Be Smarter Than Me: Mint Financial is Shutting Down— Top 2 Picks for Budgeting Apps

Don’t be dumb like I was, and do track your money. In this article, I review the top two budgeting apps I’ve used so far, including pictures!

With the digitization of everything, it’s easier now than ever to automatically track spending and monitor your budget.

If you’re not someone who regularly tracks their spending or you’re trying to pay off debt (or both), I highly recommend you start this vital habit at least every other day.

Quick reason why? Here’s a story from my naive youth. You can skip this part if you already track your money and want to see the app recommendations.

I was poor when I didn’t track my money despite making almost six figures in my early 20s

Despite having a good job, I was broke as a result of not monitoring my spending, and honestly just being plain arrogant.

The first year I started working after college, I didn’t track my spending in any way, shape, or form except when I logged into my accounts right before payment was due.

After paying for rent, insurance, phone, groceries (not to mention my groceries would go bad anyway), electricity, water, internet, gas, new clothes, dining out, happy hours, and a plane ticket to Europe… how could I not have enough cash to pay my balances??

I told you I was dumb. Don’t be like me.

I completely underestimated the cost of living in the real world and didn’t have enough cash to pay the full balance.

Thinking I couldn’t live like this forever, I quickly started tracking my spending using Mint, a free budgeting software, which was much more reliable back then.

Now we’ve covered an example of stupidity in my youth, let’s talk about budget apps!

I’ve tried many budget apps, and today I’ll share the two I recommend most.

No, it’s not Mint ❌

I loved Mint when it was first released and used it for over 10 years. As the title suggests, Intuit’s Mint financial is shutting down on January 1, 2024. Some features will transfer over to credit karma.

The announcement is likely leaving savvy budgeters puzzled as to what they’re going to use now.

- I downloaded Credit Karma yesterday, and it’s still strictly a credit reporting app. Not a bad thing, but I have yet to see the new budget features.

A reminder to all of us that sudden shutdown is a risk with using any app.

Heck, Medium is no exception.

With so many choices, I narrowed down to two apps based on these criteria:

- User interface

- Speed

- Connectivity to financial institutions

- Cost

- Similarity to Mint (Mint’s success was for a reason, and users who are acclimated to Mint’s features will transition easier to similar apps)

In the next section, I get straight to the point and list my top two along with any costs.

My Top 2 Financial App Choices

- Monarch Financial ($8.33 a month as of November 2023) www.monarchmoney.com

2. Empower (free) www.empower.com/

- I pick Monarch over Empower because of its intuitive user interface and easily customizable budget features. It is similar to Mint but faster. The associated cost seems high but it comes with dedicated customer service.

- Empower is great for tracking investment performance, with some budgeting features. The user interface is different from Mint and does not have many customization options, which makes it difficult for users who like Mint’s interface. However, I noticed Empower is better at connecting to financial institutions than most apps I’ve used. It’s the only app able to connect to my AMEX Checking account.

- I list the pros and cons for each app in the later sections.

- But first, some runner ups!

Honorable mentions:

3. NerdWallet (free) — I actually think this is a better option than Empower for most people. BUT feel it is equally not a great Mint alternative due to its limited customizable features. For example, I can track cash flow (cash coming in and out) but cannot create my budgets. Unfortunately, I only briefly tested NerdWallet, so my input is limited.

4. Simplifi Quicken ($2.99 a month as of Nov 2023) — I’ll be honest. I don’t trust the Quicken brand after wasting $200 subscribing to the original Quicken Classic desktop/cloud version, twice. However, it’s probably the most similar to Mint and the monthly fee is lower than Monarch. Quicken was originally developed by Intuit but was sold off in 2016. Its similarity to Mint and low subscription fee is why it’s on my list.

If you have other apps you like or feedback on the apps listed, I’d love to hear it!

By the way, I’m not sponsored and will not include any referral links. It’s ultimately important the best apps get people’s attention.

Next, I’ll go through the pros and cons of the top two picks.

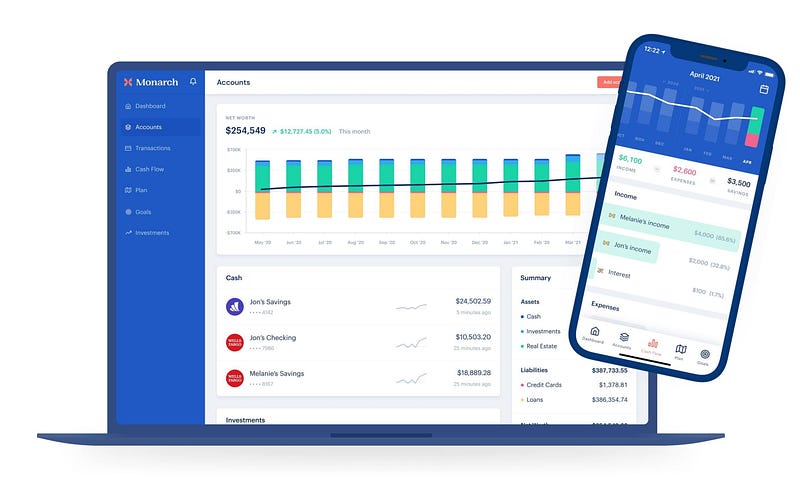

Monarch Financial

Monarch Financial is my favorite. It’s easy to use, fast and cloud-based.

Pros:

- Accessible via app and web versions.

- Transactions update quickly.

- Minimal screen lag compared to Mint.

- Strong customer support feature, easy to report issues.

- Strong transactions filter feature, can filter and sort by multiple criteria such as category and account.

