Nassim Nicholas Taleb: Revolutionizing Finance with Unconventional Theories and Discoveries ~Part 1~

Nassim Nicholas Taleb is a renowned scholar, mathematician, author, and former options trader who has made a significant impact on the field of finance. Throughout his career, Taleb has challenged conventional wisdom and introduced groundbreaking concepts that have reshaped the way we understand risk, uncertainty, and decision-making in financial markets.

This article delves into the life of Nassim Nicholas Taleb, his influential theories, and the lasting legacy he has left on the world of finance.

Early Life and Education:

Nassim Nicholas Taleb was born on October 1, 1960, in Amioun, a town located in the mountains of Lebanon. Growing up in a culturally diverse environment, Taleb was exposed to a rich tapestry of ideas and perspectives that would later shape his interdisciplinary approach to finance and risk management.

Taleb’s family belonged to the Maronite Christian community and placed a strong emphasis on education. His father, Najib Taleb, was a physician and a civil servant, while his mother, Minerva Ghosn, was an artist. Their influence fostered a deep appreciation for knowledge and critical thinking in young Nassim.

In pursuit of his academic aspirations, Taleb moved to Paris, France, where he enrolled at the University of Paris to study mathematics. During his time at the university, he developed a keen interest in probability theory, recognizing its potential applications in various fields, including finance.

“Injecting some confusion stabilizes the system.”

Taleb’s passion for mathematics propelled him to pursue further studies. He went on to earn a master’s degree in science from the University of Paris-IX Dauphine, followed by a doctorate in probability theory. His doctoral thesis explored the mathematical foundations of probability and focused on the concept of randomness.

During his years in Paris, Taleb also immersed himself in diverse intellectual pursuits. He studied philosophy, particularly the works of Friedrich Nietzsche and Karl Popper, which influenced his later thinking on uncertainty and risk. Taleb’s interdisciplinary approach, drawing from mathematics, philosophy, and probability theory, would become a defining characteristic of his career.

Professional Background:

“Don’t cross a river if it is four feet deep on average.”

After completing his education, Taleb embarked on a career in finance, working as an options trader for various financial institutions on Wall Street. It was during this time that he gained firsthand experience in the world of financial markets, witnessing firsthand the limitations of traditional risk management approaches.

Taleb’s exposure to the inner workings of the financial industry, combined with his deep mathematical background, sparked a curiosity that led him to question the prevailing wisdom in the field. He was dissatisfied with the traditional models and approaches that relied on assumptions of normal distribution and failed to capture the true nature of risk and uncertainty.

Motivated by a desire to challenge conventional thinking and revolutionize risk management, Taleb began to develop his own theories and concepts that would later propel him to the forefront of finance.

Black Swan Theory:

“This is the central illusion in life: that randomness is a risk, that it is a bad thing.”

Nassim Nicholas Taleb’s Black Swan Theory is a central concept in his work that has profoundly influenced the field of finance and risk management. The theory challenges the prevailing belief that the future can be predicted based on past events and highlights the impact of highly improbable and unforeseen events on financial markets.

According to Taleb, a Black Swan event possesses three key characteristics: it is an outlier, has a severe impact, and is often rationalized after the fact. These events are rare, unpredictable, and have far-reaching consequences that significantly disrupt established models and assumptions.

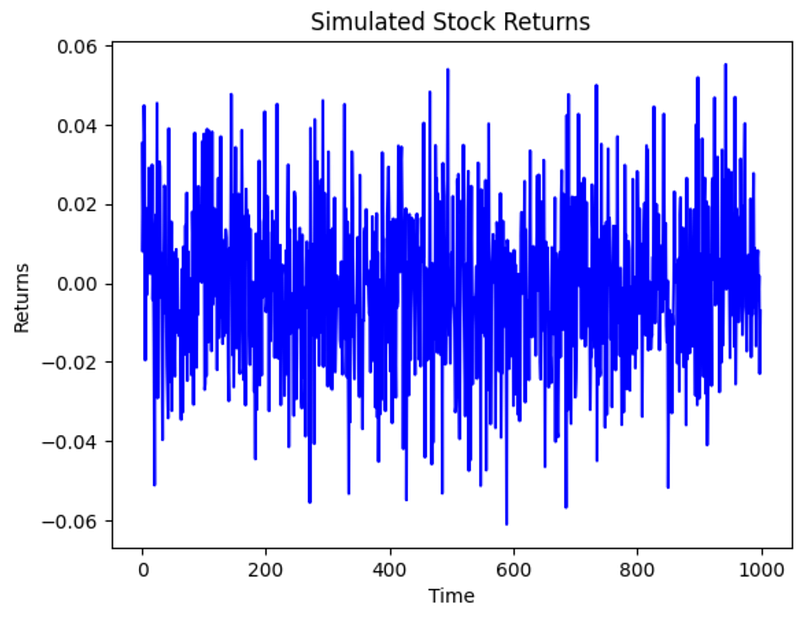

To understand the concept of Black Swan events, let’s consider an example using Python code:

import numpy as np

import matplotlib.pyplot as plt

# Simulating stock returns

np.random.seed(0)

returns = np.random.normal(0, 0.02, 1000)

