My Strategy for Saving Money and Building Wealth

Told in 3 simple steps that you can easily follow

Financial literacy should be a topic taught in every school. It’s one of the few skills that‘s universally needed by every person on the planet.

It’s also one of the biggest reason why wealth inequality exists today.

We learn how to manage money from our family, but unfortunately, if they themselves don’t have financial literacy, what does that mean for us?

To illustrate the stark difference, which of the following two do you think would come out better by retirement?

A middle class privately educated lawyer that lived paycheck to paycheck, or a working-class secretary that lived frugally?

The comparison’s not just fantasy.

Sylvia Bloom was that secretary, and despite earning a small salary in her 67 years of service, she managed to amass a fortune of more than $8 million.

21% of working American adults don’t set aside any money for their future. Don’t be one of them.

Step 1: Understand Your Finances

To succeed with any project, you need a plan.

It’s one of those things you just have to do. Without a map to direct you to where you need to go, you’ll struggle to reach your destination. But how do you go about doing that when it comes to finances?

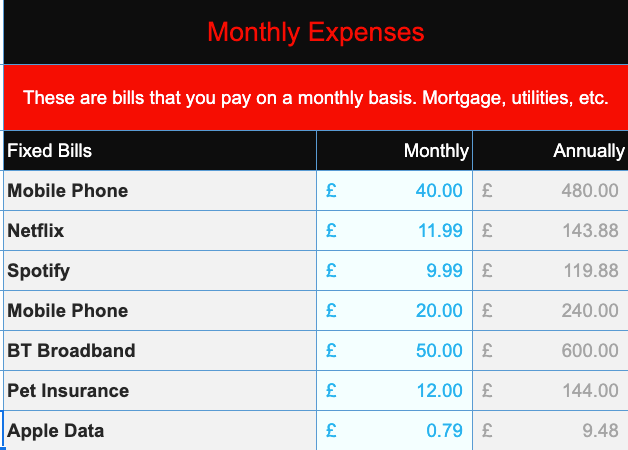

Figure out your income and expenses. Lay it all out and be honest with yourself. Do you have a surplus at the end of each month? Or are you in the negative?

I use 2 methods to track my finances which might help you get started:

What I like about budget trackers is that you can fill them out to get a snapshot of your finances. With so many free templates out there, you don’t need to start from scratch either.

It might seem cumbersome, but I promise you it’s so much easier once you have everything in one place. And it only takes a single afternoon to do.

