Predictive Analytics in Finance: Utilizing XGBoost for Stock Trend and Price Forecasting

In this article, I will use XGBRegressor from XGBoost library to predict future prices of stocks using technical indicators as features.

Let’s start coding:

import os

import numpy as np

import pandas as pd

import xgboost as xgb

import matplotlib.pyplot as plt

from xgboost import plot_importance, plot_tree

from sklearn.metrics import mean_squared_error

from sklearn.preprocessing import MinMaxScaler

from sklearn.model_selection import train_test_split, GridSearchCV

# Time series decomposition

!pip install stldecompose

from stldecompose import decompose

# Chart drawing

import plotly as py

import plotly.io as pio

import plotly.graph_objects as go

from plotly.subplots import make_subplots

from plotly.offline import download_plotlyjs, init_notebook_mode, plot, iplot

# Mute sklearn warnings

from warnings import simplefilter

simplefilter(action='ignore', category=FutureWarning)

simplefilter(action='ignore', category=DeprecationWarning)

# Show charts when running kernel

init_notebook_mode(connected=True)

# Change default background color for all visualizations

layout=go.Layout(paper_bgcolor='rgba(0,0,0,0)', plot_bgcolor='rgba(250,250,250,0.8)')

fig = go.Figure(layout=layout)

templated_fig = pio.to_templated(fig)

pio.templates['my_template'] = templated_fig.layout.template

pio.templates.default = 'my_template'Here in this code we import a series of libraries including XGBoost, NumPy, Pandas, and plotly. We also install library STLDecompose. We define various functions and sets default values, such as muting warnings and changing the background color of visualisation.

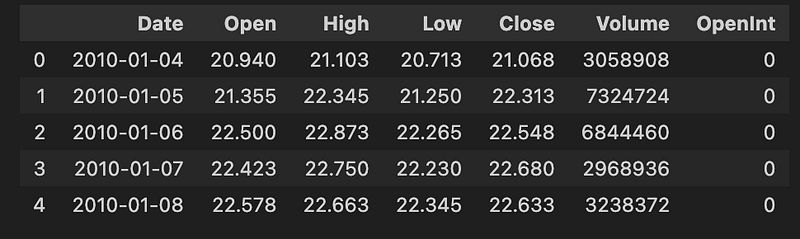

Read Historical Prices

ETF_NAME = 'CERN'

ETF_DIRECTORY = '/kaggle/input/price-volume-data-for-all-us-stocks-etfs/Data/Stocks/'

df = pd.read_csv(os.path.join(ETF_DIRECTORY, ETF_NAME.lower() + '.us.txt'), sep=',')

df['Date'] = pd.to_datetime(df['Date'])

df = df[(df['Date'].dt.year >= 2010)].copy()

df.index = range(len(df))

df.head()

In this code we load our dataset from a specified directory, filters out the data to only include dates from 2010 or later, and then displays the first few rows of the dataset.

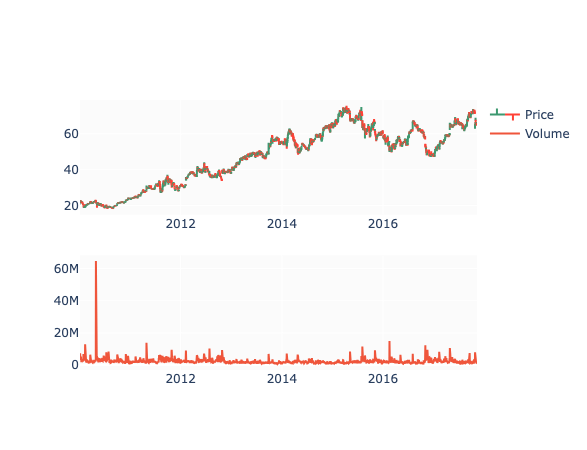

OHLC Chart

fig = make_subplots(rows=2, cols=1)

fig.add_trace(go.Ohlc(x=df.Date,

open=df.Open,

high=df.High,

low=df.Low,

close=df.Close,

name='Price'), row=1, col=1)

fig.add_trace(go.Scatter(x=df.Date, y=df.Volume, name='Volume'), row=2, col=1)

fig.update(layout_xaxis_rangeslider_visible=False)

fig.show()

Here we create a subplot with two rows and one column, and then add two trace elements to it — one for stock’s open, high, low, and close prices and one for its volume. Then we update the layout to hide the range slider on the x-axis and show the resulting plot.