# Plotting the stock returns

plt.plot(range(len(returns)), returns, color='b')

plt.xlabel('Time')

plt.ylabel('Returns')

plt.title('Simulated Stock Returns')

plt.show()

In this code snippet, we simulate 1000 stock returns using a normal distribution with a mean of zero and a standard deviation of 0.02. This represents a typical scenario where the returns are assumed to follow a Gaussian distribution, which is often assumed in traditional finance models.

However, the reality is far more complex, and financial markets are prone to unexpected events that deviate from the expected patterns. Taleb argues that these deviations, or Black Swan events, have a disproportionate impact on the markets.

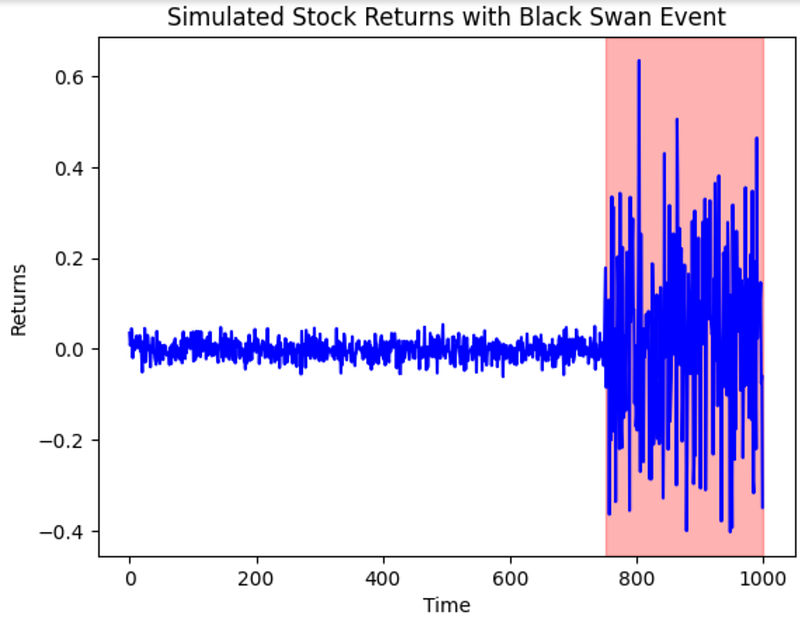

To illustrate this, let’s introduce a Black Swan event in our simulated stock returns:

# Introducing a Black Swan event

returns[750:] = np.random.normal(0, 0.2, 250)

# Plotting the stock returns with the Black Swan event

plt.plot(range(len(returns)), returns, color='b')

plt.axvspan(750, 1000, alpha=0.3, color='r')

plt.xlabel('Time')

plt.ylabel('Returns')

plt.title('Simulated Stock Returns with Black Swan Event')

plt.show()

In this modified code, we introduce a Black Swan event by replacing the stock returns from index 750 onwards with a different distribution. The new returns have a larger standard deviation of 0.2, representing a significant deviation from the expected behavior.

The resulting plot shows the impact of the Black Swan event on the stock returns. The event occurs during a specific time period (represented by the shaded red area) and leads to a sharp increase in volatility and deviation from the expected pattern.

Taleb’s Black Swan Theory highlights that traditional risk management approaches that rely solely on historical data and Gaussian assumptions fail to account for such extreme events. These events can have a profound impact on financial markets, leading to significant losses for those who are unprepared.

By recognizing the existence and potential impact of Black Swan events, Taleb argues for a more robust risk management framework that incorporates tail risk hedging, stress testing, and the cultivation of antifragile systems.

Nassim Nicholas Taleb’s concepts of Antifragility and Skin in the Game build upon his Black Swan Theory and provide further insights into risk management, decision-making, and the robustness of systems. These concepts challenge traditional notions of risk and accountability and advocate for a more adaptive and responsible approach in the world of finance.

Antifragility:

Antifragility, a term coined by Taleb, describes a system or entity that not only withstands shocks and volatility but actually benefits from them. In contrast to fragility (being vulnerable to shocks) and robustness (resisting shocks without necessarily benefiting), antifragility embraces uncertainty and volatility as opportunities for growth and improvement.

