Savings, Retirement

Make Sure You Don’t Completely Run out of Money. Use Your Retirement Savings Wisely.

All ages: Don’t retire broke. Be ready for another pandemic, cataracts or any other emergency.

The coronavirus has forced people to hunker down and conserve. Before going back to thoughtless spending, take a long-term view and think about your future. With a little planning, money would be the least of your worries if such an event happens again.

Retirement can present the same type of money problems, except in slow motion.

Retired people worry about running out of money. My dad ran out of money. We had to help support him just so he would have food on the table.

The second part of this article shows how to avoid that. But first, you must have money, no matter how much, to have some control over your life.

Young people: Can you save $5 or $10 per week? With that, you will have some money when you retire. Also, prepare now, at least financially, for a second pandemic or other disasters.

If you don’t, you will be broke your entire life. You don’t want to retire living solely on social security.

Building the Retirement Fund

Teenagers and 20-somethings are usually broke, and retirement is 45 years away, anyway. There’s plenty of time. Then you’re 40, with no retirement savings, and wondering where the time went.

You can start an IRA (Individual Retirement Account) at any time, even if you are working part-time at McDonald’s while in college. Your goal is to get in the habit of putting money into that IRA every paycheck.

Can you save five dollars per week?

You say, “I don’t make enough!” Really? Can you deposit five dollars per week or 25 dollars per month? If you start at age 25 with an initial deposit of 25 dollars to open the account, then add just 5 dollars to your monthly deposit each year, you would have $111,362 at age 65, assuming 2% interest. Waiting 2 years to retire, if you are physically able to, increases the amount to $127,826.

If you use cash only, save all of your change.

Financial planners tell you 8% growth, but that is fantasy land for most people. If you started at $50 initial deposit and 10 dollars per week, or $50 per month, you’d have $151,403 in your retirement fund.

When you get enough money in your IRA, you can transfer part of it from the savings account to higher-paying CDs.

You never, ever, withdraw money from that IRA.

First, you would have to pay income taxes on the withdrawal and then there might be penalties. Finally, that IRA is protected even if you declare bankruptcy. The worst thing you can do is retire broke. That IRA gives you some options.

While you do that:

Set up an emergency fund

You avoid a lot of problems if you start a second, regular savings account and deposit the same amount. That is your emergency fund.

If you break your arm playing basketball in the park or must replace a tire tomorrow, it’s better to pay cash than borrow the money. If you are a student, that could help with the deposit on your first apartment.

I was dumb and almost 50 when I set up my first emergency fund. It cost me a lot over the years.

If you wait until you are over 50 to start your retirement fund, you will need to save almost $600 per month to reach $151,403.

Spending the Retirement Fund

Now that you’re retired, how do you make your withdrawals? You may have done well and have ten million dollars in the bank. Even with that amount, unrestrained spending on a multimillion-dollar house, high-priced junk, and vacations can drain the account fast.

My plan tells me how much I can spend each year for 40 years. Most likely, I will not run out of money.

I will use the $151,403, not the ten million, in the examples. I use a spreadsheet to track everything, but you can use a notebook or have separate bank accounts. Whatever works for you.

Split the money on paper into escrow accounts (devoted funds) and spending categories. Think of the escrow accounts as emergency funds.

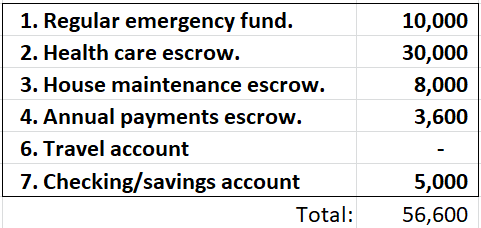

- Regular emergency fund 2. Health care escrow 3. House maintenance escrow 4. Annual payments escrow 5. Monthly budget 6. Travel account 7. Checking or savings account

You can spend your travel account on anything, not necessarily travel. Just because you have more than that in the bank, it doesn’t mean that you should spend it.

Monthly budget first You don’t feel like doing a budget? Fine, go to the next section on escrows, but be prepared for surprises on January 1st. Hopefully, not too big.

How much do you usually spend each month? Do not include vacations or major purchases. Include 1/12th of annual insurance premiums and property taxes.

Do you need a part-time job?

Do you have enough regular income, like Social Security and other monthly retirement sources, to cover that amount? If not, you may need to get a regular part-time job.

But I have all of this money in the bank!!!!!

We will see. You don’t want to be forced to work or starve at age 90.

The average gross Social Security income is about $1,500 per person, before deductions for Medicare and income taxes, or about $1,300 net per person. It could be less. We will use $2,600 for a married couple in the example.

