Mission Retire Someday: I’m blogging everyday until I’m out of debt.

Turns out we don’t have to spend our whole lives in debt afterall.

In February 2024, my husband and I embarked on what we call Mission Retire Someday. And by me, I mean I. My husband is not the one who comes up with cutsey names for everything. Thats me.

Anyway, Mission Retire Someday because — we want to retire someday. And by we I mean both of us.

The goal is to pay off all of our debt and then save enough money to be able to retire in fifteen years. We’re too old and broke to retire early. I’m 52 and Kevin is 55. But we can still retire well when I’m 67 and he’s 70.

Phase One of Mission Retire Someday involves paying off all our debt, including our mortgage. I’m blogging everyday to make extra money to add to our repayments every month.

Here’s how February 2024 went.

We confronted some hard truths.

I have been extremely poor in my life. Extremely. Dad in prison, single mom, food insecurity, couch surfing poor. And I’ve built my whole life around my strong desire to never be poor like that again.

I’m going to be uncomfortably transparent below with my finances. And with how embarrassing and upsetting this all is.

We have enough money. Or we should. You’ll see below that it costs nearly $5000 just to service our debt (that’s our mortgage, car payment, and unsecured debt.)

That’s nearly $60,000 a year, before things like utilities and food. I’m going to spend sometime, during this mission exploring how in the world I got to this place. Technically, the problem is that we don’t actually have enough income to pay $5000 a month on debt and then also buy groceries, put gas in our car, keep the lights on, and go to an occasional movie or something.

So we use credit cards to make up the balance.

My husband has never been poor and never not been in debt. I know better, though. I know what it means to be underwater. And I’m frankly shocked that I’m here again.

It’s felt for a few years like no matter how much money we earn, we’re barely treading water. And debt is why. Not only are we paying to live today, we’re also paying for living in past years. And it’s finally come to a head.

I know that it’s an extremely privileged place to come from, even being able to pay $5000 a month to service debt. We are not poor. We’re solidly middle class. A two-income couple with two adult children, one kid in college, and my husband’s mother (who has Alzheimer's and lives with us.)

We are typical sandwich generation, Gen X people with a whole lot of privilege. We’ve been living just a little outside our means for so long. Drowning by centimeters, until we’re barely treading water.

Here’s how our first month of Mission Retire Someday went.

We used Undebt.it to make a plan.

This was actually quite an ordeal. We organized every debt and inputted them into Undebt.it’s system. That’s every credit card, a personal loan, a car loan, and our mortgage.

(Undebt.it is free. I really researched what system to use to keep all of this organized, and this was the one that came most highly recommended. I’m not an affiliate or anything — this is just what we used.)

We didn’t add my student loans in. The interest on that is extremely low and I’m on an income-based repayment plan. For now, we’ll just keep making the minimum payment.

Everything else went in.

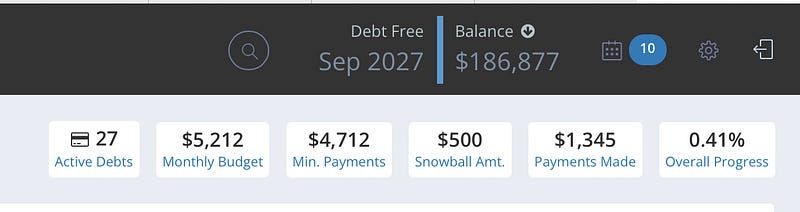

So, we’re $186,877 in debt, including our mortgage. We’re already paying $4,712 a month to pay the minimums. (The payments made you see on the right are the payments we’ve already made in March. Our mortgage payment, mostly.)

If we add in $500 a month from my daily blogging, that brings the total up to $5212.

That was — I’m not going to lie — more than a little scary to look at.

But look up at the top there — our debt free date if we follow the plan is September 2027. That’s three and a half years.

What?

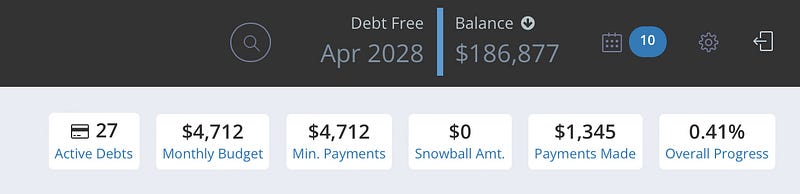

And the best part is that here’s what happens if we don’t put the extra $500 snowball amount in.

Our debt free date moves to April 2028. Making that extra payment will get us out of debt eight months faster, which is cool. But even if all we do is pay EXACTLY what we’re already paying every month right now, rolling the amounts from paid off accounts into the debt snowball, we’ll be out of debt in just a touch over four years.

That’s exciting. Really exciting.

The reason it’s so fast is because in the next year we’re going to pay off a personal loan and a car loan that will add nearly $1500 to the snowball. That will get the rest of the debts paid off quickly.