To understand the concept of Antifragility, consider the following analogy: When a bone is subjected to stress through weight-bearing exercises, it doesn’t just withstand the stress (like a robust bone); it responds by becoming stronger. Similarly, an antifragile system or individual thrives and becomes more resilient when exposed to challenges and unpredictability.

In the context of finance, an antifragile approach involves acknowledging the inherent uncertainty and randomness of markets and designing strategies that can adapt and even benefit from unexpected events. Instead of trying to predict and control every possible outcome, an antifragile mindset focuses on building portfolios, institutions, and systems that can learn and improve through exposure to diverse scenarios.

Skin in the Game:

Taleb’s concept of Skin in the Game emphasizes the importance of personal responsibility and accountability in decision-making. It suggests that individuals who have a personal stake or exposure to the consequences of their decisions are more likely to make prudent and thoughtful choices.

Having Skin in the Game means that decision-makers face the potential risks and rewards associated with their actions. This principle aligns incentives, as individuals are more cautious and diligent when their own well-being or reputation is at stake. On the other hand, decision-makers who are shielded from the consequences of their decisions may take on excessive risks or make irresponsible choices.

In the world of finance, Skin in the Game is crucial for effective risk management. Taleb argues that financial institutions, traders, and investors should have a personal stake in their investments and be exposed to the risks they take. This approach promotes better decision-making and reduces moral hazards, as individuals become more cautious and accountable for their actions.

By combining Antifragility and Skin in the Game, Taleb advocates for a risk management approach that is not only robust to shocks and uncertainty but also actively benefits and learns from them. He encourages the adoption of strategies that acknowledge the limitations of prediction and control and embrace the complex and unpredictable nature of financial markets.

Critique of Traditional Finance:

Nassim Nicholas Taleb’s work is characterized by a profound critique of traditional finance and its reliance on flawed assumptions and models. He challenges the prevailing wisdom that financial markets can be accurately predicted and controlled, pointing out the limitations of traditional risk management approaches. Let’s delve into the details of Taleb’s critique of traditional finance:

Gaussian Assumptions:

Traditional finance models often assume that asset returns follow a Gaussian or normal distribution, implying that extreme events are rare and have a limited impact. Taleb argues that this assumption is flawed because financial markets are characterized by fat-tailed distributions, meaning that extreme events occur more frequently than expected under normal distribution assumptions. Neglecting the possibility of extreme events can lead to severe miscalculations of risk.

Black Swan Blindness:

Taleb criticizes the widespread blindness to Black Swan events in the financial industry. These rare and unpredictable events have a significant impact on markets but are often neglected or underestimated due to a focus on historical data and reliance on flawed models. He argues that risk management frameworks must account for the existence and potential impact of Black Swans to avoid catastrophic consequences.

Overreliance on Quantitative Models:

Traditional finance heavily relies on quantitative models and mathematical formulas to make predictions and manage risk. Taleb argues that these models, often based on past data and assumptions of normal distribution, fail to capture the complexity and uncertainty of financial markets. He emphasizes the importance of incorporating qualitative analysis, expert judgment, and common sense alongside quantitative models to better understand risks and make informed decisions.

Fragility of Highly Leveraged Institutions:

Taleb highlights the fragility of highly leveraged financial institutions, such as banks and hedge funds, which can amplify the impact of unexpected events. These institutions often take on excessive risk, assuming they are protected by bailouts or insurance mechanisms. However, such moral hazards can lead to systemic crises and distort the true risks in the system. Taleb advocates for reducing the fragility of institutions by emphasizing the need for more substantial capital buffers and aligning incentives with long-term stability.

Inadequate Risk Management:

Traditional risk management approaches often focus on measuring and managing known risks through diversification and hedging strategies. However, Taleb argues that risk management should also address unknown risks, or “unknown unknowns,” which are typically neglected by traditional methods. He promotes the concept of tail-risk hedging, which involves taking precautionary measures against extreme events even when their probability is low. This approach can help mitigate the impact of unforeseen events and enhance resilience.

The Illusion of Control:

Traditional finance often conveys the illusion of control, suggesting that risks can be quantified and managed with precision. Taleb challenges this notion, emphasizing the inherent uncertainty and randomness of financial markets. He argues that acknowledging the limits of predictability and embracing uncertainty can lead to more realistic risk assessments and improved decision-making.

By critiquing traditional finance, Taleb calls for a paradigm shift that recognizes the inherent complexity and unpredictability of financial markets. His ideas have spurred debates and led to a reevaluation of risk management practices, encouraging financial professionals to adopt a more holistic and robust approach that accounts for Black Swan events, embraces uncertainty, and promotes responsible decision-making.