Let’s stop being gullible. You can’t predict stocks with a simple LSTM.

Dear Medium reader, Like many of us, I began my journey into algorithmic trading with stars in my eyes. It was through articles and catchy headlines that I was able to believe for a moment that predicting the stock market was child’s play. Who wouldn’t be tempted to try it when you read this kind of headline on serious forums: “Predict the stock market with AI and LSTM”.

Today, in my new article, we’re going to demonstrate in practical terms (and with a sense of humour!) that this is obviously not viable!

0. Imports

To carry out our study, we will use the following libraries:

import math

import json

import numpy as np

import pandas as pd

import requests

from sklearn.preprocessing import MinMaxScaler

import matplotlib.pyplot as plt

from sklearn.model_selection import train_test_split

import tensorflow as tf

from tensorflow import keras

from tensorflow.keras import layers

from keras.utils.vis_utils import plot_model1. Collecting data

For the purposes of this study, we’re going to look at some of the stock prices most commonly used by this type of author. Of course, we won’t be basing our analysis on a **share that’s made you laugh** or Gamestop, but on a stock that makes you dream, like AAPL, MSFT or many others. It’s certain that if you want to sell dreams, it’s easier to base yourself on stocks like these.

To retrieve this data, we’re going to use Alpaca Market, a company dedicated to algorithmic traders, whether professional or not, which enables us to implement real investment solutions.

def get_historical_prices(symbols, interval = '1Day', start_date = None):

def fetch(url, next_page_token = None):

if next_page_token:

url+=f'&page_token={next_page_token}'

headers = {

"accept": "application/json",

"APCA-API-KEY-ID": "YOUR-API-KEY",

"APCA-API-SECRET-KEY": "YOUR-API-SECRET-KEY"

}

response = requests.get(url, headers=headers, verify=False)

data = json.loads(response.text)

try:

next_page_token = 'stop' if str(data['next_page_token']) == 'None' else str(data['next_page_token'])

except:

next_page_token = 'stop'

return data['bars'], next_page_token

if start_date:

url = f"https://data.alpaca.markets/v2/stocks/bars?symbols={'%2C'.join(symbols)}&timeframe={interval}&start={start_date}&limit=10000&adjustment=raw&feed=iex"

else:

url = f"https://data.alpaca.markets/v2/stocks/bars?symbols={'%2C'.join(symbols)}&timeframe={interval}&limit=10000&adjustment=raw&feed=iex"

historical_prices = {}

next_page_token = None

while next_page_token != 'stop':

data, next_page_token = fetch(url, next_page_token)

print(next_page_token)

historical_prices.update(data)

print(historical_prices)

print('Data Downloaded')

prices = [[[dict['t'],dict['c']] for dict in historical_prices[symbol]] for symbol in symbols]

active_symbols = []

stocks = {}

for i in range(len(symbols)):

try:

stocks[symbols[i]] = pd.DataFrame(prices[i], columns=['date', 'close']).sort_values(by='date', ascending=True)

active_symbols.append(symbols[i])

except:

print('bug with: ', symbols[i])

return stocks, list(stocks.keys())

# Download data

symbols = ['MSFT']

stocks, symbols = get_historical_prices(symbols, interval='1Day', start_date='2020-09-01')

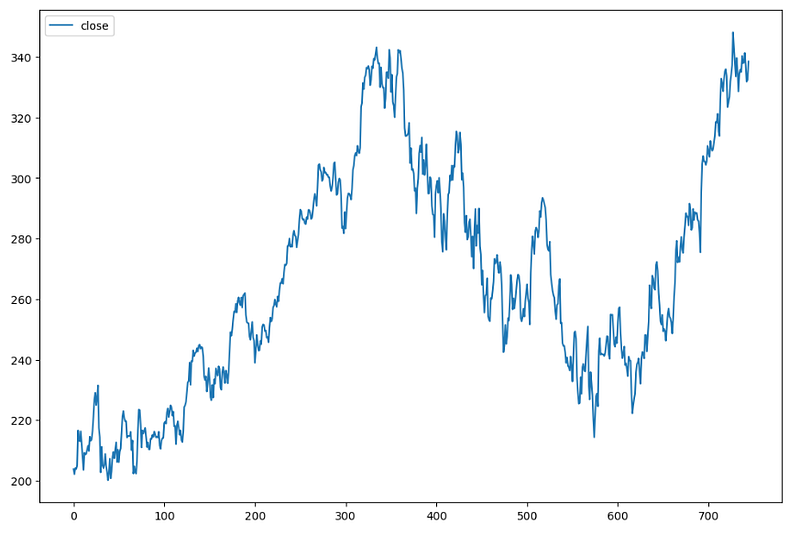

stocksLet’s plot the MSFT share price to show these newcomers what we’re all about.

