Plugged In Or Priced Out?

Costs and Barriers of Entry Into The EV Market.

Bitesize Edition

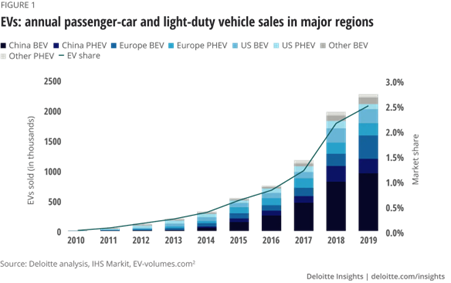

- The EV transition is underway, but it still has a long way to go. 2019 data from Deloitte states EVs only have 3% of the total vehicle market share.

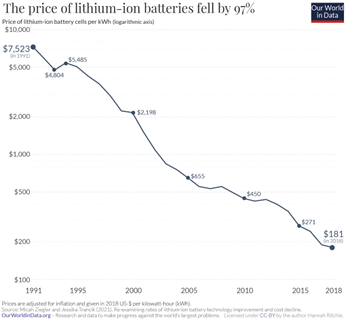

- The price of lithium-ion batteries has dropped dramatically, falling 97% since 1991. This is helping to reduce the overall price of electric vehicles, but is it enough?

- For first-time buyers of vehicles in a few decades, their only choice will be electric. Once you have an electric vehicle, it’s cheaper to run than ICE vehicles if you have a 7kW home charger installed. However, will these new participants in the transportation sector be priced out due to high upfront costs? If these consumers can’t afford a car upfront, they certainly won’t be able to afford an imaginary house upon which they can place their imaginary 7kW home charger.

- Will we see the innovation of how we move around? Ride-sharing services such as Uber and driverless taxis, such as those invented by Waymo are seeing a rise in popularity.

Introduction

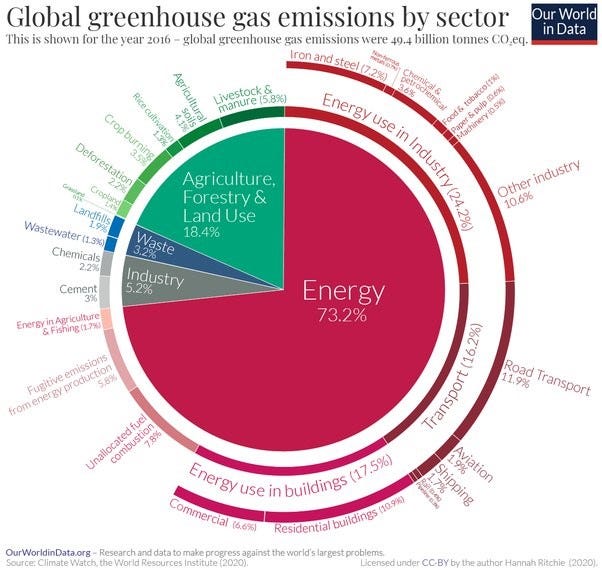

The clean energy transition is needed in energy use in buildings and industry, in agriculture, and industries such as cement and production of chemicals such as fertilisers. Road transport is one of the largest sectors of greenhouse gas emissions as of 2016 data.

This ensures transport will be one of the largest transitions to modern life as we transition to the green age. Lithium is of vital importance to this transition.

Cost of Lithium and Adoption of EVs

Lithium is now a developed industry, with price per kWh having dropped 97% since the 1990s, according to 2018 data.

This is aiding the speed of the EV transition, with 2019 data seeing EVs approach 3% of the total market share. This figure, in my opinion, remains surprisingly low, even if it is a few years old.

Over recent years, many car manufacturers have pivoted solely to EV production out of fear of being left behind. This is easier said than done, especially in a rising interest rate environment. Volkswagen recently announced a large number of layoffs, with the reason stated as a stalled EV transition for the German company. Notably, Volkswagen has seen its market share drop in China due to the rise of BYD, Tesla, and other smaller Chinese EV companies such as NIO and Li Auto, the former of which reported a revenue miss in its Q4 earnings but saw 46% vehicle sales rise YoY and a 47% revenue increase YoY. A key trend to consider is how these car manufacturers partner with battery manufacturers to secure up their supply chains. Without lithium-ion for EV batteries, good luck growing your business.

