Is Buying Your Own Home in Japan Worth it?

Does it make sense to invest in your own place, or should you continue paying rent?

If you want to buy your own home in Japan, you’ll need one of two things:

- a flashy smile, a weighty wallet, and more zeros in your bank account than toes on your tootsies

- Permanent Resident (PR) status. Without it, the banks won’t give you a loan.

There are currently 880,000 PR foreigners in Japan, but I wonder how many have bought their own homes here?

In 2017, I did, after 13 years in Japan, so I’m going to give you my take on whether it was the smart move to make. Or as wise as a kid in prison.

Procreating or Profiteering?

The first thing to consider is whether you’re going to reside in the home or view it as part of your investment portfolio. After all, nothing screams rich and cool more than a casual quip about your rental joint in Japan, eh?

Forget it.

If you’re in it for wealth growth and north pointing green arrows on Excel spreadsheets, bad news. Declining birthrate, decreasing population, and simple supply and demand rules mean that real-estate profits are almost non-existent outside central Tokyo.

Buying a home in Japan only makes sense if you’re going to be an owner-occupier.

Further to that, you need a secure job that isn’t a limited contract gig that’ll end every few years and see you interviewing and moving over and over again.

The contract job merry-go-round and buying your own home is a match made in Satan’s onsen.

For me, the necessaries had all lined up by the time my wife and I decided to buy back in 2017. We’d been married 3 years, our daughter was 1, we had another on the way, and I had job security.

Boxes ticked. Here to stay. Time to buy.

Bang for Buck

Whether you’re single, partnered up, full of family, or doing it differently, buying your own home is a big investment. Perhaps the grandest and most intimidating you’ll ever make. Therefore, if you’re going to give years of tears and sacrificed beers for your own little patch of earth, you want to feel confident you’re not getting gouged on value.

For me here in Japan, it was a no-brainer.

I bought a 4BR, two-storey house with big backyard full of grass for AUD$255,000 (USD$155k). Best of all, it’s a 7-minute drive to great surfing beaches and a 10-minute drive to work. Or 20 minutes of furious pedalling on my e-bike through the rice fields.

Rural, sure. But I hate monolithic mega-cities so no probs there.

Over to Australia.

What would it take for me to get something similar in a quiet coastal surf town on the east coast, where I’m from? At best, you’re spending north of AUD $800k. In some places, like where I grew up in the south of Sydney, 6 zeros is the median. The median!

This is what the current boss of the ANZ Bank just said about buying in Australia:

“If you want a loan you have to be better off, and essentially rich.”

Gotta be rich just for a loan?

Further, The Sydney Morning Herald just led with this headline:

“Is right now the worst time to buy a house?”

And it’s not just Australia. Pop over to Zurich, in Switzerland, and Philip Skiba, a well-paid analyst working in the finance industry, says about buying a home there:

“It’s beyond luxury. Two kids, a house, a garden, two cars — I don’t know anybody who has that.”

I do. In Japan.

So, pulling the trigger on a big ole’ beachside home for AUD$255k?

Bet your house on it!

What’s Your Interest?

So, you’re in Japan long-term, you’ve decided you want to buy, and you’ve found a place you like. Next fear to contend with, how much will the banks disembowel your finances with interest rates?

Good news.

The standard rate for a fixed 10-year loan from most Japanese banks right now sits around 1.5%. Less in some places. More in others.

Once you’ve wedged your bulging eyeballs back inside their sockets, you’ll be even more stunned to learn that our fixed 10-year rate, set back in 2017, is 0.75%.

Less than 1% for another four years? Happy days!

What does that mean in terms of dollars, savings, spendings, or being forced to make a profile on OnlyFans to cover costs?

