Kalman Filters for Stock Price Signal Generation

Let’s implement a Kalman filter for predicting stock prices using synthetic data.

Overview:

- Generate synthetic stock price data.

- Implement a Kalman filter for the synthetic stock data.

- Demonstrate how the Kalman filter can be used to dynamically adjust predictions and trading strategies.

Step 1: Generate Synthetic Stock Price Data

To begin, we’ll generate synthetic stock price data. We’ll use a simple random walk model with some noise:

Where Pt is the stock price at time t, and ϵt is a random noise term.

import numpy as np

import matplotlib.pyplot as plt

# Seed for reproducibility

np.random.seed(42)

# Number of days for our synthetic stock data

num_days = 250

# Generate synthetic stock price data using random walk

epsilon = np.random.normal(0, 2, num_days) # Noise term

prices = np.cumsum(epsilon) + 50 # Start from a stock price of 50

# Plot the synthetic stock price data

plt.figure(figsize=(10, 6))

plt.plot(prices, label="Synthetic Stock Price")

plt.title("Synthetic Stock Price Data")

plt.xlabel("Days")

plt.ylabel("Stock Price")

plt.legend()

plt.grid(True)

plt.show()

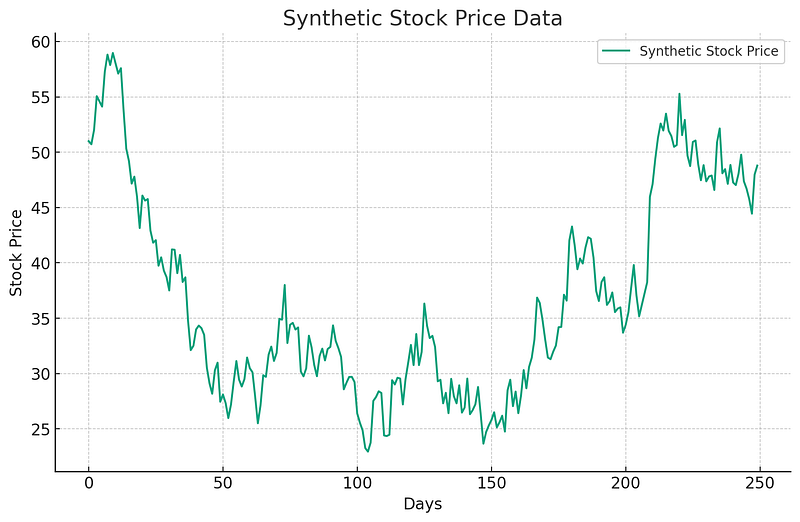

Here’s our synthetic stock price data based on the random walk model. The stock price starts at 50 and evolves over 250 days.

Step 2: Implement a Kalman Filter for the Synthetic Stock Data

The Kalman filter is a recursive algorithm used to estimate the state of a linear dynamic system from noisy observations. For our stock price prediction, we’ll use the following simple model:

State equation:

Where Pt is the true stock price at time t, and wt is the process noise which is assumed to be normally distributed with mean 0 and variance Q.

Observation equation:

Let’s implement the Kalman filter for our synthetic stock price data:

class KalmanFilter:

def __init__(self, Q, R):

# Initial state estimate

self.P_hat = np.zeros(num_days)

# Initial state estimate error variance

self.P_var = np.zeros(num_days)

# Process noise variance

self.Q = Q

# Measurement noise variance

self.R = R

# Initial estimate of state

self.P_hat[0] = prices[0]

# Initial estimate of state variance

self.P_var[0] = 1.0

def update(self, z):

for t in range(1, num_days):

# Prediction Step

P_hat_minus = self.P_hat[t-1] # Predicted state estimate

P_var_minus = self.P_var[t-1] + self.Q # Predicted error variance

# Update Step

Kt = P_var_minus / (P_var_minus + self.R) # Kalman gain

self.P_hat[t] = P_hat_minus + Kt * (z[t] - P_hat_minus) # Updated state estimate

self.P_var[t] = (1 - Kt) * P_var_minus # Updated estimate of state variance

# Parameters for our Kalman filter

Q = 1 # Process noise variance (assumption)

R = 4 # Measurement noise variance (based on our synthetic data generation)

# Create and run the Kalman filter

kf = KalmanFilter(Q, R)

kf.update(prices)

# Plot the results

plt.figure(figsize=(10, 6))

plt.plot(prices, label="Synthetic Stock Price", alpha=0.5)

plt.plot(kf.P_hat, label="Kalman Filter Estimate", linestyle="--", color="red")

plt.title("Kalman Filter Estimation of Stock Price")

plt.xlabel("Days")

plt.ylabel("Stock Price")

plt.legend()

plt.grid(True)

plt.show()