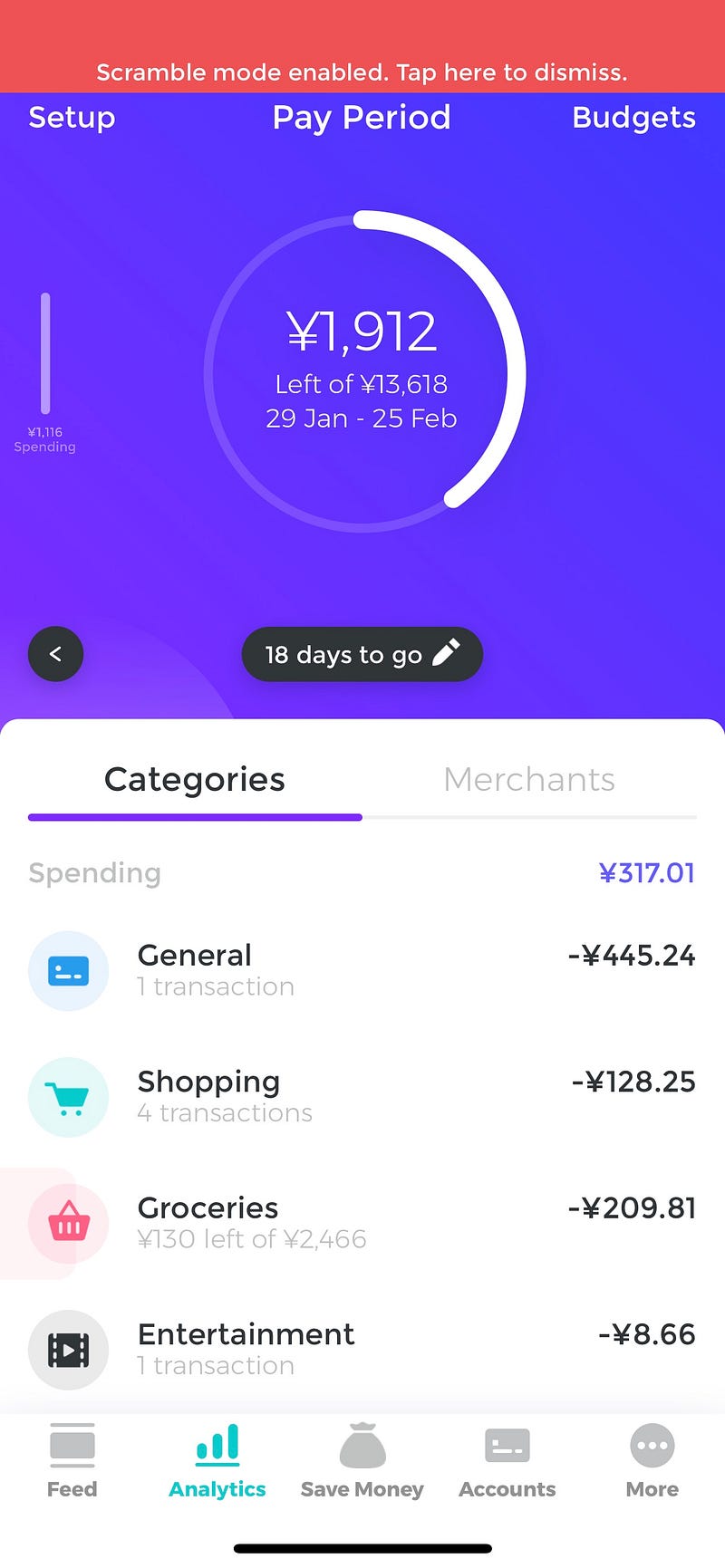

A financial tracker is great for having a summarised view, but you don’t want to have to manually input numbers every time you make a transaction. This is where apps come in to play.

A budgeting app like Emma works by connecting to your bank account and displaying the information within the app. It’s a great way to see every week where your money is going.

You can also set limits to certain categories and then track them from your phone. For example, if you’re within 90% of your grocery budget, the app will send you a notification to warn you.

Don’t get carried away with trying to fine-tune your methods of tracking and getting everything perfect though.

Remember, the goal here is to understand how much money you’re left with at the end of each month, and to increase the surplus by as much as possible, not spend weeks figuring out what colour your income tab should be.

“Do not save what is left after spending, but spend what is left after saving.” — Warren Buffett

I did this with my dad and we ended up saving 35% on our grocery bills.

Step 2: Establish your Goals

Now that you’ve got a handle on your finances, it’s time to start setting goals. Are you looking to save for a house deposit, a holiday, or just a rainy day?

Regardless of the goal, you need to consider a few things:

- What is my target amount to save?

- What % of my surplus can I afford to allocate to this?

- How long will it take to reach my target?