Eventually we’ll spend about a year paying $5212 toward mortgage every month.

We’ll think about some things later.

We bought our house at a time when interest rates were very low. Our interest rate is 4 percent. As much as I would like to get our mortgage paid off, we might decide, when it comes down to it after everything else is paid off, to put the extra money into savings instead.

I’m pretty sure it wouldn’t be too hard to put our money into some kind of super safe savings account that would earn more than 4 percent interest. Saving that money and then putting the interest toward paying our house off faster might make more sense.

Ultimately, I don’t have to know everything right now. It will take two years to get to where our mortgage is our only debt. We can reevaluate then.

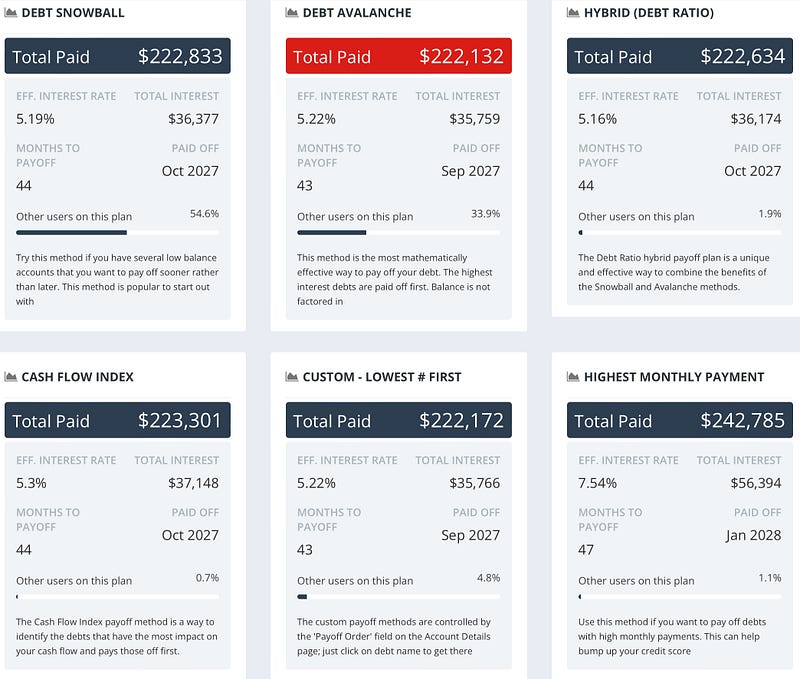

We’re doing a debt avalanche.

Undebt.it has several repayment plans to choose from. We’re going with the Debt Avalanche because it gets us out of debt the fastest (just by a month though) and costs the least overall.

Basically, a debt avalanche has you paying down the debt with the highest interest rate first. A debt snowball means paying off the credit cards with the lowest balances first, so you can start seeing results faster.

We’re paying $35,759 in interest, even paying things off early. I’m kind of glad we can see that so starkly, because it pisses me off enough to keep me on track.