The automaker sector is shifting dramatically. Did those who started the EV transition earlier find themselves in an advantageous position versus those who were later?

How vehicles are built and used is also changing. Almost 100 components of an ICE vehicle are no longer required in EVs, and 41 new components will become staples of EVs.

Many states hope to see their automakers be the ones to pave the way to EVs taking the majority of the automobile market share from ICE vehicles. However, to even get EVs moving, we need ample charging facilities.

EV Charging

In the UK, research conducted by the RAC in May 2023 saw only 23% of 119 motorway service stations possessing the target number of EV chargers.

The close to 400 chargers can charge 682 EVs at one time.

This low progress isn’t meeting targets proposed in May 2020 and reiterated in March 2022, when the government stated the need for six rapid chargers at each motorway station by the end of 2023. These rapid charge points can charge a battery for 100 miles of range in 35 minutes.

Another problem with EV charging is cost. Currently, the use of rapid and ultra-rapid chargers is more costly than petrol and diesel as of October 2023. However, using a 7kW home charger is much cheaper. To get a 7kW home charger, the installation cost and cost of the charger is around £1000. With a £350 government grant, the cost can be brought down to £650 (UK). In the United States, there are tax breaks and tax credit incentives when purchasing EVs.

The cost per mile from a home charger is 8p. Compare this with petrol and diesel (18p), rapid chargers (20p) and ultra-rapid chargers (22p).

If using an ICE vehicle, you’d only need to travel 6500 miles in an electric vehicle charged from a home charger to save money on the installation and purchase of the charger.

Mathematics Explanation:

£650 = Cost of 7kW Charger (With Grant)

£0.10 = Savings per Mile Driving Home Charged EV versus Petrol/Diesel Vehicle.

£650/0.10 = 6500 Miles To Breakeven on Charger Cost And Cost Saved Per Mile With EV.

This doesn’t consider the cost of electricity used from your home to power the charger and charge the car, however. It appears the cost of electricity added to your annual bill is still cheaper than the mileage in fuel costs.

The transportation transition is accelerating and is forecast to continue speeding up. Will the costs of home chargers, or the high cost to purchase electric vehicles upfront lead to shifts in the automobile market? Will auto loan debt continue to rise as consumers purchase vehicles on finance? Will ride-sharing services continue to grow in popularity?

Using the UK as a case study will differ from other states. Firstly, the UK has a large population but a small landmass. Population density is fairly high. The high percentage of 1km squares populated does contribute to very few areas where there will exist long rural driving where a range of an electric vehicle would come into question. As a result, the strategy to place electric vehicle chargers along motorway service stations and near population centres is a promising strategy for reaching the majority of the population. Take a large, developed country with a large urban population in a small area and the logistics of electric vehicle charging becomes more difficult. A key point governments will have to consider in their electric vehicle charging approaches.

You Will Own Nothing

In the trend towards us all eating bugs for dinner and not owning anything, some sectors will see an increase in debt financing or subscription-based models. This can allow consumers to access technologies and services they would otherwise be priced out of if paying upfront in one payment was the only option.

This trend has seen an increase in auto debt and a decrease in vehicle ownership percentages. Many ride-sharing services are also arising to reduce the need for private vehicle ownership, especially in cities.

Take the case of Waymo for example. They are now operating driverless taxis in Austin, after already operating in San Francisco, Los Angeles, and Phoenix.

One thing is clear. The automobile clean transition could be one of the biggest paradigm shifts in the transport sector since the invention of the ICE vehicle. We’ve also discussed alternatives to EVs such as hydrogen fuel cell vehicles and the adoption of synthetic fuels in transportation, which still struggle to achieve scalability and viable competition for lower costs to consumers. The fight for automobile market share is well and truly underway.

Will consumers accept the trend towards lower ownership if alternative transport methods are implemented? This remains to be seen.

Concluding Remarks

This transition towards electrifying the transportation sector will go down in history as one of the greatest technological shifts ever attempted by humanity. How it will change our consumeristic tendencies remains to be seen. However, the current trends support young consumers being priced out of the EV market. Greater innovation still has to be seen to further lower costs.