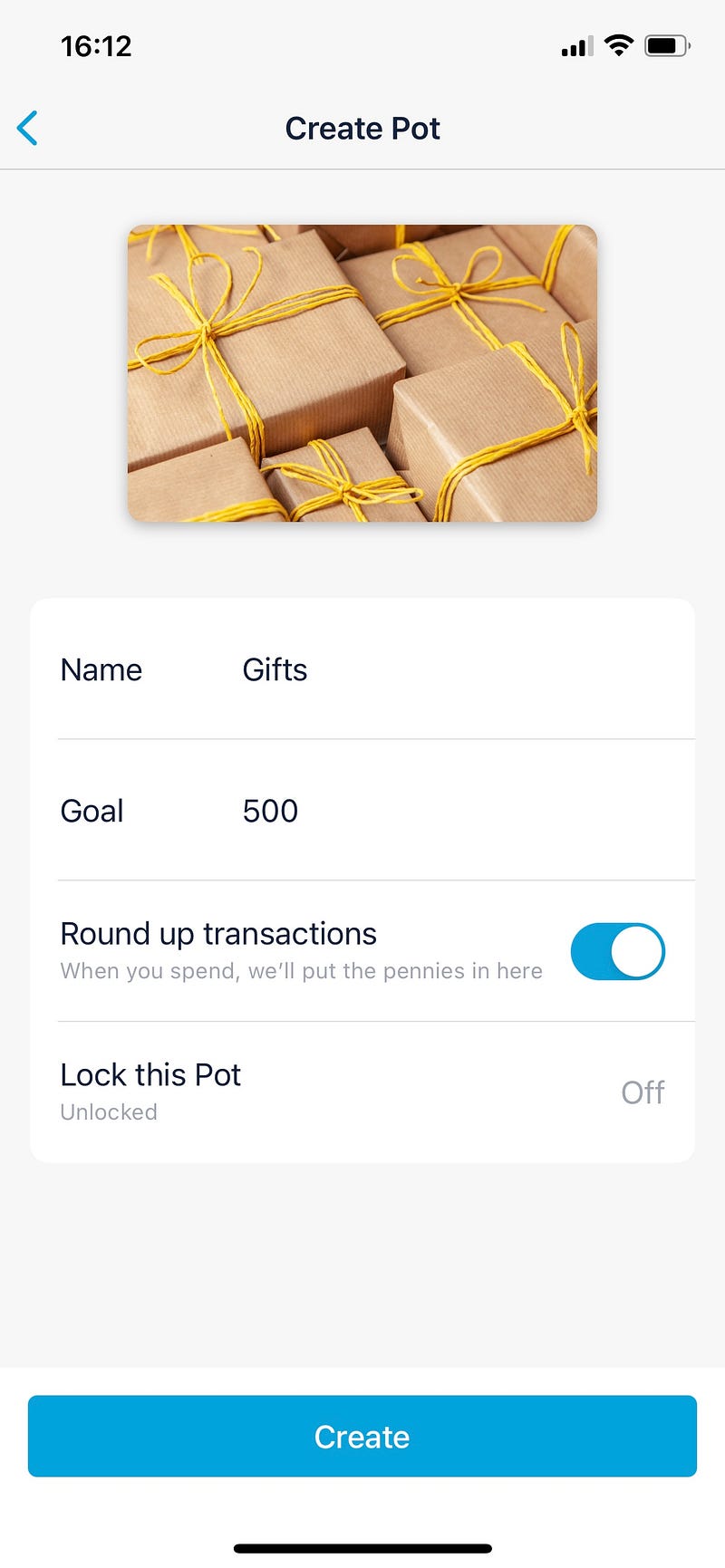

Monzo, a UK challenger bank has a feature called ‘Pots’ which allows you to allocate a certain amount of money that almost works like a mini account within your main account.

The benefit here is that you’re able to build towards that goal over time. You can even lock the pot so that you can’t access the money until after a certain date.

If you don’t have access to Monzo, you can replicate the same features by setting up a direct debit to another account instead.

Remember, the goal here is to find an affordable amount you can put away so that when the time comes, you can immediately access it rather than needing to borrow.

“You don’t have to see the whole staircase, just take the first step.” — Martin Luther King, Jr.

Step 3: Invest and Let your Money Grow

Hopefully, you still have some surplus. If not, then go back to Step 1.

Remember, the point of saving is to have a backup plan or work towards a goal. But if you want to build real wealth, you need to invest.

With the rise of free trading apps like RobinHood in the US and Trading212 in the UK, it’s easier than ever to invest and make money.

Even our hero Sylvia Bloom invested. There’s no way she would have acquired $8m by simply saving.

“How many millionaires do you know who have become wealthy by investing in savings accounts? I rest my case.” — Robert G. Allen

Investing requires research, but we live in a time where information is abundant. It’s up to you and your risk tolerance, but know that with the right decisions, you will always come out better than the savings interest rates.

My personal view would be to invest in stocks and crypto. They may be considered riskier, but they really aren’t when your view is to hold them for the long term.

The real benefit of investing comes from compounding returns. Assuming you’ve invested well, and the stock market continues to rally, you should see an average return of 8% a year.

Here’s what investing $10 with those returns would get you:

- After 1 year, you’d have around $500

- After 10 years, you’d have $7,200

- After 20 years, you’d have almost $23,000

Keep in mind, we’re starting from $0 and only investing $10 a week!

Because the more money you have, the bigger it compounds, starting with an initial investment of $1000 as opposed to $0 would result in around $27,000 after 20 years.

Investing $500 a month to reach $1m would take 35 years. But guess how long it would take to reach $2m? Only 8 years!

Building a wealth strategy doesn’t just work for young people. You can implement it at any stage.

I helped my dad create one in his early 50’s, an age when most would give up on trying to build wealth.

Unfortunately, we live in a world where instant gratification is the expectation. But money does not come instantly.

We need to grow and nurture it, and only then can we harvest its benefits.

If you want to learn more about money management, here are my 3 recommendations:

- Rich Dad Poor Dad: What the Rich Teach Their Kids About Money That the Poor and Middle-Class Do Not!

- The Naked Trader: How anyone can make money trading shares, 5th edition

- The Art of Investing: Lessons from History’s Greatest Traders

Disclaimer — Note that some of the products I’ve recommended in this story contain affiliate links