2. Setting the LSTM

(This part is just to set the LSTM for a newcomer, if you are at ease with basics LSTM, go directly to section 3.)

No more daydreaming, it’s time to code! Let’s implement our LSTM in the best possible way, with a little pre-processing.

First of all, we’re going to scale the data

# Define the dataframe, here we’re looking at MSFT

df = stocks['MSFT'][['date', 'close']]

# Scaling the data

scaler = MinMaxScaler(feature_range=(0,1))

scaled_values = scaler.fit_transform(np.array(df.sort_values(by='date', ascending=True)['close']).reshape(-1,1))

scaled_df = df.copy()

scaled_df['close'] = scaled_values

scaled_dfThen split them into two parts. One for training and one for testing. (be careful to set shuffle=False, as our data must be in chronological order).

train_df, test_df = train_test_split(scaled_df, test_size=0.2, shuffle=False)

train_dfLet’s set up the rolling windows for the LSTM.

# Set up the train rolling window for the LSTM

x_train = []

y_train = []

for i in range(30, len(train_df)):

x_train.append(train_df.iloc[i-30:i]['close'])

y_train.append(train_df.iloc[i]['close'])

x_train, y_train = np.array(x_train), np.array(y_train)

x_train = np.reshape(x_train, (x_train.shape[0], x_train.shape[1], 1))# Set up the test rolling window for the LSTM

x_test = []

y_test = []

for i in range(30, len(test_df)):

x_test.append(test_df.iloc[i-30:i]['close'])

y_test.append(test_df.iloc[i]['close'])

x_test = np.array(x_test)

x_test = np.reshape(x_test, (x_test.shape[0], x_test.shape[1], 1))Now it’s time to build our LSTM architecture. To do this, we’ll adopt the most basic version possible.

model = keras.Sequential()

model.add(layers.LSTM(128, return_sequences=True, input_shape=(x_train.shape[1], 1)))

model.add(layers.LSTM(64, return_sequences=False))

model.add(layers.Dense(32))

model.add(layers.Dense(1))

model.summary()And finally, let’s train our AI.

model.compile(optimizer='adam', loss='mean_squared_error')

model.fit(x_train, y_train, batch_size= 1, epochs=3)3. A first prediction

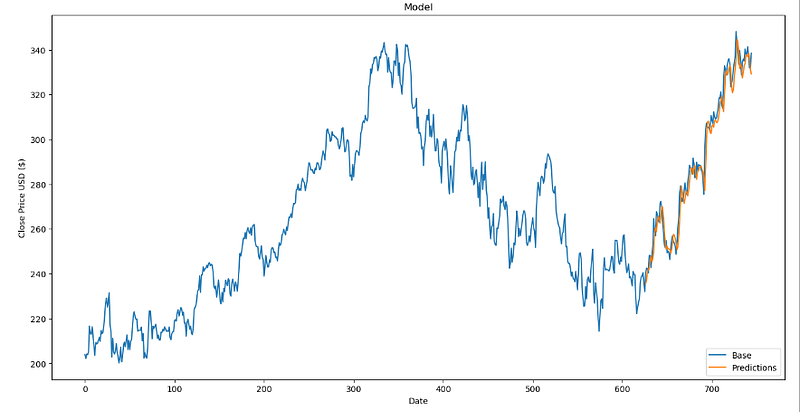

Using our LSTM, let’s predict the test values and look at the fabulous result we get.

predictions = model.predict(x_test)

predictions = scaler.inverse_transform(predictions)

validation = test_df[30:].copy()

validation['predictions'] = predictions

plt.figure(figsize=(16,8))

plt.title('Model')

plt.xlabel('Date')

plt.ylabel('Close Price USD ($)')

plt.plot(df['close'])

plt.plot(validation[['predictions']])

plt.legend(['Base', 'Predictions'], loc='lower right')

plt.show()

INCREDIBLE!!! Our prediction fits the curve perfectly.

This is where the beginner will be fooled. It’s all very well to stop your article here and get thousands of views, but there’s something I feel needs to be made clear…

For each prediction, the LSTM uses the last 30 values (in our situation). These last 30 values are true and not predicted… We don’t make predictions based on predictions. In other words, we only forecast 1 day in advance.

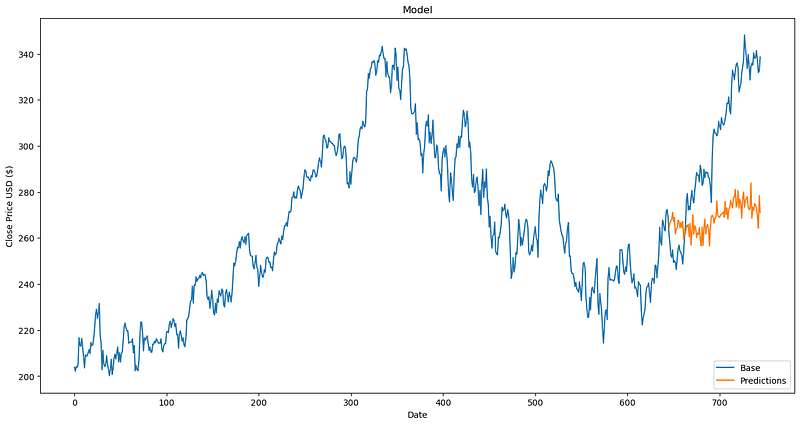

3. Back to reality

If we want to predict in the long term, we base our prediction on predictions etc. The errors then multiply at breakneck speed! Now let’s simulate this on python by removing the first value of X test and adding the last position of the predicted value, etc etc.

import numpy as np

import pandas as pd

from tqdm import trange

from sklearn.preprocessing import MinMaxScaler

from keras.models import Sequential

from keras.layers import LSTM, Dense

# Create a time series

df_train = df.iloc[:-100].copy()

time_series = np.array(df_train['close'])

# Normalization

scaler = MinMaxScaler(feature_range=(0, 1))

normalized_series = scaler.fit_transform(time_series.reshape(-1, 1))

# Training data

lookback = 30

X_train, y_train = [], []

for i in range(len(normalized_series) - lookback):

X_train.append(normalized_series[i:i+lookback, 0])

y_train.append(normalized_series[i+lookback, 0])

X_train, y_train = np.array(X_train), np.array(y_train)

X_train = np.reshape(X_train, (X_train.shape[0], X_train.shape[1], 1))

# Test data

last_instances = normalized_series[-lookback:]

X_test = np.array([last_instances])

X_test = np.reshape(X_test, (X_test.shape[0], X_test.shape[1], 1))

# Prediction

predicted_values = []

for i in trange(100):

model = Sequential()

model.add(LSTM(128, input_shape=(lookback, 1)))

model.add(Dense(32,activation='relu'))

model.add(Dense(1,activation='sigmoid'))

model.compile(loss='mean_squared_error', optimizer='adam')

model.fit(X_train, y_train, epochs=1, batch_size=1, verbose=0)

predicted_value = model.predict(X_test)

X_test = np.reshape(np.array([np.concatenate((X_test.reshape(lookback,)[1:], predicted_value[0])).reshape(-1, 1)]), (X_test.shape[0], X_test.shape[1], 1))

predicted_values.append(scaler.inverse_transform(predicted_value)[0][0])

print("Predicted values:", predicted_values)Now let’s take a look at the result with a long-term prediction and how quickly it deviates from reality.

4. Conclusion

To conclude, these headlines are very catchy and allow these authors to get a lot of views, but they are misleading and only show part of the truth. Nevertheless, it still allows people to think a little about these technologies and arouses their curiosity, we can’t take that away from them!

However, LSTMs should not be thrown away, because they are good indicators of the next value to be predicted! We’ll be talking about them in a future series of articles on long-short equity trading strategies! Thank you for your time and take care!

