Paying off Debt vs Investing — Getting the Most for Your Money

A guide to help you develop your personal plan

Meme stocks (GameStop’s diamond hands), Elon-approved cryptocurrencies (Dogecoin millionaires, anyone?) — investing isn’t the boring hobby it used to be. With so much hype, it’s only natural that more people want in on the fun.

But if you’re one of the 40 million-plus adults with student debt, dipping your toes into the market is a classic “chicken or egg” scenario: do you aim to build wealth by paying off your loans quicker or by investing for your future?

An argument for Paying off your Debt:

Debt sucks. Debt is the worst.

While there are good debt and bad debt, in general, most people don’t want to have debt. Debt is like a big weight on your shoulder and it’s always on your conscience. Have you ever caught yourself or someone you know say: “I would like to do this, but I have all this debt” or “I would like to invest in this, but I have all this debt” or “I would like a vacation, but I can’t, I have all this debt.” It’s a never-ending weight, always chipping away at you. It causes stress, marital problems. According to a Citibank survey, 57% of divorces stemmed from some sort of financial stress.

Another downside of debt is you can make hasty decision when you have debt. For example, you lost your job and you have to take another job immediately. Instead of being in the market longer and pick the dream job, you don’t have the time and have to accept the first job offer that you might not want. You have no choice because of the over-looming debt.

An argument for investing:

Greater return from investing than paying off debt

Personal finance is personal decisions about your finance. It’s deeply behavioral rather than mathematical. The first common argument many new investor make is: “I can make a 10% return on the market instead of paying of 6–7% loans (e.g: student loan). Why would I want to pay off my debt?”

Paying off your debt (student loan, mortgage, credit card debt, etc.) is a guaranteed rate of return. If you pay the debt off (e.g: $20,000 of student loan), you are guaranteeing yourself an annual rate of return of 6% — which would have been the interest rate you carry if you still have the loan.

What if you want to keep investing in the market at the return rate of 10%, and pay monthly pay with interest on your loan at 6–7% and profit the difference (3–4%)? Yes, this strategy is great in great times when the stock markets experience newer highs every month. It’s especially true after March 2020 brief collapse, retail investors had enjoyed the rise of meme stocks (GME, AMC, …) and crypto (Dogecoin, Shiba Inu) after the market recovered following government stimulus and the Feds’ money printing. However, these new investors never experienced a huge market downturn like 2008 when people lost 40–50% of their portfolio.

While this argument is viable, a guaranteed of return involves no risk, and uncertainty. In contrast, here are methods for curbing your risk, such as diversifying your portfolio, but no investment is entirely free of risk. Therefore, if you are an individual with a lot of high interest debt, or a large amount of student loans, consider paying down your debt will give you more peace of mind.

Can you balance the two options, perhaps a hybrid plan, if you’re strategic about it. Here are the four key questions to ask yourself as you determine your best fitted plan for your financial situations.

What are your Financial Goals?

The reason you should know your goals is because they dictate which path you are going to take. For example, a high-income person (above $200,000) in their late 20s, early 30s will prefer investing over savings or paying of debts. They are not satisfied with guaranteed fixed returns, they will always be hungry for the next big return to make more. They have a big appetite for consumption as they would have for investing in stocks, real estate, etc. Only you know the answer to this question, because only you know yourself better than anybody does.

For the majority, the financial goals are aligned with the middle class.

These people represent your 8 to 5, W2 employees with some investments but also debts (student loans, mortgages, car loans) and responsibilities (child care, medical cost, aging parents). If you identify with this group, and want to retire relatively stress-free, paying off high-interest debt first before investing probably will give you a better peace of mind.

Tips: The psychological benefit of being debt-free can avoid you marital stress, the overhead (interest payment) of your debt, the crappy job you don’t want to take. Once free of debt, you can really kick your wealth-building into high gears, and start increasing your saving rates by maxing out your 401(k) with employer’s match and your Roth IRA.

What is your Age?

I have written about the magic of compound interest because I believe it is the secret of a fulfilled life. This is the reason I try to write a post about personal finance and personal development at least once a week. I hope that building that writing muscle will compound benefits over time.

