Fundraising Strategy for Early-Stage Startups (№2 of Series)

Basic Understanding Before Fundraising — Angel Investors

This is the 2nd article in the early-stage startup fundraising strategy series. You may find the links of related readings at the end of this article.

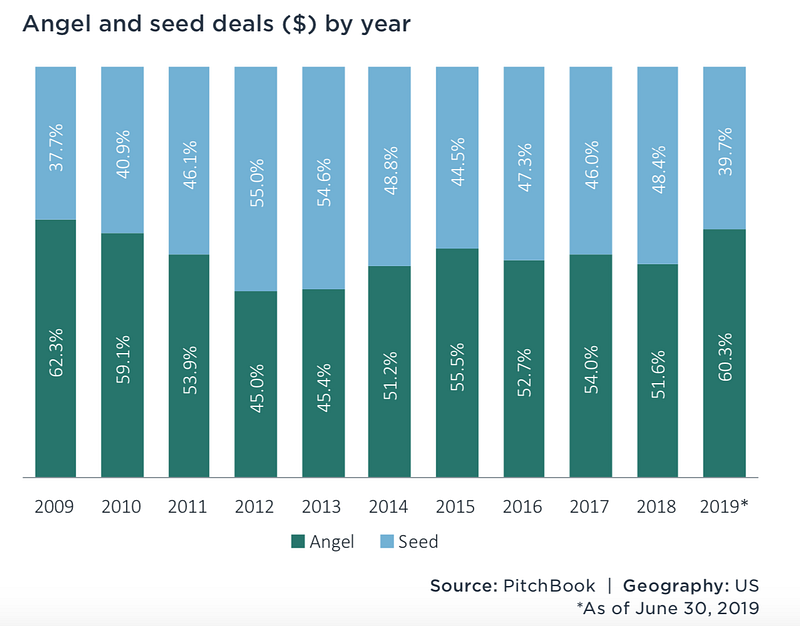

My first article under this series of “financing strategy for early-stage startups” starts with institutional investors’ introduction as they are the main type of investors startups work with in fundraising. However, when startups do fundraising, their first-round is not always led by institutional investors like VC firms or accelerators. On the contrary, the angel round or pre-seed round fundraising will likely be led by individual investors, namely angel investors. According to Pitchbook (PitchBook), majority pre-series A deals that have taken place in H1 2019 is angel round financing (refer below).

1. Angel Round vs. Seed Round

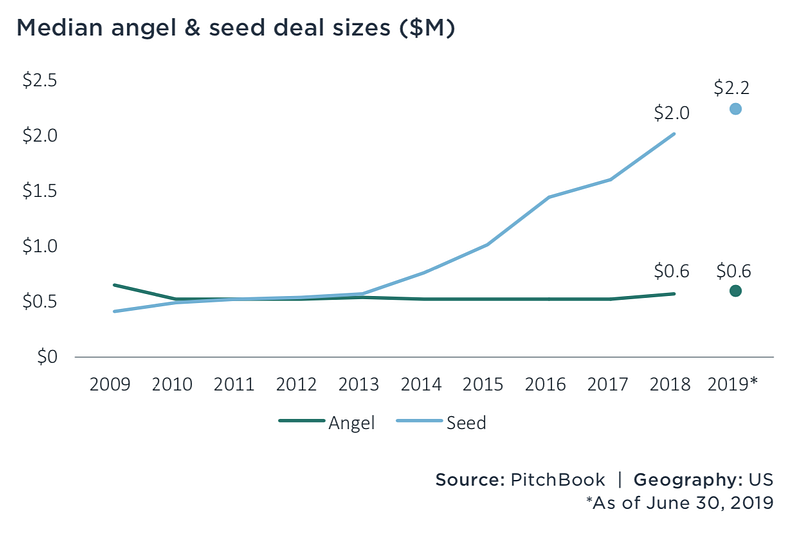

The difference between the angel round and seed round is mostly about the funding size. Pitchbook indicates that in H1 2019, the median financing amount of angel round is $0.6 million while the median size of seed round has climbed up to $2.2 million (refer below). Another unsettling fact shared by Pitchbook is that the median age for startups to close angel & seed round financing in H1 2019 is 3.1 years, up 10.9% from full-year 2018, which is historically high.

One result of the bigger check of a seed round is higher valuation. According to CooleyGo, the median pre-money valuation of seed round financing at Q2 2019 is almost $10 million. Another byproduct is that the measurements to invest in seed round are higher. Metrics on high growth and market fit validations are expected to be delivered when VC firms value early-stage deals.