PS : A bonus part has been added at the end

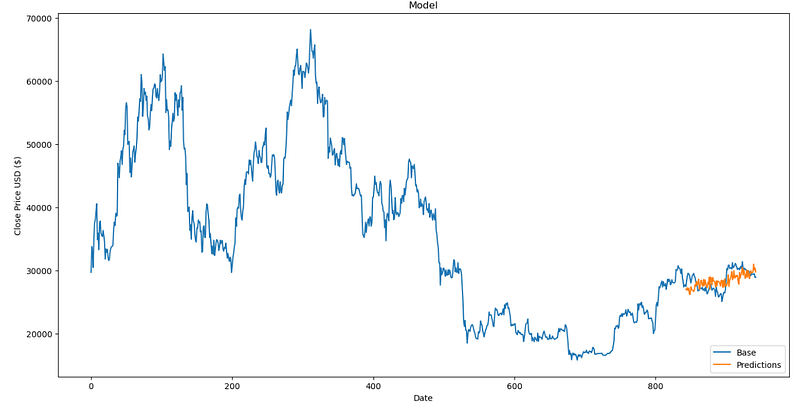

5. Bitcoin

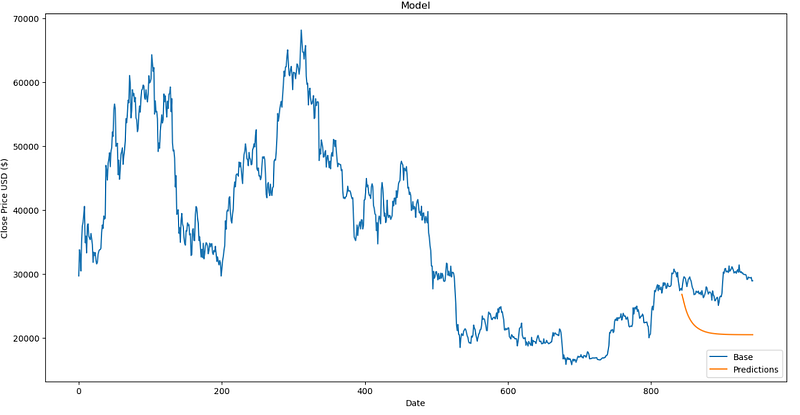

Previously in this article, we worked on shares of the stock market but after consideration, I think that would be worth it to also test it on the bitcoin. Please find below a slightly different function to get the historical data from Alpaca (no need Api Key for the bitcoin). And also different results ! (No others changes are needed)

def get_historical_prices(symbols, interval = '1Day', start_date = None):

def fetch(url, next_page_token = None):

if next_page_token:

url+=f'&page_token={next_page_token}'

response = requests.get(url, verify=False)

data = json.loads(response.text)

try:

next_page_token = 'stop' if str(data['next_page_token']) == 'None' else str(data['next_page_token'])

except:

next_page_token = 'stop'

return data['bars'], next_page_token

if start_date:

url = f"https://data.alpaca.markets/v1beta3/crypto/us/bars?symbols={'%2C'.join(symbols)}&timeframe={interval}&start={start_date}&limit=10000"

else:

url = f"https://data.alpaca.markets/v1beta3/crypto/us/bars?symbols={'%2C'.join(symbols)}&timeframe={interval}&limit=10000"

historical_prices = {}

next_page_token = None

while next_page_token != 'stop':

data, next_page_token = fetch(url, next_page_token)

print(next_page_token)

historical_prices.update(data)

print(historical_prices)

print('Data Downloaded')

prices = [[[dict['t'],dict['c']] for dict in historical_prices[symbol]] for symbol in symbols]

active_symbols = []

stocks = {}

for i in range(len(symbols)):

try:

stocks[symbols[i]] = pd.DataFrame(prices[i], columns=['date', 'close']).sort_values(by='date', ascending=True)

active_symbols.append(symbols[i])

except:

print('bug with: ', symbols[i])

return stocks, list(stocks.keys())

symbols = ['BTC/USD']

stocks, symbols = get_historical_prices(symbols, interval='1Day', start_date='2016-01-01')

df = stocks['BTC/USD'][['date', 'close']]

Ouch… As beautiful as it can be, I dare you to bet even 1k£ on such a prediction…

6. Alternative algorithm but faster

As you may have noticed, I have trained the LSTM in every loop which considerably reduced the speed of the LSTM but produced much more convincing results. Below is a much faster but less accurate code, as you will see.

import numpy as np

import pandas as pd

from sklearn.preprocessing import MinMaxScaler

from keras.models import Sequential

from keras.layers import LSTM, Dense

df_train = df.iloc[:-100].copy()

# Create a time series

time_series = np.array(df_train['close'])

# Normalization

scaler = MinMaxScaler(feature_range=(0, 1))

normalized_series = scaler.fit_transform(time_series.reshape(-1, 1))

# Training data

lookback = 30

X_train, y_train = [], []

for i in range(len(normalized_series) - lookback):

X_train.append(normalized_series[i:i+lookback, 0])

y_train.append(normalized_series[i+lookback, 0])

X_train, y_train = np.array(X_train), np.array(y_train)

X_train = np.reshape(X_train, (X_train.shape[0], X_train.shape[1], 1))

# LSTM

model = Sequential()

model.add(LSTM(128, input_shape=(lookback, 1)))

model.add(Dense(32,activation='relu'))

model.add(Dense(1,activation='sigmoid'))

model.compile(loss='mean_squared_error', optimizer='adam')

# Fit

model.fit(X_train, y_train, epochs=5, batch_size=1, verbose=1)

# Test data

last_instances = normalized_series[-lookback:]

X_test = np.array([last_instances])

X_test = np.reshape(X_test, (X_test.shape[0], X_test.shape[1], 1))

# Prediction

predicted_values = []

for i in range(100):

predicted_value = model.predict(X_test)

print(predicted_value)

X_test = np.reshape(np.array([np.concatenate((X_test.reshape(lookback,)[1:], predicted_value[0])).reshape(-1, 1)]), (X_test.shape[0], X_test.shape[1], 1))

predicted_values.append(scaler.inverse_transform(predicted_value)[0][0])

print("Predicted values:", predicted_values)

Ouch…

Github link : https://github.com/leopoldcosson/medium