- Easily customizable budget features, with the ability to create custom spend/income categories.

- Great for tracking investments, especially cryptocurrency. For example, Coinbase balances update instantly. Mint’s investment feature was never accurate for me, I would track manually or refer to Empower.

- Multiple connectivity options to sync to financial institutions

- Ability to load in bulk .csv files to correct balances or fix accounts with missing history, a feature Mint did not have (you were SOL if the account didn’t load properly)

Cons:

- Connectivity can be an issue, unlike Mint, Monarch has a hard time overcoming accounts with two-factor authentication. Despite having multiple connection options, I often have to refresh these connections manually to see new transactions.

- It is expensive, about the same cost as some streaming subscriptions.

- Does not show credit score, unlike Mint, users will have to rely outside the app to get regular updates on credit.

Now that we’ve covered Monarch, let’s go through the pros and cons of Empower.

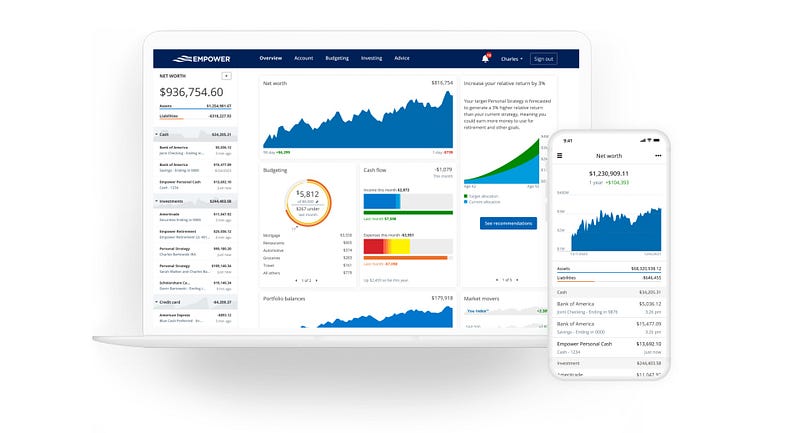

Empower

Empower is an investment and retirement tracking tool with some budgeting and notification features.

Pros:

- A wide array of financial institutions to connect to.

- Connections are reliable, not as many frequencies of accounts disconnecting compared to Mint or Monarch.

- Great for tracking investments, provides an opinion on your portfolio’s risk exposure.

- Accessible via app and web version.

- The budget feature is simple.

- Ability to track cash flow.

- Easy to update transactions.

- Tracks spending patterns over time and can send email notifications to let you know if you’ve spent more or less than last month.

- Can see credit scores.

- Will refund if data in app causes users to overdraft.

- Best of all, it’s FREE!

Cons:

- It’s more focused on tracking investments and net worth than spending.

- The budgeting feature is limited.

- It’s hard to customize budget categories.

- Many hard sells of their financial advisory services (they have to make money somehow, right?)

- The user interface is not as intuitive as Mint.

Have you tried any of these apps before? Let me know what you like or don’t like about it!

I’ll end this post with some data points and parting thoughts.

Tracking spending is a fundamental habit if you want to get rich and stay rich

Now that we’ve reviewed the apps, I want to point out some relevant but startling statistics.

- Three out of four people I meet do not track their spending or budget consistently. However, a quarter of the same group doesn’t track spending due to being in the top 2% of earners, where money isn’t an issue-coinciding with the next data point.

- 51% of Americans live paycheck to paycheck. Tracking your spending to ensure a surplus of funds each month is crucial to getting out of this cycle.

I used to be one of those people. Don’t be that person.

A little over 55% of Americans do not use a budget to manage their hard-earned income, according to a new survey by The Penny Hoarder.

A similar 56% hours of survey respondents said they didn’t know how much money they spent last month.

Needless to say, this is a problem, especially with how the cost of living has risen dramatically in the US.

It’s no wonder so many people, even earners making over $100,000 annually, live paycheck to paycheck.

Over time this causes debt, as expenses must be paid from somewhere. If not through credit cards, then from personal loans from banks or even family and friends.

This is how credit card companies get you. Don’t let them win!

Conclusion

Deciding on a tool to help you get money-smarter can be overwhelming, but it’s worth the research.

In my experience, picking an unsuitable app for your budgeting needs is an immense time suck. Why?

- It takes time to connect your accounts

- It takes time to load the data

- It takes willpower to even get started

I’ve wasted so much time and energy testing out different apps until I found one I liked. I worked with spreadsheets all day so managing my finances on a spreadsheet was unsustainable.

It’s important to start with as few obstacles as possible when onboarding these apps.

In this article, we reviewed my top choices, Monarch Financial and Empower.

With the amount of software out on the market, there’s no one-size-fits-all solution. Picking the right budgeting tool will be based on your needs and how much you’re willing to spend.

Who needs another subscription, right?

But this is a critical subscription, perhaps more valuable than Netflix or Hulu.

Who knows, like 51% of Americans, you might be overspending your income.

A tool like the ones we reviewed can help you gain a solid grasp of your finances.

Hopefully, this article helped provide some data points for you.

And if you’re a soon-to-be ex-Mint user, I wish you the best of luck with the transition!

My passion is to help others discover their wealth. I grew up in deep poverty and conquered serious financial challenges to have a normal life. I eventually saved enough cash to quit my job and kickstart my own consulting firm, where my clients vary from mid-large organizations. Through Modern Money, I share money tips, education, and career advice. I hope even one tip can make a difference for others. 💰✨

This article is for informational purposes only and should not be considered financial or legal advice. Consult a financial professional before making any major financial decisions.