Mortgage Borrowing — Part 3. Reimagine How You Spend Money to Benefit YOU, Not Your Lender

In the first 5 years of a 7%, 30-year fixed mortgage, everything else you buy just became 5 times more expensive—leverage it to benefit you!

Related

• Mortgage Borrowing for YOUR Benefit (1. Pay Less Interest) (2. Interest Savings Over First 5 Years) (3. Reimagine How You Spend Money to Benefit YOU, Not Your Lender) • 4 Lessons on When to Sell $400,000 Worth of Stock • Is the Stock Market Really in a Bear Market? Maybe. Maybe Not. • When Is a Stock Market Crash Not Really a Stock Market Crash?

Recent

• 2 Reasons Populations Are Collapsing in Developed Countries • The Deafening Silence on Stock Buybacks from Centrist Democrats • 3 Key Facts Everyone Is Missing About Biden’s Student Loan Debt Relief

Potential to Change the Way You Think

• Why Are Fundamental Human Values Critically Important for Successful, Enduring Brands? • Life Expectancy vs. Healthcare Costs in the U.S. (and Japan, Germany, France, Spain, Portugal, etc.) • Why Vote “Blue No Matter Who” If Centrist Dems Never Play to Win?

There is a different way to think about your mortgage payments that is far more beneficial to YOU than what everyone else in the mainstream media, in the mortgage lending business, and on Wall Street has been telling you all of your life.

For the first several years of a 30-year fixed-mortgage at 7%, everything else in your life just became 5 or 6 times more expensive.

As mortgage interest rates get above a certain level — and in September 2022, we are “there” already — it’s VERY much in the interest of anyone borrowing money to buy a house to change their mindset about their mortgage and the money they owe.

And when I say change mindset, I mean do a total paradigm shift.

The Key Insight

Instead of worrying about “how much I pay each month for my mortgage,” we will instead focus on “how much I can save over the life of the mortgage?” and “how large an extra nest egg of cash I can create by the end of the mortgage?”

Here’s why.

As we already covered in the first two articles in this series, the monthly mortgage payment is $2,661 for a

- 7.00%

- $400,000

- 30-year

- fixed-rate mortgage.