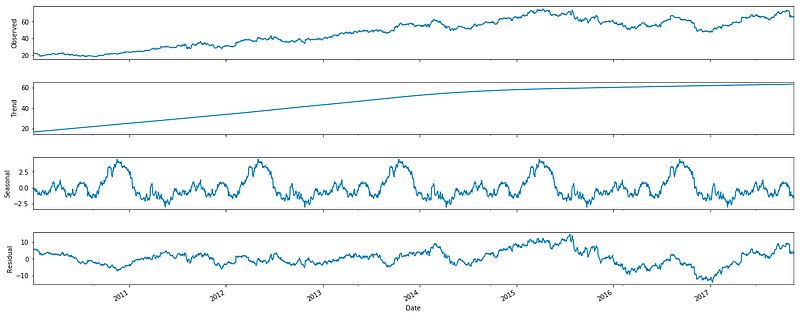

Decomposition

df_close = df[['Date', 'Close']].copy()

df_close = df_close.set_index('Date')

df_close.head()

decomp = decompose(df_close, period=365)

fig = decomp.plot()

fig.set_size_inches(20, 8)

Now we create a copy of a dataframe that contains two columns Date and Close, set the Date column as the index, performs a decomposition on the data with a period of 365, and then plots the decomposition on a figure.

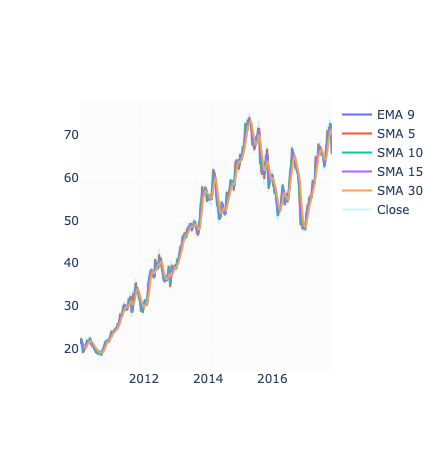

Technical Indicators

df['EMA_9'] = df['Close'].ewm(9).mean().shift()

df['SMA_5'] = df['Close'].rolling(5).mean().shift()

df['SMA_10'] = df['Close'].rolling(10).mean().shift()

df['SMA_15'] = df['Close'].rolling(15).mean().shift()

df['SMA_30'] = df['Close'].rolling(30).mean().shift()

fig = go.Figure()

fig.add_trace(go.Scatter(x=df.Date, y=df.EMA_9, name='EMA 9'))

fig.add_trace(go.Scatter(x=df.Date, y=df.SMA_5, name='SMA 5'))

fig.add_trace(go.Scatter(x=df.Date, y=df.SMA_10, name='SMA 10'))

fig.add_trace(go.Scatter(x=df.Date, y=df.SMA_15, name='SMA 15'))

fig.add_trace(go.Scatter(x=df.Date, y=df.SMA_30, name='SMA 30'))

fig.add_trace(go.Scatter(x=df.Date, y=df.Close, name='Close', opacity=0.2))

fig.show()

This code adds several new columns to the dataframe, each containing the mean of the ‘Close’ column for different time periods. It then creates a graph using this data, with each line representing one of the calculated means and the opacity set for the original ‘Close’ data. Finally, it displays the graph.

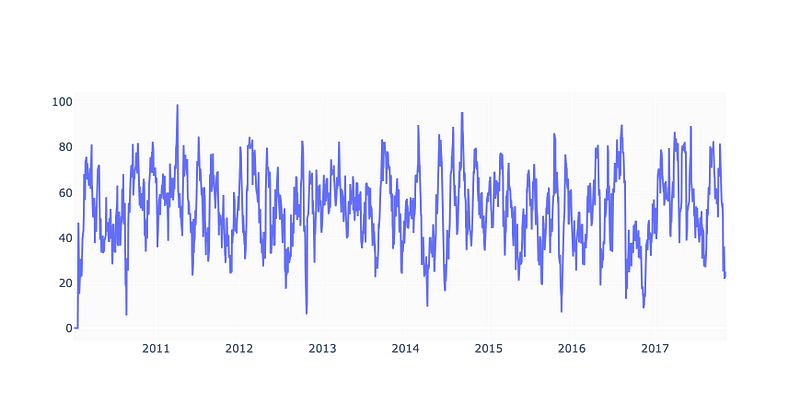

Relative Strength Index

def relative_strength_idx(df, n=14):

close = df['Close']

delta = close.diff()

delta = delta[1:]

pricesUp = delta.copy()

pricesDown = delta.copy()

pricesUp[pricesUp < 0] = 0

pricesDown[pricesDown > 0] = 0

rollUp = pricesUp.rolling(n).mean()

rollDown = pricesDown.abs().rolling(n).mean()

rs = rollUp / rollDown

rsi = 100.0 - (100.0 / (1.0 + rs))

return rsi

df['RSI'] = relative_strength_idx(df).fillna(0)

fig = go.Figure(go.Scatter(x=df.Date, y=df.RSI, name='RSI'))

fig.show()

In this code we calculate the RSI of our stock. The function relative_strength_idx takes in a dataframe of our stock and calculate the RSI using a default period of 14 days, unless specified otherwise. The RSI is then added as a new column RSI to the original dataframe and any missing values are filled with 0. The result is then plotted using the plotly library and then displayed.

