Medicinal Cannabis in Australia

Introduction

This report is a guidance document to navigate the complex commercial landscape of Medicinal Cannabis in Australia (Cannabis for clinical research is not covered). The contents of this document might be useful for someone who is in the Cannabis industry, looking to start a Cannabis related business or someone who is just interested in the Cannabis industry. The information presented is based on my interactions with government officials & industry representatives, web research, and networking at industry events such as CannaTech. Through my research and interactions, it is evident that current information pertaining to the Medicinal Cannabis is fragmented and both industry professionals and government officials are still not well-versed with it. For example, recently, I had to speak with six different government agencies including the state police just to understand ‘what are the vehicle requirements to transport Medicinal Cannabis in Australia’. Another government official, I spoke with recently regarding imports & distribution quoted “The regulation in the Cannabis industry is not all red or green, there are a lot of grey areas”. This siloed and difficult to interpret information is counterproductive in terms of operating an efficient Medicinal Cannabis supply chain (be it for someone who is already in the industry or a new entrant).

The aim of this report is to break those silos and merge the information in a coherent manner — Consider a hypothetical scenario — Let’s assume that Mr. Green would like to start wholesaling Cannabis for medicinal use in NSW (New South Wales). Now, how would he ensure that his business model complies with government regulations? How might those regulations constrain or grow his business? This document can be used as a springboard to help answer such questions. For readers wanting more detail, it will help them begin their research by pointing them in the right direction.

The following topics are covered -

- The regulatory framework of medicinal Cannabis in Australia

- Medicinal Cannabis Supply Chain & Distribution pathways

- Forecasts — No. of patients, domestic demand, domestic production, imports & exports

Regulatory Framework

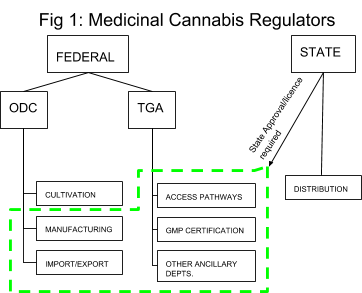

In Australia, medicinal Cannabis is regulated both at a federal level and a state/territory level. At the federal level, The Department of Health regulates medicinal cannabis products through -

- The Office of Drug Control (ODC), which administers the Narcotic Drugs Act that regulates controlled substances (medicinal Cannabis is a controlled substance)

- The Therapeutic Goods Act (TGA), which administers and regulates, amongst others, the quality, safety, and efficacy of medicines as well as access to medicines that have not been approved for general use (not clinically tested).

At a state level, each state has a role in medicine scheduling and stipulating medical conditions for which medicinal cannabis can be used as treatment by patients in their jurisdiction ( TGA advises five types of patient groups for which medicinal Cannabis can be recommended as a treatment). Additionally, each state has controls around the distribution of medicinal Cannabis.

Both the ODC and TGA are further divided into more specialized departments as shown below (Fig-1).

To explain how these regulators & departments work in tandem, let’s get back to Mr. Green’s wholesale business. Mr. Green’s business is to import finished Cannabis product from Canada and wholesale that product in NSW. In order to do so, he would need a license & a permit by the import/export department of the ODC for the product to cross international borders as well as wholesale distribution license from the state of NSW to supply the product domestically. Additionally, the company from which he is importing is required to comply with TGA’s manufacturing standards. For someone like Mr. Green to understand the regulatory requirements, since there is no centralized point of contact within the government, he would have to get in touch with each government agency separately and within each agency, the correct department e.g. import/exports department in the ODC will not be able to guide Mr. Green on wholesale distribution.

As one might appreciate from the above example that gathering information regarding the cannabis industry is time-consuming and can cause long delays in the application & approval process.

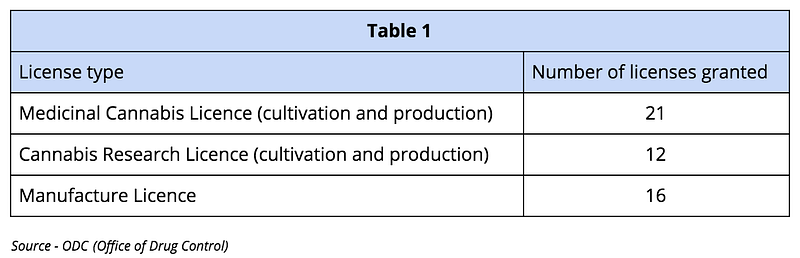

Even though it has been two years since legalization (cultivate & manufacture), only 49 Cannabis related licenses have been issued (refer to table 1 below). Since some companies hold more than one license the actual number of companies that are engaged in cultivation and manufacturing of Cannabis is lower.

