lending business like BlockFi. This was a textbook event where rehypothecation could and would have gone wrong if they were mismanaged and overextended. But thanks to BlockFi’s experienced investment strategies, nothing happened.

This is the best testament that BlockFi has robust safety parameters in place to effectively navigate even the worst market moves crypto can throw at them. And that’s saying a lot.

In Conclusion

BlockFi has its share of caveats, but the most important thing to keep in mind is the trust that they have built with users like myself.

At the end of the day, you control where you deposit your valued coins, and if you’re keen on earning interest on your crypto, why not do it with a company that has survived the turbulent March 2020 price dump and who has been heavily praised by borrowers on their platform for responsive support and helping avoid liquidations? When times are tough, a company’s true nature bubbles to the surface and in BlockFi’s case, they’re doing a top-notch job with a client-first approach.

For those curious to hear more about BlockFi, I highly suggest checking out the podcast with BlockFi CEO Zac Prince linked below. I found it very informative hearing what the company is aiming to achieve and how they plan on making waves in the crypto space while keeping our funds safe.

You’ll have to decide whether BlockFi is the right fit for you!

There are plenty of lending platforms out there with their own pros and cons. As always, I suggest doing your own due diligence and make sure you stay informed!

For further inquiries, you can always reach BlockFi support at [email protected]

Happy earnings!