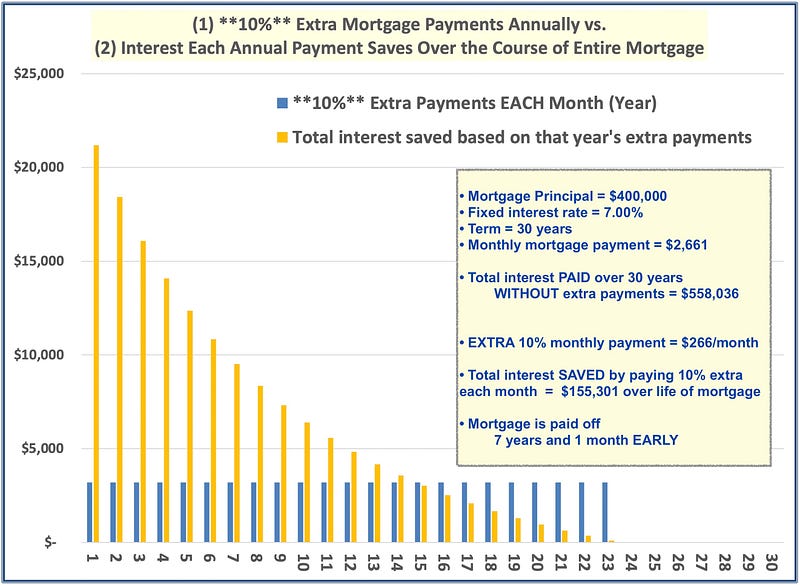

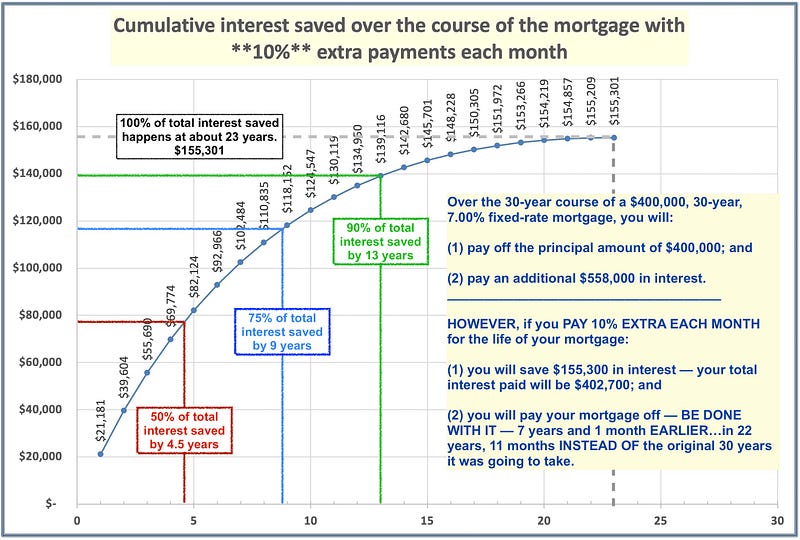

Over the course of this example mortgage, you would pay $558,036 in INTEREST in addition to paying back the original principal amount of $400,000.

But if you pay an extra 10% each month on top of the $2,661 payment — i.e., an extra $266 — then you will not only pay off the mortgage about 7 years earlier, you will pay $155,301 LESS in interest over the now-shortened life of the mortgage.

Essentially that’s an extra $155,301 less that you will pay your mortgage lender and $155,301 more that you will have in your own pocket.

We know from the chart in the first article in this series ((Part 1. Pay Less Interest) Turn Mortgage Borrowing Around to Benefit YOU) that the amount of interest you save is greatest in Year 1 of the mortgage and smallest in the last year of the mortgage.

For convenience, here is that chart again:

- The orange bars are the interest you save each year.

- The dark blue bars are the extra 10% payments ($266/month or $3,193/year) you are making each year.

- You can see how the orange bar is highest in Year 1, while the orange bar for Year 23 is so short you can barely see that tiny little orange “nub” in the column for Year 23.

Let’s do a quick example.

Imagine that we are going to make extra payments for ONLY YEAR 1 of the mortgage.

For every year after Year 1, we won’t make any extra payments. But for the 12 months in Year 1, we will pay an extra $266.10 each month.

How much do we then save over the life of the mortgage versus what the extra payments for Year 1 cost?

- Cost of extra payments = $266.10 x 12 = $3,193

- Savings in interest over the lifetime of the mortgage = $21,181

- Ratio of interest savings to extra payments for Year 1 = 6.6

That means for every $1.00 extra you pay in Year 1, at the end of the mortgage (20+ years later), you will have $6.60.

Another way to think about this is that you get the most bang for your “extra payment” buck in Year 1.

The bang for the buck (or “ROI”) is still pretty good in Year 2 and Year 3, but not as good as it was in Year 1.

And the ROI for each year keeps decreasing every year after that.

By the time you get to Year 13 or 14, it really doesn’t make that much sense to keep making the extra 10% payments since you will have already locked in 90% of the maximum total savings you could get if you made extra payments all the way through.

Now on to the Key Insight that will change the way you think about your mortgage payments

There are 3 parts to the key insight:

Part 1. When you make extra payments, you save more money over the lifetime of the mortgage than you put in with those extra payments.

We just covered this.

Part 2. The earlier you make the extra payment, the more money you save.

We just covered this, too.

Part 3 is the new “mindshift”

When you have an opportunity in Year 1 to save $6.60 for every $1.00 extra that you pay to the mortgage, then you have to think about every other nonessential expense in Year 1 as having the same trade-off.

For instance, if you are going to take the family out for pizza and a movie, and the out-of-pocket cost for the evening will be $100, then the real cost of that movie and pizza night is NOT $100.