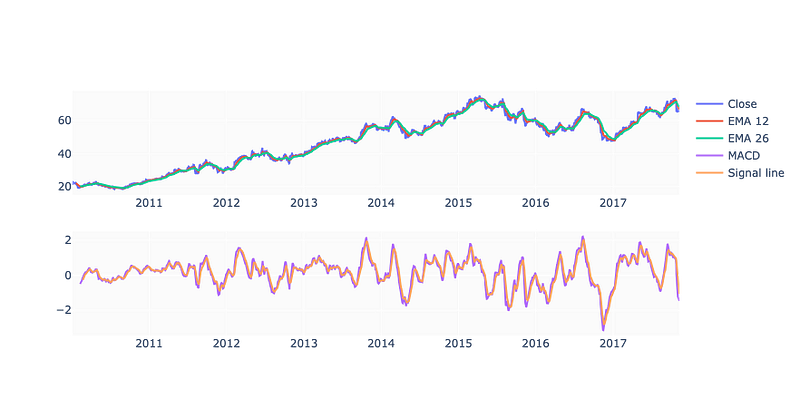

MACD

EMA_12 = pd.Series(df['Close'].ewm(span=12, min_periods=12).mean())

EMA_26 = pd.Series(df['Close'].ewm(span=26, min_periods=26).mean())

df['MACD'] = pd.Series(EMA_12 - EMA_26)

df['MACD_signal'] = pd.Series(df.MACD.ewm(span=9, min_periods=9).mean())

fig = make_subplots(rows=2, cols=1)

fig.add_trace(go.Scatter(x=df.Date, y=df.Close, name='Close'), row=1, col=1)

fig.add_trace(go.Scatter(x=df.Date, y=EMA_12, name='EMA 12'), row=1, col=1)

fig.add_trace(go.Scatter(x=df.Date, y=EMA_26, name='EMA 26'), row=1, col=1)

fig.add_trace(go.Scatter(x=df.Date, y=df['MACD'], name='MACD'), row=2, col=1)

fig.add_trace(go.Scatter(x=df.Date, y=df['MACD_signal'], name='Signal line'), row=2, col=1)

fig.show()

This code calculates the Exponential Moving Average (EMA) and Moving Average Convergence Divergence (MACD) indicators for a financial dataset and creates a visual representation of the data using a plot.

Drop Invalid Samples

df = df.iloc[33:] # Because of moving averages and MACD line

df = df[:-1] # Because of shifting close price

df.index = range(len(df))Using this code we select rows from the df dataframe starting from index 33 until the end and assign it to the variable df. It also removes the last row of the dataframe and updates the index based on the new length of the dataframe.

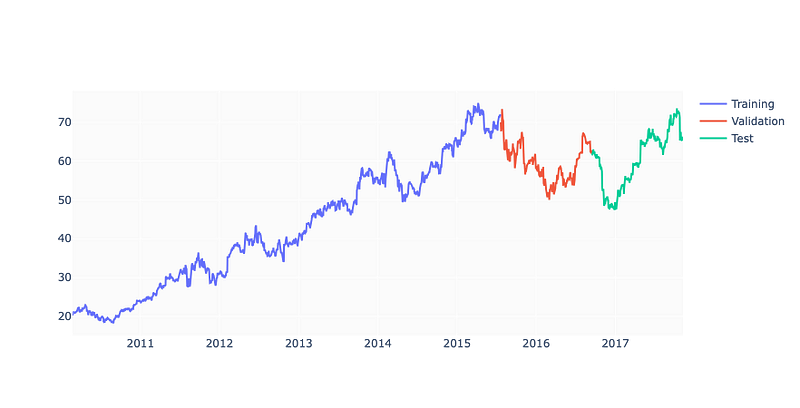

test_size = 0.15

valid_size = 0.15

test_split_idx = int(df.shape[0] * (1-test_size))

valid_split_idx = int(df.shape[0] * (1-(valid_size+test_size)))

train_df = df.loc[:valid_split_idx].copy()

valid_df = df.loc[valid_split_idx+1:test_split_idx].copy()

test_df = df.loc[test_split_idx+1:].copy()

fig = go.Figure()

fig.add_trace(go.Scatter(x=train_df.Date, y=train_df.Close, name='Training'))

fig.add_trace(go.Scatter(x=valid_df.Date, y=valid_df.Close, name='Validation'))

fig.add_trace(go.Scatter(x=test_df.Date, y=test_df.Close, name='Test'))

fig.show()