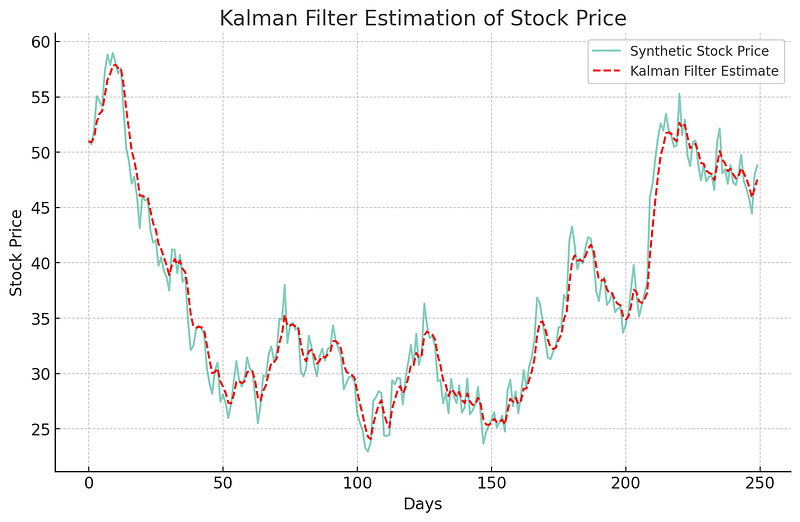

The plot above shows both the synthetic stock price data (in blue) and the Kalman filter estimate (in dashed red). The Kalman filter provides a smoothed estimate of the stock price, reducing the effects of noise.

Step 3: Demonstrate how the Kalman filter can be used to dynamically adjust predictions and trading strategies.

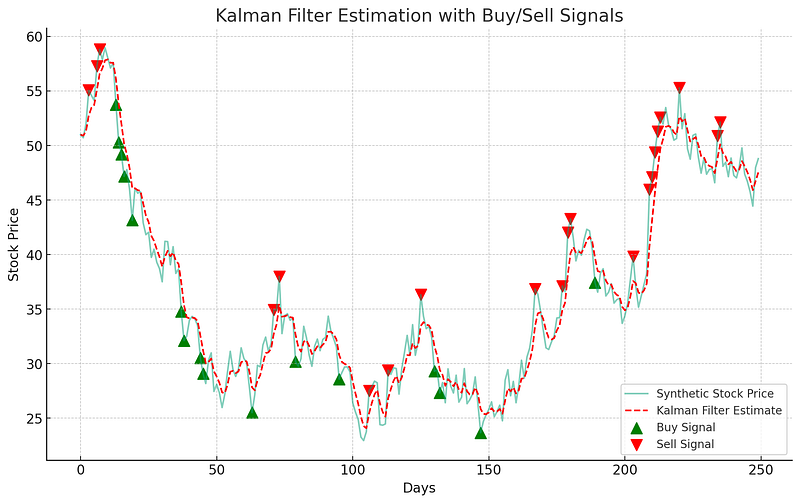

To demonstrate a basic trading strategy, let’s assume the following:

- We buy the stock when the Kalman filter estimate is significantly below the observed price, expecting a price correction upwards.

- We sell the stock when the Kalman filter estimate is significantly above the observed price, expecting a price correction downwards.

For simplicity, we can consider a threshold (e.g., 2 units) to determine when to buy or sell.

Let’s visualize these buy and sell signals on our plot.

# Threshold for buy/sell signals

threshold = 2

# Generate buy/sell signals

buy_signals = np.where(prices < kf.P_hat - threshold)[0]

sell_signals = np.where(prices > kf.P_hat + threshold)[0]

# Plot the results with buy/sell signals

plt.figure(figsize=(12, 7))

plt.plot(prices, label="Synthetic Stock Price", alpha=0.5)

plt.plot(kf.P_hat, label="Kalman Filter Estimate", linestyle="--", color="red")

plt.scatter(buy_signals, prices[buy_signals], marker="^", color="green", s=100, label="Buy Signal")

plt.scatter(sell_signals, prices[sell_signals], marker="v", color="red", s=100, label="Sell Signal")

plt.title("Kalman Filter Estimation with Buy/Sell Signals")

plt.xlabel("Days")

plt.ylabel("Stock Price")

plt.legend()

plt.grid(True)

plt.show()

The plot now shows buy signals (green upward triangles) and sell signals (red downward triangles) based on our simple trading strategy using the Kalman filter estimate.

- When the observed stock price is significantly below the Kalman filter estimate (more than our threshold), a buy signal is generated, indicating a potential opportunity to buy the stock in anticipation of a price rise.

- Conversely, when the observed stock price is significantly above the Kalman filter estimate, a sell signal is generated, indicating a potential opportunity to sell the stock in anticipation of a price drop.

Remember, this is a basic demonstration using synthetic data. In a real-world scenario, stock price movements are influenced by many factors, and any trading strategy should be approached with caution and thorough backtesting.