At a recent conference in Sydney, John Skerritt, the deputy secretary for the Australian Department of Health mentioned that the processing time for any new license application is currently more than six months. This is because the government has received more than 180 licenses applications (higher than expected) and are running at a 6-month backlog due to inadequate staffing. Moreover, getting a license is only the first step to establish a cannabis cultivation or manufacture business. To actually start operations each company requires a permit from the government. Presently, as reported by Australian media, only three Australian companies have a permit to grow — Little Green Pharma, Cann group, & Medifarm.

Medicinal Cannabis Supply Chain & Distribution Pathways

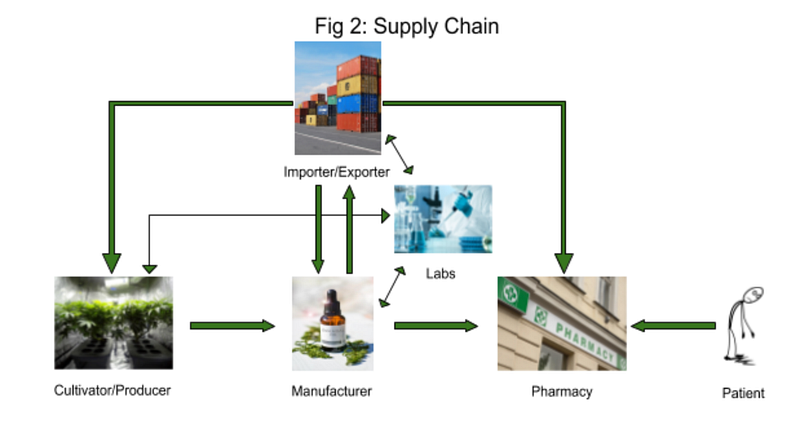

To understand how the regulations impact distribution pathways, it’s useful to have the picture of a medicinal cannabis supply chain in mind (Refer to fig 2 below).

A patient can buy cannabis via a pharmacy through different access schemes (discussed later in this paper).

The pharmacy can receive supply a finished cannabis product (such as oils, capsules, etc.) from either a domestic manufacturer or import finished product from overseas.

The manufacturer can receive the supply of harvested crop from a domestic cultivator or import semi-finished products from overseas (a manufacturer will have to demonstrate more than just a packaging step for imported products to the government).

The cultivator can start growing crops from either imported seeds/strains or he/she can source the seeds/strains locally.

The Importer/Exporter are wholesalers.

Lastly, the laboratories play a part across the supply chain in order to maintain quality standards.

Demand & Supply Pathways

Demand — In Australia, medicinal cannabis products are available to patients only through prescription. It is estimated that there are currently 1400 registered patients in Australia, as quoted by industry professionals at the recent Cannatech conference, that can use medicinal cannabis legally. Medicines that are available on prescription fall in two categories -

- Approved medicines — Medicines that have been clinically tested and the federal government have taken steps to vet the quality and efficacy of such medicines. Currently, only one Cannabis-based medicine (Sativex) is in the approved category

- Un-Approved medicines — Medicines for which there is not yet enough information for the federal government to make a decision on the risks, quality, the efficacy of those medicines. Most medicinal cannabis products fall in this category

Approved medicines — Are easier to access just like any other prescription medications (e.g. antibiotics) as they are well regulated, can be advertised for specific purposes, and medical practitioners are confident about the effects of those medicines. These medicines are supplied to health practitioners through existing pharmaceuticals distribution channels. Sativex, used for treating Multiple Sclerosis (MS), is the only approved cannabis-based medicine. However, MS is the least prevalent condition for which medicinal cannabis is used as a treatment in Australia, 0.1% of the total population compared to chronic pain at 16.2%. Approved products such as Sativex make up a small percentage of the total demand.

Unapproved medicines — Most of the medicinal cannabis products fall in this category and access to these medicines is tightly controlled by the government, advertising has strict rules, and there is a long lead-time for the patient to receive product due to the paperwork involved.