Crafting a dataset the code splits an existing dataset into three segments: training, validation, and test. The dimensions of the test set and validation set are dictated by the test_size and valid_size variables. The dataset is severed at a certain index based on the size of the dataset multiplied by the test size or validation size. The training set encompasses all data up to the validation split index, the validation set contains data between the validation split index and the test split index, and the test set holds all the data after the test split index. Lastly a plot is fashioned using three distinct Scatter objects one for each dataset and then displayed.

Fine Tune

%%time

parameters = {

'n_estimators': [100, 200, 300, 400],

'learning_rate': [0.001, 0.005, 0.01, 0.05],

'max_depth': [8, 10, 12, 15],

'gamma': [0.001, 0.005, 0.01, 0.02],

'random_state': [42]

}

eval_set = [(X_train, y_train), (X_valid, y_valid)]

model = xgb.XGBRegressor(eval_set=eval_set, objective='reg:squarederror', verbose=False)

clf = GridSearchCV(model, parameters)

clf.fit(X_train, y_train)

print(f'Best params: {clf.best_params_}')

print(f'Best validation score = {clf.best_score_}')

Constructing a dictionary of parameters for a machine learning model the code sets up an evaluation set creates a model using the XGBRegressor class and then employs GridSearchCV to discern the best combination of parameters for the model. It then outputs the best parameters and the best validation score for the model.

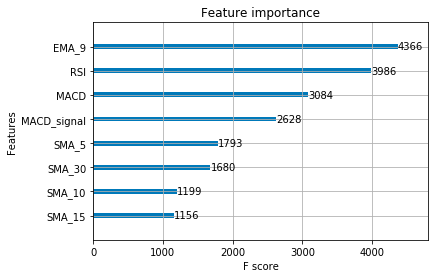

plot_importance(model);

We plot the importance of different features in a model.

Calculate and Visualise Predictions

y_pred = model.predict(X_test)

print(f'y_true = {np.array(y_test)[:5]}')

print(f'y_pred = {y_pred[:5]}')

In this code we use a trained model to predict outcomes for a given set of data. It then prints the first 5 actual outcomes from the test data and the first 5 predicted outcome.

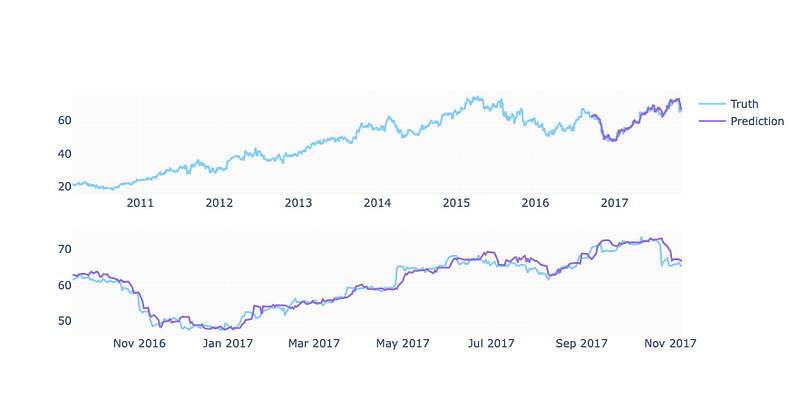

predicted_prices = df.loc[test_split_idx+1:].copy()

predicted_prices['Close'] = y_pred

fig = make_subplots(rows=2, cols=1)

fig.add_trace(go.Scatter(x=df.Date, y=df.Close,

name='Truth',

marker_color='LightSkyBlue'), row=1, col=1)

fig.add_trace(go.Scatter(x=predicted_prices.Date,

y=predicted_prices.Close,

name='Prediction',

marker_color='MediumPurple'), row=1, col=1)

fig.add_trace(go.Scatter(x=predicted_prices.Date,

y=y_test,

name='Truth',

marker_color='LightSkyBlue',

showlegend=False), row=2, col=1)

fig.add_trace(go.Scatter(x=predicted_prices.Date,

y=y_pred,

name='Prediction',

marker_color='MediumPurple',

showlegend=False), row=2, col=1)

fig.show()

Here are our final predictions.

And this is how we can forecast stock using xgboost.