KWSP 2023: Why stock investment is not for you

Prelude to KWSP (EPF) end of 2023

- Many individuals who are uninterested in stocks better be safe with their government securities or private insurance.

- See the web to compute your Cost of Living calculator for a moderate family and a single person in Malaysia. And KWSP’s guide and retirement calculator too before you decide to leave your Company.

- KWSP (EPF — Employment Provident Fund) can produce risk-averse investments at 5 to 7 percent annual dividend return.

- Investment requires some experience and the probability of losses is much higher that we cannot trifle with risks.

If we can’t comprehend the gyration of stocks, it is better to be safe with experienced hands such as a government vehicle or pension plan. Other private pension plans, such as insurance companies or asset management companies while employed by your Company can also provide retirement scheme plans in return for the life insurance plan governed by the SC (Securities Commission).

These investment vehicles can provide diversified investments without risking too much by picking a single stock or even several of these stocks.

I resided in Malaysia, KWSP (EPF – Employment Provident Fund, a sovereign wealth fund) which can produce risk-averse investment at 5 to 7 percent annual dividend return enough to overcome the basic cost of inflation.

Cost of living

TWO-thirds of Employees Provident Fund (EPF) contributors who are aged 55 and below – or 71% – do not have enough funds for retirement to raise them above the poverty level, revealed Prime Minister Datuk Seri Anwar Ibrahim.

According to Focus Malaysia.com, unfortunately, many do not have enough funds to retire comfortably.

The cost of living in Penang for a moderate family and a single person is in the range of 100k and 28k annually (see the web Cost of Living calculator with costs including a mid-range restaurant dining, beer, and cappuccino excluding rental nor accommodation costs). With a dividend return of 5% assuming a bad economic environment at a pessimistic assumption in the lower end of the range, the fund can produce 50k annually to compensate for a moderate lifestyle although an extravagant lifestyle. Enough to beat the current inflation rate of 1.5 percent in 2023 trending from the previous hike at 4% in 2022.

See also the KWSP contribution calculator for how to compute employer and employee annual contributions for a year. For the retirees, see the link provided by KWSP, whether we can retire comfortably.

KWSP provides exposure to Companies that power the economy engine in Malaysia. KWSP equities (short-listed 30 equities in 2022) reported to the public are of diversified kinds such as banking, investment holding, residential and commercial property development, real estate trusts, container transportation hubs, semiconductor production, telecommunication, maintenance of airports, oil, gas, petrochemical, logistics, healthcare, plantations, etc. There are too many categories to list on a flat list in one swoop. These are the top companies that power the economies in Malaysia of various kinds.

Diversification helps to reduce unsystematic risk that spans financial instruments, industries, and other categories. Systematic or market risk is generally unavoidable such as country debt and commodity risk.

How does KWSP work?

Under our government body, the KWSP scheme collects monthly salary for ~11% from our employees, with employers contributing an additional 12% to 13% based on the current statutory rate. Funds collected are then reinvested in bonds and equities to grow dividend income for future retirees.

KWSP reported income in 1H 2023: investment managers took advantage and capitalized on the market rally, which contributed to the higher return from equities during the period. In contrast to the last half of 2022, most markets posted worse performance and lower returns in decades during the OPR interest rake hike in 2022.

Despite the market returns, equity and bond markets will continue to remain fairly volatile given the varying expectations of the timing of the end of the hiking cycles by central banks, recession risks, policy uncertainty, and geopolitical tensions said KWSP Corporate Affairs Department. The last OPR interest rate decision hike was 0.25% for 3% in May 2023.