There are two schemes through which the demand for unapproved medicinal cannabis products is fulfilled -

- Authorized Prescriber (AP) — A medical practitioner can become an AP of cannabis medicine if they meet the requirements (should be trained, able to determine needs of the patient, and monitor outcome) as laid out by the TGA. There is paperwork involved and it could easily take several weeks to get approved (applicant has to meet both state and federal requirements, receive an ethics committee approval or get endorsed by specialist colleges). Once a medical practitioner becomes an AP they do not need to notify the government to prescribe medicinal cannabis products. A patient can visit an AP and get approval right away. Currently, there are only 49 AP’s in Australia and there is no publicly available information on how many patient applications have been processed by AP’s 7. Demand generated through this access is not public information but it is safe to say that the demand generated through AP’s is significantly less compared to the Special Access Scheme (SAS) discussed below. One can arrive at this conclusion because of the number of SAS applications approved so far, a total of 1771 applications as mentioned on the TGA website, is somewhere close to the total ~1400 patients in Australia 8. The ratio of patients to applications is not 1:1 because some patients have submitted more than one application. My interactions with the TGA have led me to believe that there are a few 100 patients that have submitted more than one application. There is an opportunity to streamline the AP process that might boost demand.

- Special Access Scheme (SAS) — As discussed above, it can be inferred that the majority of demand in Australia is currently generated through the SAS (SAS A or SAS B). The way this scheme works is that a medical practitioner, after assessing a patient, has to submit an application to the government specifying details such as clinical justification of prescribing a specific medicinal product, sufficient safety, and efficacy data. All of which requires in-depth product knowledge and education. It takes about two days for the TGA to process applications as each application is evaluated on a case-by-case basis. A couple of companies in Australia, Cannabis Access Clinics & Emerald Clinics, have started clinics to provide consultancy to both patients and medical practitioners about medicinal cannabis treatments that comply with government regulations, particularly through the SAS. The growth of such clinics is likely to have an uptake in demand. Additionally, some states such as NSW have also developed a hotline for doctors to help answer any questions they may have related to medicinal cannabis.

Supply — Almost all of the medicinal cannabis legally supplied in Australia is currently imported. In 2017, Australia imported ~145 Kgs of medicinal Cannabis product from Canada. It is expected that as domestic manufacturing picks up imports will decline and Australia would become a net exporter of cannabis products. The rate at which domestic companies are granted permits, their operations ramp up and they standardize manufacturing processes, will determine the export volume from Australia. At present, there are only three domestic companies that have started growing operations in Australia with more companies (pending permits) to follow suit in the coming months.

For the domestic market, medicinal cannabis can be either supplied via -

- Local cultivation & manufacturing — To understand the supply pathways involved let’s begin at the first step of cultivation followed by manufacturing

A) Cultivation — Anyone who wishes to cultivate or grow Cannabis plant, for medicinal purposes, will first require licenses from both the state and federal government and then a permit from the ODC that details the types & quantities of Cannabis that will be produced by the cultivator. The cultivator can source seeds locally from a regulated cultivation industry or have them imported (license required). It is important to note that a cultivator is required to have a contract or a written agreement from a manufacturing buyer, as a prerequisite, to submit an application for a license. This regulation is restrictive because it limits supply channels. The cultivator cannot start growing unless he/she has a contract with a manufacturer. Additionally, the quantity of cannabis one can cultivate is also regulated through the contract with the manufacturer which in turn depends upon the requirements of medical practitioners and patients. A cultivator can also only supply medicinal cannabis to a manufacturer with whom there is a contract. However, a cultivator can also be the manufacturer of the finished product, in which case, a separate manufacturing license is also required by the cultivator. This type of regulation tends to favor vertically integrated companies in which the cultivator and manufacturer are the same company, saves the hassle of getting into a contract beforehand.

B) Manufacturing — A manufacturer of medicinal cannabis finished products can either source raw cannabis plant from a domestic cultivator, import from countries where cannabis is federally regulated (import license required) or grow its own (requires cultivation license as well). Most Australian companies fall in the last category. The manufacturer, like the cultivator, requires both state and federal licenses as well as a permit from the ODC to begin operations. A two-step process, first procuring licenses then permit. Each manufacturer must ensure that their products comply with all applicable quality standards (TGO 93, TGO 98 of the Therapeutics Good Order) and manufacturing standards Code of Good Manufacturing Practice (GMP). Record keeping, Security Arrangements, Standard Operating Procedures (SOP’s), lab tests etc. are all part of the process to maintain compliance and receive a license. Unlike a cultivator, the manufacturer does not require any contract to apply for a license. However, a permit is granted only when a manufacturer has the demand to supply to a medical practitioner or patient through one of the access pathways. The amount of product that can be manufactured is also dictated by this demand. The manufacturer may also export the finished product if they meet certain conditions mentioned in the exports section below. Currently, manufacturers cannot advertise medicinal cannabis products to the public.