The real cost is the $660 that you could have at the end of the mortgage.

Does that make sense?

If you take that $100 in Year 1 of the mortgage and pay it toward the mortgage, you will end up paying $660 less toward your mortgage over its lifetime.

Or, said another way, YOU will have an extra $660 by the end of the mortgage.

Same thing if you spend $1500 upgrading to a new smartphone 1 or 2 years earlier than is really necessary.

Now, I’m not saying that you should live an entirely Spartan, joyless life for the first several years of your mortgage . . .

. . . but I am saying that if getting a guaranteed 660% return on any extra money you want to put towards your mortgage is important to you, then you get by far the biggest bang for your “extra payment” buck in the first 4–6 years of your 30-year mortgage.

Become your grandparents or great-grandparents for a few years.

Break legs to pay every extra dollar you can in that first year.

Yes, I am telling you — to whatever extent you’re not already doing this — to start being a total hard-ass about non-essential spending.

Put off clothes shopping if you can. Combine trips by car so that you can save gas money. Be extra savvy and extra frugal with how you spend money.

You have a huge financial incentive to behave this way in the first several years of your mortgage.

I will go a step further now.

Because you get such a high rate of GUARANTEED return in the first few years of the mortgage, that means that any extra paid work you do is worth a lot more if the money you earn goes toward making extra payments on the mortgage.

If you’re getting paid, say, $50 per hour for a side gig in Year 1 of your mortgage and you pay that earned money toward your mortgage, it’s correct to think about that as you earning $330 per hour . . . although you won’t actually collect on that $330 per hour until the end of your mortgage.

But that $330 per hour is guaranteed. Zero risk. It IS going to happen . . . as long as you pay that “$50 per hour” toward your mortgage as extra on top of your regular monthly payments.

I’ll go yet one more step further.

Put your kids to work, too.

If you have children, then this is a family affair.

If your children are old enough, make sure they are out there mowing every neighborhood lawn they can during the summer and shoveling every driveway they can in the winter to earn extra money.

Just be sure to put some significant portion of that money earned toward the family’s mortgage.

The whole family benefits from this.

Bottom line, the most important thing is to make a conscious decision about whether having $100,000 to $200,000 extra in your bank account by the end of your mortgage is a good tradeoff for YOU vs. making extra payments on your mortgage for the first 5–13 years.

If it is a good tradeoff for you, then do it.

Don’t be dissuaded by CNBC or Fox Business or Wall Street Journal talking heads who will tell you “saving money” or paying extra on your mortgage isn’t as smart as investing it.

They will try to make you think that only chumps do that.

Those assholes are talking their book. THEIR book.

Not yours.

Related

• Mortgage Borrowing for YOUR Benefit (1. Pay Less Interest) (2. Interest Savings Over First 5 Years) (3. Reimagine How You Spend Money to Benefit YOU, Not Your Lender) • 4 Lessons on When to Sell $400,000 Worth of Stock • Is the Stock Market Really in a Bear Market? Maybe. Maybe Not. • When Is a Stock Market Crash Not Really a Stock Market Crash?

Recent

• 2 Reasons Populations Are Collapsing in Developed Countries • The Deafening Silence on Stock Buybacks from Centrist Democrats • 3 Key Facts Everyone Is Missing About Biden’s Student Loan Debt Relief

Potential to Change the Way You Think

• Why Are Fundamental Human Values Critically Important for Successful, Enduring Brands? • Life Expectancy vs. Healthcare Costs in the U.S. (and Japan, Germany, France, Spain, Portugal, etc.) • Why Vote “Blue No Matter Who” If Centrist Dems Never Play to Win?

Want me to cover a topic? Please post suggestions in the comments, and I’ll use your input to help prioritize my writing and research.

If you appreciate my writing, please share it on social media.

Want unlimited access to all Medium articles? Become a member!

Again, thank you for reading, subscribing, clapping, and sharing — your time and attention are deeply appreciated!