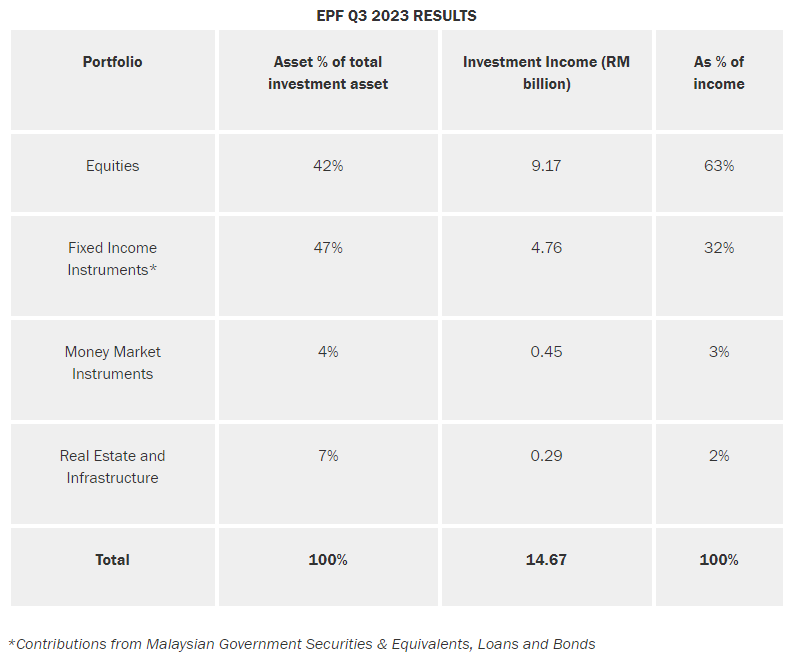

Based on KWSP’s posted Q3 2023, equities contributed 63% of investment income for 9.17b from its 42% total invested assets. Equity investments remained a significant contributor to KWSP.

In contrast to equities, fixed-income instruments contributed 32% of investment income from 47% of invested assets which are less volatile than equities. The remaining income contribution of 5% was from Money market instruments and real estate infrastructure investment. Lesser real estate income contribution was seen in Q3 with 2% compared to 15% contributed in 1H of 2023 when BNM hiked interest rate in May. Real estate investment is less volatile than equities. Bond price movement changes depending on the value of the income provided by its coupon payments relative to broader interest rate changes. Bonds are less susceptible to market fluctuation but can rattle the market during COVID-19 market distress.

See the table chart:

KWSP forecast in 2024 will be a tad slower than in 2023, expecting a slowdown despite the resilience it has shown in 2023 raised confidence in a soft-landing scenario.

In response to the International Monetary Fund’s (IMF) 2024 outlook1 that global economic growth in 2024 will be slightly lower than 2023, Datuk Seri Amir Hamzah said the EPF acknowledges the prevailing economic conditions that are anticipated to shape the fund’s business landscape.

KWSP engine

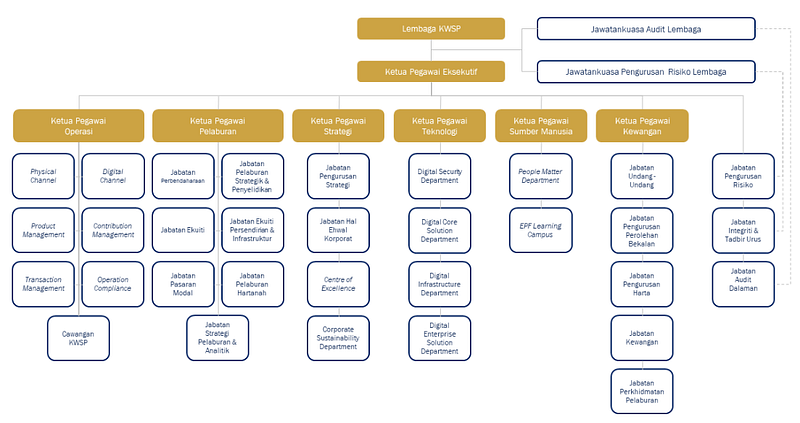

KWSP has about 14 million members and employed 5,700 staff approaching a trillion ringgit under its management. The expenses for running a pension fund (such as KWSP) can be aggregated into digital and physical counter operation, strategic investment, technology expenses, human resources, and legal and regulatory compliance costs (KWSP organization chart).

Why we can’t beat them

Investment requires some experience and the probability of losses is much higher that we cannot trifle with risks. Furthermore, it takes time to invest or trade to learn about the stock market. Therefore, it is better to stay away from it.

It requires understanding the management of the Company, financial knowledge, the ability to read charts, balance sheets, economics, and the list goes on. Almost everything going around in the world (from wars to elections to recessions) affects stocks therefore increasing the riskiness of markets. The stocks are not fixed rather it is dynamic, ticking up and down as with proton and electron whirling around orbits as the second goes, unlike fixed deposits at your banks. I can’t say for sure too, it comes with risks and a lot more volatility than the business behind that stock.

Long-term investments are more approachable rather than gambling with your hard-earned money. The ability to sit and do nothing is of rarity. Some argue immediate gratification to be reaped from the ticking of stocks is much more entertaining.

“If you took our top fifteen decisions out, we’d have a pretty average record. It wasn’t hyperactivity, but a hell of a lot of patience. You stuck to your principles and when opportunities came along, you pounced on them with vigor.”

– Charlie Munger

You may also want to consider index funds to diversify a broad range of assets rather than putting all eggs in a basket of Stocks.

Therefore, it is best to avoid it if we cannot understand the riskiness of the assets.

Furthermore, health is much more invaluable than stock tickering up and down.