2. Imports — Importers of medicinal cannabis either import seeds for cultivators, flower/leaves or semi-finished cannabis products for manufacturers, or act as wholesalers of finished cannabis products. Medicinal cannabis product can be received from a GMP cleared overseas manufacturer in bulk and put in storage. However, it can only be distributed within Australia when there is a demand from a medical practitioner or patient through one of the access pathways. An importer also needs both federal license (to move product across international borders) and state license (for distribution within each state) as well as a permit each time there is a shipment. Advertising follows the same rules as in manufacturing and there are currently 15 licensed importers listed on the ODC website.

For the international market, the Australian government permits exports of medicinal cannabis product as outlined below,

Exports — Other than cannabis flower, leaves etc. or cannabis resin all forms of medicinal cannabis products can be exported from Australia. To be able to export medicinal cannabis products, an exporter requires to list the product on the ARTG as ‘export-only’ and then apply for an export license & permit (for each shipment) from the ODC. The exporter will need to demonstrate that they are able to supply medicinal cannabis in Australia for supply under the special access scheme, to authorized prescribers or for clinical trials (this is to ensure domestic demand if fulfilled first before exporting). In addition, the exporter has to prove that medicinal cannabis products for exports were manufactured under a GMP license. With medicinal cannabis demand growing slowly in Australia, most domestic manufacturers hope to export a majority of their products in the short to medium term to European & South American countries.

Laboratories — Play a key role in maintaining the quality of products in the medicinal cannabis supply chain. Laboratories are required to perform standardized tests as per TGA to provide information on pesticides, impurities, cannabinoids, terpenes, etc. inside a medicinal cannabis product. These tests are needed so that cannabis products, at every step in the supply chain, comply with TGO 93 quality standards. The government requires plants used in the manufacture of cannabis products, finished medicinal cannabis products, & any medicinal cannabis product that is imported or exported to conform to TGO 93 quality standards. This implies that a manufacturer, & importer/exporter both require a laboratory to test their cannabis products. However, a cultivator/producer is not required to get the plants tested. Currently, there is only one independent lab in Australia, Auscannlabs, that conducts cannabis testing.