Angel round financing remains almost the same level at its financing amount. When companies grow, the variables become more. The valuations for companies and the capital companies need to achieve the next milestone differ greatly. But the angel round reflects the minimum capital to take off and, except for certain heavy capital industries such as biotech, most early-stage startups shouldn’t need that much money at the beginning.

Investors that invest at the angel round are usually angel investors and accelerators, and occasionally some VC firms. Accelerators have very different business models and with main revenue coming from consulting or working space leasing. But accelerators are still institutional investors and they operate based on their corporate governance and rules, which make them act more like VC firms than angel investors.

2. Angel Investors vs. Institutional Investors (VC Firms/Accelerators)

Closing Speed: Angel investors invest with their funds, so they don’t have mandates to follow. Institutional investors have sophisticated operation rules and have fiduciary duties towards external investors (LPs). Institutional investors have to spend time to follow procedures to mitigate risk by conducting due diligence, requiring specific deal structure, and asking for fund-customary terms. On the other hand, angel investors vet deals based on their philosophy and care more about upside earnings instead of downside protection. Thus, when founders pitch deals with angel investors, it usually takes much less time and a simpler procedure to close a deal.

Mentorship: Many angel investors are entrepreneurs and industry experts. One big motivation to have angel investors on board is to get investors’ in-depth and personal involvement and guidance for early-stage startups. If the founder is very well connected, she/he may even handpick angel investors who are specialized in different domains, and complement the talent pool and extend the networking. Institutional investors assign a designated partner or senior executive as a board member, board observer, or liaison for post-investment portfolios. They provide more value based on the fund’s networking and strength rather than personal contribution.

Negotiation Position: As angel investors are in general not as sophisticated as institutional investors, startups usually find themselves in a better position to get deal structures and deal terms more in favor of founders and the companies. It is also possible that startups can even hand the terms to investors and lead the whole negotiation with its lawyer, but not the other way around. In this way, founders can save time and money to close deals and have more control of the company at the time by not giving the board seat and having fewer minority shareholders’ protection terms.

Number of Investors: Angel investors write smaller checks than institutional investors. How big amount does an investor usually invests is a key fact for founders to check before pitching. Depending on how much a startup needs at angel round, founders may have to raise funds from more angel investors than institutional investors to fulfill the funding goal. Some angel investors have great personal networking of investors and she/he may lead a group of investors to invest in a deal individually or as a syndication group. Managing shareholders require time and money. Founders should put this into consideration and optimize a deal structure by not having too many direct shareholders at the company level.

Follow-on Investment: Angel investors usually do not participate in follow-on fundraising, but institutional investors do. This means when founders at startups with angel investors raise next round, she/he needs to initiate new pitching. Institutional investors also have more extensive networking within its circle and introductions to other investors are very useful. Thus, startups backed by institutional investors have more resources to do their next round financing.

3. When Founders Should Consider Angel Investors

A startup should never dismiss angel investors for their first-round financing, even if the angel investors are not the leading investors. As mentioned above, angel investors may bring personal networking and mentorship to startups where institutional investors cannot. Having industry leaders to back a startup is self-evident.

If a startup does not need a big check to achieve its next milestone, pitching angel investors could be a good strategy to consider. Founders can start with family and friends to see whether they can fund the startup. If that’s not sufficient, founders may leverage personal networking and online platforms, such as AngelList.

In scenarios where founders are not eager to turn their startups into a publicly traded company, they may not find favor in the eyes of institutional investors. Institutional investors’ business model dictates that they pursue the high growth and high potential to exit either from an IPO or an M&A. However, these startups may be liked by angel investors for various reasons. For example, food & beverage industries are not easy to scale and some dedicated investors are interested in this sector. Rather than pushing for an IPO as a single goal, these investors focus more on revenue sharing.

4. Conclusion

Angel investors are very different compared with institutional investors. Even within angel investors, there are different approaches based on founders’ networks. It’s harder to systemize how to raise capital from angel investors than institutional investors as the market data is not as transparent as it is for VC firms and accelerators. Some angel investors may not have gained enough exposure to become a mature investor to handle the deal. There could be surprises when you do angel fundraising. But the methodology and principles are similar. Pitching to investors is essentially a sales role, which is all about doing homework, having a clear plan, telling an appealing story, and closing the transaction.

Disclaimer

This article should not be construed as or relied upon in any manner as financing, investment, legal, tax, or other advice. Readers should consult your own advisors as to legal, business, tax, and other related matters concerning any financing or investment activities.

Related readings: