Is The Blockchain Ready?

Use Cases and the Real Value

A blockchain is a database being continuously expanded by record “blocks” at fixed intervals. These blocks are linked to each other by mathematical processes (cryptography), making it impossible to falsify the entries. At the same time, there is no need for a middle man anymore and the entire process is fully transparent. However, blockchain is not always the optimal solution, as storing the blocks takes time. Blockchain gathered a marketing image representing innovation a few years ago. Does it still match those expectations and should you, as an entrepreneur, use a blockchain?

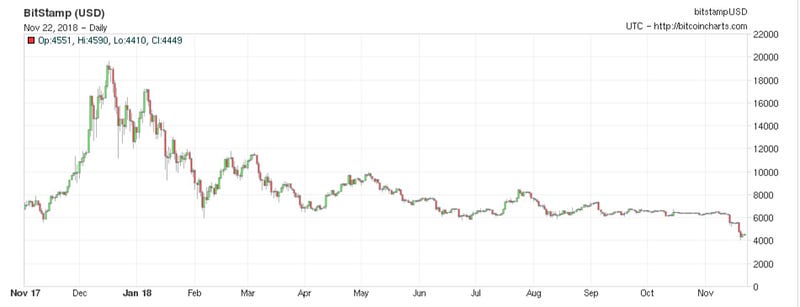

Innovations go through various stages of development. The technological initial spark is followed by a phase of euphoria, which is then replaced by a phase of disillusionment. Always. When hitting rock bottom, more mature solutions with real added value emerge. That's how it works. The blockchain sector saw such euphoria in the second half of 2017, with visionaries already dreaming of a revolution of the world. The flagship of blockchain technology at the time was cryptocurrencies. Due to the hype, these reached unimaginable highs at the time.

The inevitable Bitcoin crash casts a shadow of skepticism over the blockchain sector since then. What remained, was the continuous further development of the technology. But is blockchain technology now ready to be implemented in the real world?

Implementations

Since the Bitcoin crash in 2017, blockchain technology has been viewed more critically and realistically. There is an increased focus on the most dominant use cases for blockchain: administration, supply chain management, and applications in finance and banking. For example, the state of Malta is one of the blockchain pioneers. Since 2019, the island has a reporting requirement for leases being processed via blockchain.

Bitcoin is a remarkable cryptographic achievement, and the ability to create something that is not duplicable in the digital world has enormous value. — Eric Schmidt, CEO of Google

It’s important (especially for entrepreneurs) to understand what a blockchain is — and whatnot. Blockchain is a transparent database solution and belongs to the decentralized database systems. While traditional databases are managed by a single entity, blockchains can be shared between different actors. Bitcoin is by far the best-known blockchain example. Behind it is a public blockchain that can be used by anyone. However, there are also private blockchains, which are usually operated by organizations or companies. Well-known examples are the internet currency Libra (now Diem) from Facebook or the open-source project Hyperledger from the Linux Foundation. Private blockchains have restricted access, which means that they can only be viewed or written to a limited extent.

The Blockchain Takes the Bus

The OECD is convinced that the pace of urbanization is set to continue. And speaks of the “century of the metropolis”. According to the organization’s estimates, the proportion of the population living in cities will grow to 85% by 2100. The increasing pressure on public infrastructure poses a growing threat to people’s quality of life. But with blockchain, it doesn’t have to come so far. Whether a city is livable or not depends on many factors. The number of green spaces, medical care, rental prices. But also on the quality of public transport. Public transportation forms the backbone of large cities. But many cities suffer from outdated infrastructures that are poorly equipped to meet the enormous challenge of urbanization and the never-ending flow of tourists. To cope with the crowds and remain attractive to the population as a sexy option, transportation services must grow and adapt rapidly.

The prerequisites for a satisfactory transportation system are a clear and uncomplicated ticketing system, as well as sufficient connections at regular (and as short as possible) intervals.

A remedy for this problem could be an independent, transparent database that can be managed equally by all providers.. with a blockchain maybe?

More Efficient Collaborations

Spain is the European pioneer in the ticketing sector. Banco Santander plans to process all mass transit-related payments in Madrid through a single blockchain-based app. For the end-user, the application is simple: download the app, register, and the city’s full transport service can be used. This is a significant relief for customers, as the city’s 30 or so major transport providers are using different apps and systems. Previous attempts at a uniform solution failed due to a lack of trust. After all, no company is willing to join a foreign platform and thus develop a dependency on a competitor.

With blockchain, things are different: the database is operated equally by all partners, which protects against misuse and exploitation. Not only saving the companies word but also a tidy sum of money. In the Chinese region of Shenzhen, there are similar plans for a ticketing system as in Madrid. The annual savings through blockchain are roughly 60,000 euros — just for the paper saved.

Identifying Use Cases

What is the problem to be addressed? Can the problem be solved with a traditional database? Who is involved in the process and is a middleman required for the specific case?

Based on these questions, a company can roughly estimate which requirements a database should bring along. For companies that mainly consider internal processes, speed should play a more important role than trust. Traditional databases may make more sense than a blockchain in such cases. After all, a company should be able to trust its own employees, right? Control makes sense when a company works with external partners and wants to ensure the accuracy of database data. A collaboration in food production and food transportation, for example, involving suppliers and distributors along the value chain. In such a case, blockchain makes sense as a transparent control instance.

A public blockchain makes sense for companies when they want to share their information and data with very many different people. Take food, for example. Consumers in industrialized countries have long been demanding more transparency — especially for sensitive products such as fish, meat, or baby food. In 2008, China was shocked by a milk powder scandal. Hundreds of thousands of babies got ill from products contaminated with melamine, and at least six children died. Since then, Chinese customers distrust domestic products. With the help of a publicly viewable blockchain, producers could gain trust.

Is the Blockchain Ready?

Blockchain can do much more than just store documents in a decentralized manner. The so-called “smart contracts” can implement business logic within the blockchain by writing algorithms/processes instead of simple values to the chain. For example, the French insurer AXA already uses smart contracts for travel policies. If a flight is delayed by more than two hours, an automatic compensation payment is made to the insured’s account. Of course, technical questions about scaling or legal issues about data protection still need to be addressed to enable widespread adoption. Blockchain does not necessarily have to be better than a traditional database — but it can very well generate immense added value.