Escrows Allocate funds from the IRA to your escrow accounts. Keep track of the balances if you must spend any money from them. You may want to physically move money to a separate IRA savings account just for the escrows.

You must withdraw money from the IRA if you spend them. The amounts are paper-only.

If the totals get too low, allocate funds from whatever remains in your IRA. It will, of course, cut the amount for your travel account the next year.

You thought there was $151,403 to spend…

Nope. You have less than $95,000 after you subtract the $56,600. That has to last you the rest of your life. Notice the travel account (#6) is empty.

The health care escrow may seem large.

You have a 65% likelihood of developing cataracts. Surgery and single-distance lenses are covered by Medicare. They are good for one distance; other distances still need glasses. Progressive lenses and laser surgery for astigmatism costs an additional $10,000, which you must pay if you want it.

The health care escrow gives you a choice.

Open a bank account for daily use

Finally, open a bank account to use to pay bills, where your Social Security direct deposits will go, and where you can get cash. It should be at least equal to your monthly spending to start.

Fund the travel account yearly on Jan 1st First, we use the term “travel account” just to give it a name. Some might say, Slush Fund, Spending, or whatever you like. We bought our last computer using money from that account.

Unlike the other accounts, you move funds to the travel account on January first from whatever remains in your savings accounts minus the escrows total above. That’s your available funds. Include the balance in the travel account from the end of last year or zero if negative (you spent all of it and more).

How much? Whatever will prevent you from running out of money, based on your age on January 1st.

First, decide how long you want the money to last — what age. If your relatives lived to 100, you better use at least 105. Subtract your age from that number and divide your available funds with the answer. If you are married, use the younger person’s age.

We’ll use 95 and a current age of 67 in the example.

Travel amount = 94,803 / (95 - 67)

The calculated travel amount is $3,385.82 or rounded to $3,400 in the first year, less than $300 per month. Rounding doesn’t change anything since the travel amount adjusts itself the next year when the balances change.

Add the $3,400 to the travel account total remaining from the prior year.

Just don’t do something silly, like assuming you will die at age 72. People are living longer. Use a realistic final age.

Monthly spending adjustment to the travel account If you didn’t do a budget or your monthly income is close to your spending, skip to the next section.

Subtract the monthly spending from your monthly income. Multiply by 12.

- If your income was higher than your spending, add the result to the travel account

- If your income was less than your spending, subtract the result from the travel account

The final total is what you have to spend for the year.

If there is nothing left or you are in the hole, you need to cut your monthly spending or may need to get a part-time job.

If you took the vacation of a lifetime and spent three years from your travel account, don’t worry about it. The account will adjust itself on January 1st.

Just don’t do it more than once or twice.

Update travel amount monthly on the 1st Suppose you didn’t travel. Don’t do anything.

If you did travel, add all expenses including hotel, gas, parking, restaurants, and tours. Any cost during the trip.

- If the trip cost was less than the travel account balance, subtract it to get the new balance. You still have that much to spend for the remainder of the year.

- If the trip cost was more than the travel account balance, the new balance is zero.

You can spend the travel account on anything. Suppose you want a new TV. Sure, as long as there is enough money in the travel account to cover it.

The travel account stops you from spending your savings too fast

If you do a budget and track expenses for the month, subtract any significant overspending from the travel account, too. Of course, you can add to the travel account if you spent significantly less.

Other considerations You may have additional assets that you want to add to available funds.

- Stocks. If they are a small part of your total, add their value on January 1st. If large, like 50% or more, divide their value in half and use that.

- Your house. No. You need someplace to live and you can’t turn it into cash.

- Your vacation home. Very risky unless you have a large amount of cash assets. You can’t quickly turn it into cash to cover your escrow accounts.

Of course, if you have these, you probably have a financial advisor.

Conclusion

Having enough money throughout retirement is easy — if you have saved some money and your monthly income covers your usual monthly spending. Even if it doesn’t, this method still helps stretch what’s available.

To summarize:

- Save some money

- Take out and set aside an emergency fund, health-care emergency fund, house major maintenance fund, and annual payments fund

- Divide what’s left by the number of remaining years you hope to be alive

- Spend that amount if you want

- Add it to the next year if you don’t spend any of it.

Finally, the travel account is meant to be spent. Do something you always wanted to do, even if it costs two or three years from the account. It will adjust itself the next year.

No matter what happens, you will still have your emergency funds.

The whole idea is to have peace-of-mind and not to run out of money too soon.

This article is for informational purposes only, it should not be considered Financial or Legal Advice. Not all information will be accurate. Consult a financial professional before making any major financial decisions