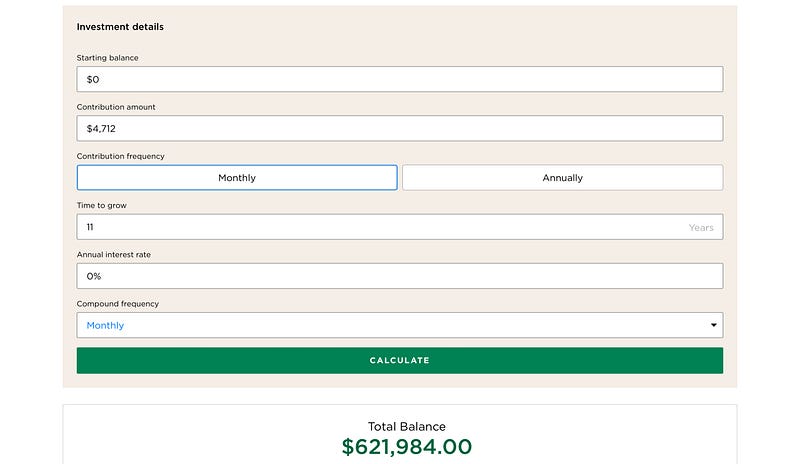

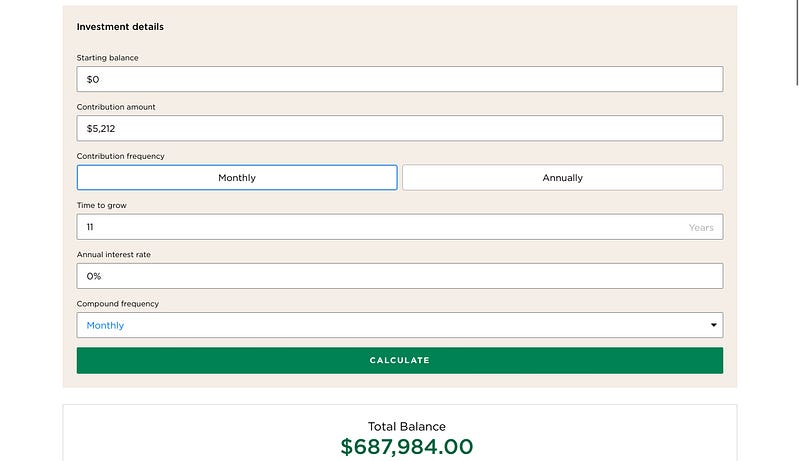

I went over to Nerd Wallet’s savings calculator and looked at what would happen if we saved that $4712 a month for 11 years — to bring us up to 15 years.

This is without interest at all and starting from a zero balance.

And here’s what happens if we save $5212, or an extra $500, for 11 years.

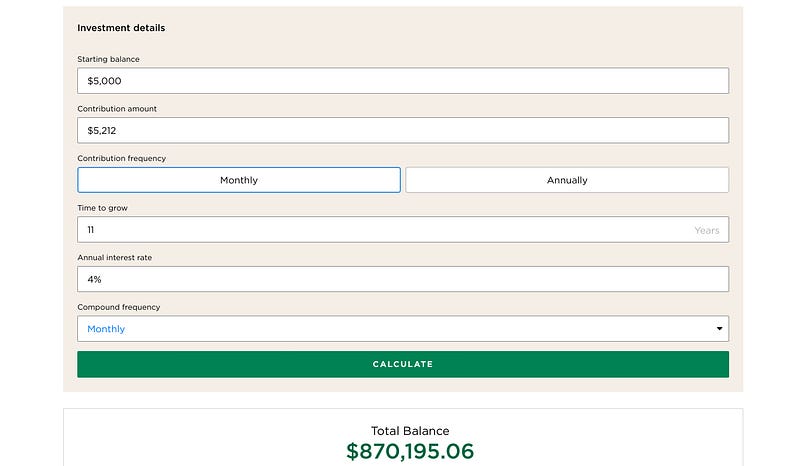

And — just for kicks. If we save $5212 a month for 11 years and put the money somewhere that earns 4 percent interest and manage to save $5000 before we start.

And that’s why this is Mission Retire Someday. If we were debt free and managed to save that much money, we could actually retire someday.

We’re working on building up some savings, too.

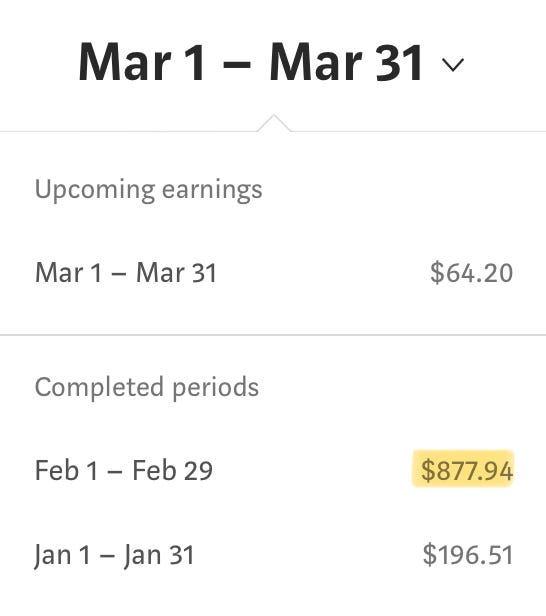

I earned $877.94 blogging in February. This was a marked improvement over January. Mostly because I actually blogged in February. I only published once in January.

The February earnings go toward March’s payments. Initially, the plan was to put whatever I earn blogging into the debt snowball. But we decided to stick with $500 — and any extra will go into our savings account.

In March, we’re going to put $500 toward our debt and $377.94 in savings. That will let us pay off one credit card with a low balance and a $40 minimum payment.

Next month the debt snowball/avalanche/whatever will be $500 from blogging and that $40, or $540. We’ll pay off another credit card with a $35 payment. So in May we’ll have $575. And so on.

We stopped using our credit cards.

We didn’t use any credit cards in February. That forced us to evaluate our finances and be much more mindful of how we spend our money. Because while we can make those minimum payments and keep food in the fridge and the heat on, it’s by the skin of our teeth.

Part of why we decided to put anything over $500 into savings is so that money is there if we need it, instead of turning to a credit card.

Shaunta Grimes is a writer and teacher. She is an out-of-place Nevadan living in Northwestern PA with her husband, three superstar kids, King Louie Baloo the dog, and Ollie Wilbur the cat. She is the author of Viral Nation, Rebel Nation, The Astonishing Maybe, Center of Gravity and Here I Am. She is the original Ninja Writer.

Sign up for her Substack newsletter, Then See What Happens.