My Coast FIRE Number: $1,250,000 by the End of 2025

Can I do it?

Let’s be real — reaching $1,250,000 by the end of 2025 will NOT be easy.

I’m very fortunate that this is even an option for me, I know that, but I’ve also made a lot of tough decisions in my life to get to my current situation…and I’m not done making those sacrifices.

I need to go from $680K to $1.25M…in 23 months…or I have to keep working my full-time 9–5 job.

Escaping my 9–5 is a lot of motivation!

Here’s how I got to this point…

Review of my current numbers.

My wife and I sat down and reviewed our Coast FIRE plan this past weekend.

We have been working toward this goal for several years now.

But after some tense conversations, we realized we were not on the same page with the plan.

So we started over.

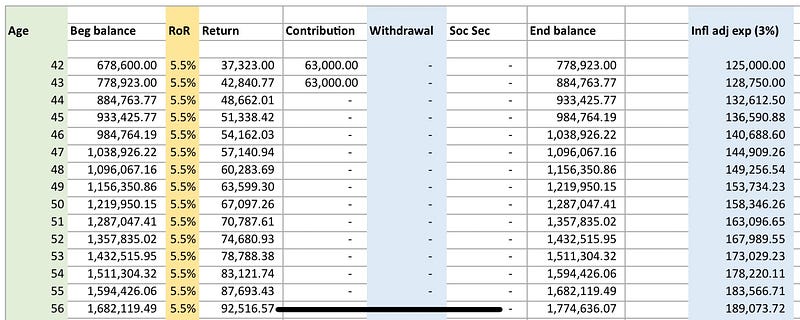

- We looked at how much we had in our retirement accounts (about $679K).

- We included how much we plan to add from our employer 401k and our budgeted taxable retirement contributions (about $63K a year).

- We determined how much (in today’s dollars) we would need to live on in the future (about $125K a year).

- We agreed upon a conservative rate of return for our investments (5.5% before inflation). This was the real sticking point for us. I’m a lot more aggressive and expect our rate of return to be closer to 7 or 8%. My wife is more conservative and wanted to use 5%. We compromised on 5.5%.

Doing the math for the future.

Pulling all of this information together was great — we were aligned and we now needed to see how that impacted our original plan.

FYI — our original plan was to reach Coast FIRE by the end of 2025 with our current 401k and taxable brokerage contributions only.

To visually see the math at a high level, we started a worksheet. Plugging in our numbers, percentages, estimations, future earnings, conservative Social Security payments, inflation impact on our annual living cost, and a rough estimate of how long we’ll live.

I like to plan on living to 100, but the odds are slim. The average life expectancy for a man in the U.S. is now 73!

The math wasn’t good — mostly because our original plan included a larger rate of return on investments.

Sticking with our current plan we’d run out of money (approximately) in our late 70s.

That would work if we live to only the average life expectancy, but I’d rather plan on a bit longer.

Determining our new number.

We started playing around with the numbers.

Investment gains will fluctuate (wildly) from year to year, but we need to use averages and estimates to get any planning done with money.

But how much additional money would we need to contribute to still reach our Coast FIRE by the end of 2025?

The answer:

$280,000

This would bring our investments to approximately $1.25M, allowing our money to last until we die.

Making extra money isn’t easy.

Reaching our (new and improved) Coast FIRE number will not be easy.

- We both already have decent-paying 9–5 jobs.

- We both already max out our 401K contributions and budget an additional $1400 a month for retirement.

- We both already practice intentional spending, regularly reviewing and updating our budget.

To be transparent, we didn’t include the appreciation value of our townhome in our current net worth, but we did include it in our estimates for reaching $1.25M — so we still need $280K of additional income.

But making money on the side isn’t impossible — there are so many ways to make money outside of our 9–5:

- Selling items around the house (and stuffed in the garage) that we don’t use or don’t bring us value.

- Pet-sitting, DoorDashing, and starting an Instagram account for our ridiculous-looking dog.

- Even writing on Medium.

Let’s get creative!

The positive that will help us reach the goal?

We’re both on the same page with our goal now…and that’s encouraging!

A shared plan, that everyone is working toward, with a defined amount and timeline.

We can conquer anything together.

Now we need to get creative!

I guess being “scrappy” turned out to be the perfect 2024 word.