Forecasts

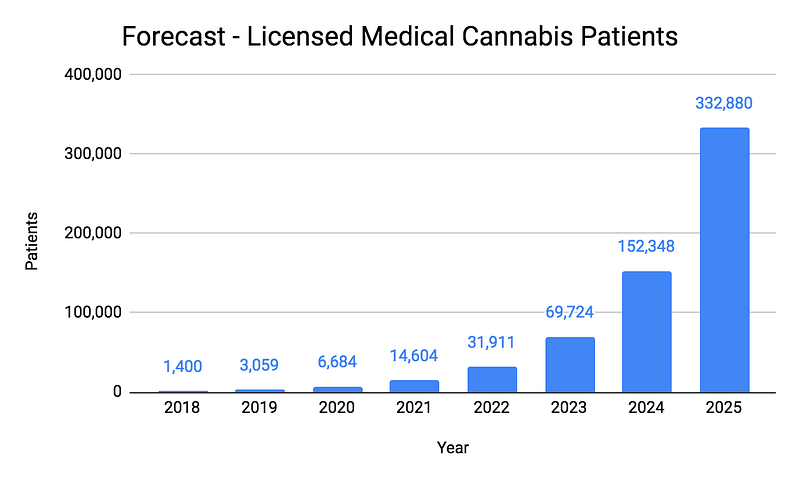

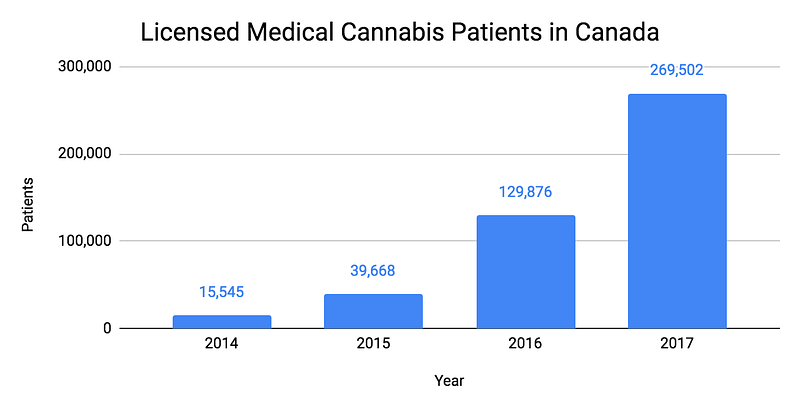

Patients — This is based on prevalence rates of the qualifying conditions accepted in Australia for medical cannabis treatment — Epilepsy, Multiple Sclerosis, Nausea & Vomiting, Chronic Pain & Palliative Care and the levels of patient participation seen in other medical cannabis markets for these conditions. New Frontier Data has estimated that there will be 330,000 legal medicinal cannabis patients in Australia by 2025. This patient estimate does not account for Australian health department expanding the use of medicinal cannabis as a treatment to other medical conditions or the impact of a recreational cannabis market if it were legalized. However, at this point in time, with limited data available this estimate is used as a starting point. For the patient population to increase from 1400 in 2018 to 330,000 by 2025, means an annualized growth rate of ~120% year on year (chart 1). This number may seem high but considering that the number of licensed Medical Cannabis Patients in Canada grew by ~160% year-on-year from 2014–2017 (chart 2), it seems to be a reasonable estimate.

Chart-1

Chart — 2

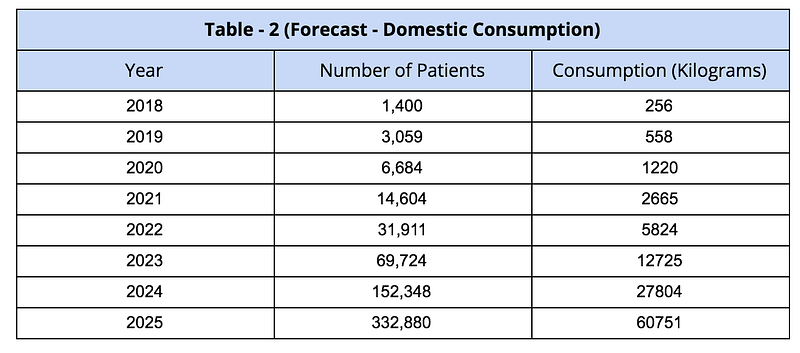

Domestic consumption — Assuming that on average each patient consumes 0.5 grams of medicinal cannabis daily, then the amount of cannabis forecasted to meet domestic demand is as follows (table 2) -

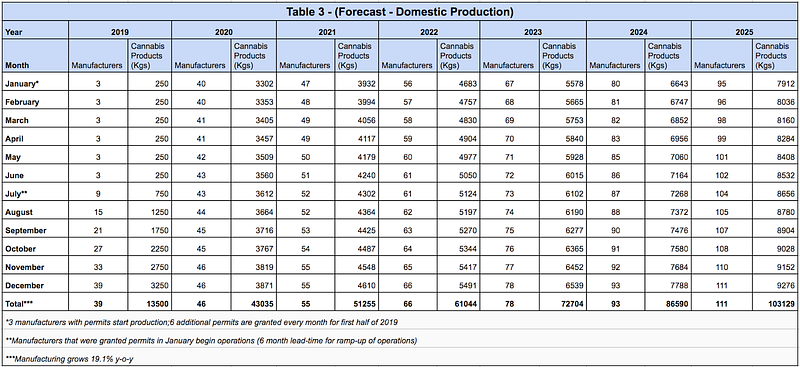

Domestic Production — Based on publicly available information on the production capacities of cannabis manufacturers globally, 10 square feet of grow area yields on an average about 1 kg cannabis plant annually.

Australian manufacturers such as the Cann Group, Creso Pharma, & Althea Group either have built or plan to build the largest production facilities in Australia ranging from 15,000–40,000 sq. ft. with an estimated production capacity of 1,500–4,000 Kgs of cannabis product annually. However, these manufacturers have the largest market-cap in Australia. Most cannabis manufacturers, somewhere in the range of 40 (28 of which are listed on the ASX), have a much lower market cap. Therefore, the annual average production capacity of these manufacturers is also estimated to be lower, bringing down the overall average of production capacity for all cannabis manufacturers in Australia.

For the purposes of forecasting domestic production volumes (Table 3 — next page), the following assumptions have been considered.