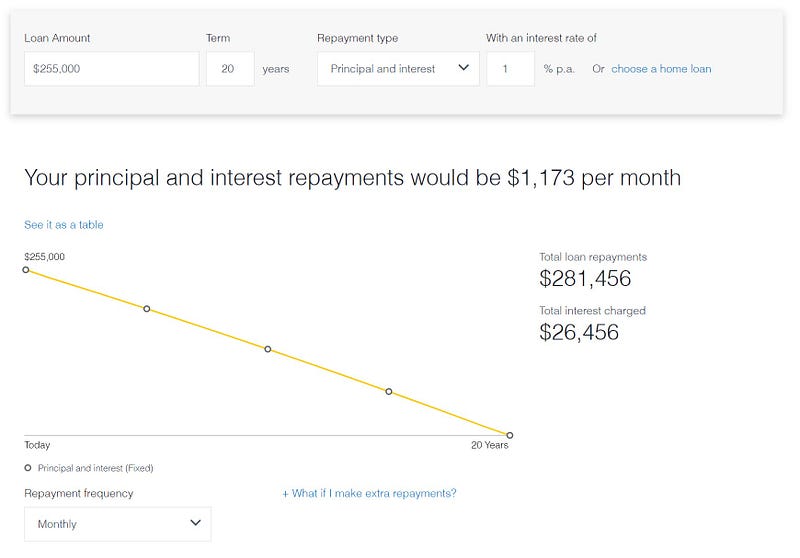

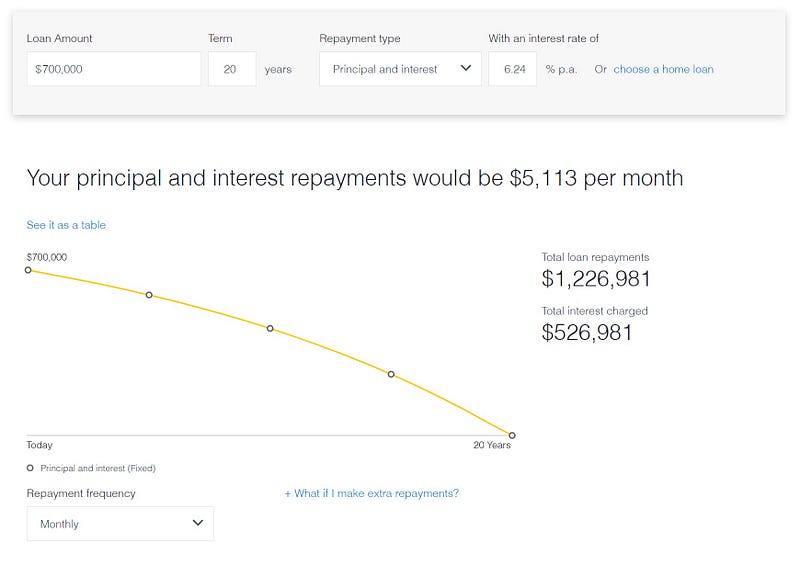

Take a look at these interest repayments calculator graphics below.

In Japan, I borrowed pretty much the full amount of the loan — AUD$255k. Over 20 years, at an interest rate of 1% (accounting for an increase in our rate in 2027), I’ll have to repay a total of $281,000 — $26,000 in interest to the bank. Not bad.

What about Australia?

If I borrowed a conservative AUD $700,000 at the current variable rate of 6.24%, my total repayments after 20 years would be… $1,227,000.

$1.2 million? Are you frikken kiddin’ me? $526,000 to the bank in interest repayments alone?

That’s more than 2 extra houses for me here in Japan. With those kind of savings, I could become a real-estate mogul!

Again, I’ll take Japan, thanks.

You’ve Gotta Pay Anyway

Remember, we’re talking about long-termers in Japan here, not teachers or other workers who plan to stay for a few years of fun and experience and then skedaddle home.

So, if you’re intending to stay put in The Land of the Rising Sun for decades, then it makes no sense to me that you don’t buy. The main reason being that you have to pay rent during that time anyway.

Before buying my place, I rented 4 times in different locations. The monthly total for each, including a carpark, was:

- ¥72,000

- ¥74,000

- ¥64,000

- ¥80,000

So, let’s just average that out for argument’s sake and say rent is ¥72,500 for me.

I paid that from 2005–2017. 12 years, or 144 months, at ¥72,500? ¥10,440,000.

In USD at the current rate, about $70k. AUD, about $105k.

No dramas, as I was single, free, and unsure about my future for most of that time.

Then I committed to Japan and decided to buy a place in 2017 because I knew I was going to be here long-term and didn’t want to continue watching my money disappear on rent.

I got a 20-year mortgage as I saw myself here that long.

If I’d opted to pay rent, instead?

20 years is 240 months. 240 months paying ¥72,500? ¥17,400,000.

That’s about 70% of my ¥25,000,000 bank loan.

But I’d never see that money again. Worse, I’d be lining some landlord’s pockets. By buying my own home, that money is essentially going to myself and my family, and when I’m done paying the house off, my wife and kids will have the security of a roof over their heads for as long as they’re alive.

That’s a huge incentive for me.

Why pay rent for 20 years when it’s not much more to get your own home and set yourself and/or your family up?

Plus, once I’m done paying the bank loan, I won’t have to pay anything to live in it for all the years I’m left alive, aside from some taxes here and there (which are still way cheaper than paying monthly rent).

What’s the Smart Move?

If you’re intent on staying in Japan long-term and you have a secure job, then I think it makes a lot of financial sense to invest in your own home, for reasons such as:

- Value for money

- Low interest rates

- Renting or buying, either way you gotta pay

I don’t regret my choices for a moment, but I’d love to hear your thoughts on the topic.