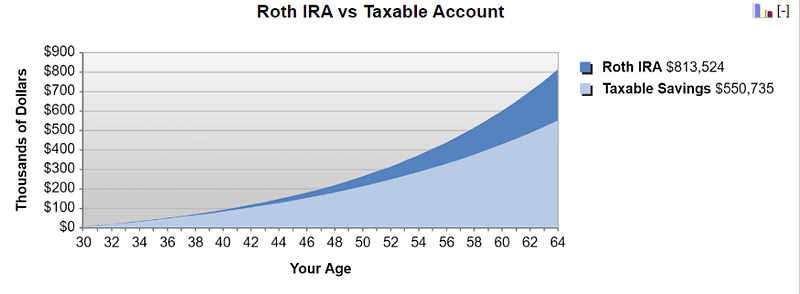

Applying this principle to your financial life, the younger you start investing, the more time your money can compound on itself. For example, if you start investing $5,500/year at 7% return from age 30 to 65. This is below the maximum contribution for Roth IRA in 2021, and it’s generally an achievable amount of savings per year. Perhaps, taking a side hustle (Uber, Doordash, Instacart) can help you earn this money without dipping into your current budget.

The graph above shows the result of your hypothetical investment, compounded over 35 years. You would have in your Roth IRA $813,524. While it doesn’t take into account inflation or any other economic conditions within the timeframe, that is an astonishing number that is much harder to reach with any short-term investments. If you are relatively young and have no major responsibilities (children, parents, health care costs) and high-interest debts, I would prioritize investing to maximize on the benefit of compound interest.

Tips: Let time work in your advantage and grow your investment. You can delay paying off debts or do a hybrid between maxing out Roth IRA and paying down your higher-interest debt.

Do you have FOMO?

Fear of Missing Out might sounds like this “I’m on the sidelines. Everyone is investing in GME. To the moons, baby. Paper hands …” I’ve been there and that resulted me in buying 3 GME shares on Robinhood at the peak of the short squeeze in January 2021. Needless to say, I lost more than a several hundreds of dollar within 3 days.

I had FOMO and that taught me a valuable lesson. My loss is infinitesimal compared to many that caught on the craze late January 2021. Many made millions, while other might have lost everything, taking out a second mortgage to buy into meme stocks.

It’s easy to be caught up to a new investing scheme in this hyper-socialized digital age. I follow multiple YouTubers, podcasters, Instagram and TikTok influencers, all of which inevitably recommend a different investing scheme. It can be real estate, cryptocurrency, NFTs, options trading, etc… Take an honest look at your investment to make sure you know why you’re investing in something. If you don’t know the reason behind an investment, you most likely have FOMO.

Tips: Start with small investment and paying off your debt first. Especially in a highly volatile market that we are experiencing right now, smaller investments allow you to keep your emotions in check. You will learn how to invest with discipline while paying down debt at the same time.

Do you have enough money to invest?

When you put together a budget, the first order of business is usually to make sure you can cover your basic expenses — things like rent, groceries, and monthly student loan payments. You also want to make room in your budget for things you want, like eating out. Any money left over, that’s money you can save or invest.

Often, people invest all of their money and neglect one of the most important tool of a responsible adult: an emergency fund to help you stay afloat during financial stressful times — from emergency car repairs to getting by if you lose your job.

Instead of being in a 3-6 month emergency fund, if your money is tied up in a brokerage account or 401(k), you will be forced to take out your investment and incur penalties, taxes and fees. If this scenario happens, it might wipe out any excess return you have accumulated because you might have to sell your investments when the market is down.

Tips: Focus on building up your emergency fund (3–6 months of expense) then decide whether to pay down debt or to invest.

The bottom line

There’s not a one-size-fits-all answer when it comes to deciding between paying off debt or investing — even experts disagree on which one should come first. Some argue that debt is like “handcuffs” and the sooner you can get rid of it, the better. Others think that you need to start investing as early as possible to not miss out on potential returns.

Ultimately, growing your money isn’t just about paying off debts vs. investment, it’s a balancing act. Many people have a hybrid plan to paying down debt while maintaining a diversified/lower risk investment portfolio. After all, they serve separate purposes and have distinct risks and benefits.

By understanding the difference between paying off your debts and investing, you can apply that knowledge to find the balance that best meets your short- and long-term financial goals.

Thank you for reading my post, and I hope you found it useful and informative for your financial independence journey. Please support me by follow me, subscribe to Medium or check out my other posts for more personal finance and self-improvement tips. As always, have a fulfilled day as you go out there and be your best self.