- A domestic manufacturer produces an average of 1000 Kgs of cannabis product annually (as discussed above)

- 6 manufacturing permits are granted every month for the first half of 2019 (currently there is a 6-month backlog in processing time and about 36 manufacturers are awaiting permits)

- It takes 6 months for a manufacturer to ramp-up operations once a permit has been granted

- Manufacturing grows by 19.1% each year (Medical Cannabis industry growth pegged at 19.1% CAGR)

It is important to note that in addition to legal domestic production there are a number of black-market growing operations in Australia that are currently involved in illicit trade — Based on UNDOC data ~21,000 Kgs of illegal cannabis products were seized in Australia in 2016. If the Australian government, like the New Zealand government, were to offer amnesty to these growers then it would provide an opportunity for illicit cannabis growers to enter the legal medical cannabis industry. Such a change in regulation would also have an impact on the overall supply, price, & distribution of cannabis. New Zealand manufacturers such as Helius Therapeutics & Hikurangi Cannabis Company have already invited local growers to start collaborating. The impact of a black market supply has not been considered in the forecast below (table 3).

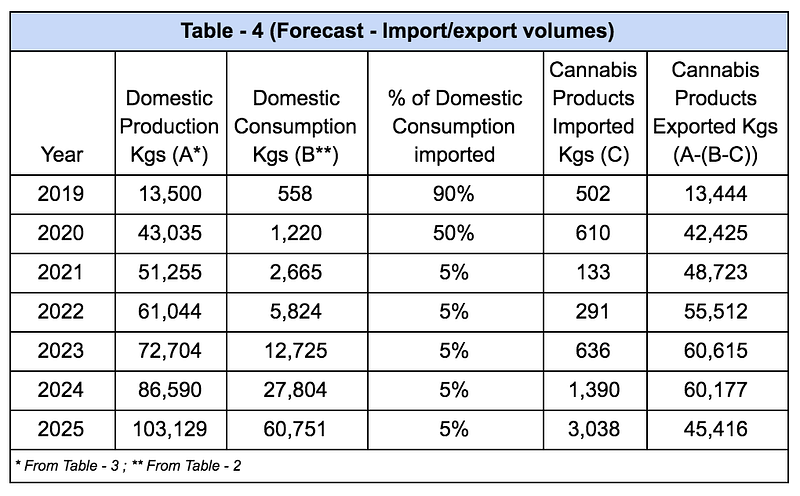

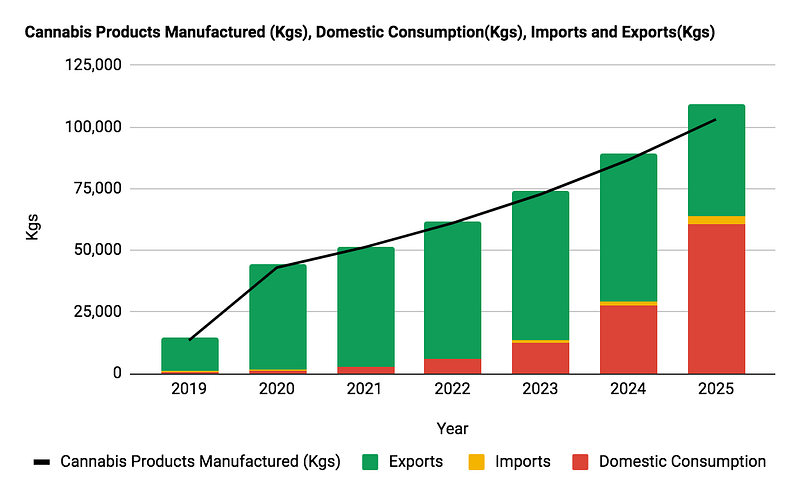

Imports/Exports — As discussed previously (Table-2 & Table-3), it can be observed that forecast of domestic production (supply) is expected to far exceed the forecast of domestic consumption (demand) of medicinal cannabis products. Not only would domestic products be cheaper to purchase than imported products, but excess supply would further drive prices down for medicinal cannabis products. Thus making imports less appealing to domestic patients. Assuming that imports drop from 90% in 2019 to 50% in 2020 and finally stabilize at 5% of domestic demand from 2021 onward. Import/Export volumes are forecasted as follows (Table — 4).

The above assumptions depend upon two key factors 1) Number of manufacturing permits granted by the government & 2) The speed at which Australian manufacturers will be able to manufacture quality medicinal cannabis products. The percentages (in table — 4) may vary quite a bit but directionally the trend of imports vs exports should be as shown below (Chart 3)

Chart — 3

Assuming imports make up 90% of domestic demand in 2019, 50% of domestic demand in 2020, & less than 5% of domestic demand thereafter