Investing in a Bear Market

How to stay sane as Coronavirus drives investors crazy

If you haven’t noticed, the stock market hasn’t been doing so well recently.

The S&P 500 closed at 2,741.38 on March 11, down 15% on the year and down 17% since its high in late January.

I’m honestly not sure what’s scarier to investors right now, what the Coronavirus can do to the human body or what it’s doing to the stock market.

With fear running rampant, it’s time to try and put our emotions aside and look at things logically so we don’t panic and shoot ourselves in the foot like everyone else. Let’s start by examining two very different approaches to investing:

Buying and Selling Based on Market Activity (Timing the Market)

This is the default way that our brains want to view investing and the presence of the 24-hour news cycle exacerbates this bad habit.

It seems so simple: buy low, sell high. If it seems like the market is going to drop, sell. If it seems like it’s going to rise, buy. Don’t get caught with a bunch of money invested in the stock market when it takes a big dip.

Here’s the problem: no one — and I mean NO ONE — knows what the market is going to do. This doesn’t take a lot of evidence to demonstrate, here’s the simple proof: if someone could reliably time the market they would be obscenely rich.

The reality is that even when the market starts going down, you don’t know how far it will go or when it will turn around. Coronavirus panic might keep driving the market down, or this may be the very bottom and the exact perfect moment to buy. You don’t know.

What ends up happening is that people who try to time the market nearly always end up doing the opposite of what they intended: they end up buying high and selling low. It goes like this: the market is going up so the buy, then it goes down and they sell thinking they made a mistake and need to cut their losses. They buy high and sell low.

The problem is further confounded when you realize the market is bound to take several large dips during the course of your investing career. For each major drop, you need to be right twice — once when you sell at the top and once when you buy at the bottom.

Buying and Selling Based on Your Stage of Investing

The alternative to timing the market is to have a robust investing strategy that works whether you’re investing in a raging bull or a fearsome bear.

Personally, I think the strategy that makes the most sense for figuring out when to buy and when to sell is one based on the stage of your investing career. I use the categories below created by JL Collins, author of The Simple Path to Wealth and the excellent stock series:

The Wealth Accumulation Phase

The reason why you’re investing money is so that it can grow into more money. Your money starts making money and eventually it makes enough that you don’t have to keep working.

During the wealth accumulation phase, you invest as much money as you can as quickly as you have it. Yes, sometimes the market goes down right after you put some money away, but far more often it goes up, so getting invested earlier is almost always than waiting in the long run.

During the wealth accumulation phase, you have several things going for you that help make market crashes less scary:

- You’re putting money away with each paycheck, so a dip in the stock market is just an opportunity to buy stocks on sale

- You aren’t selling shares, meaning your losses are only “paper” losses. You still own the same number of shares, it’s just that if you sold them right now you’d get less for then than you would have before the dip

- If you invest in a good index fund like VTSAX and have your dividends automatically reinvested, your portfolio will keep accumulating shares of stock (at a discount) even without additional investment

The wealth accumulation phase is where I’m at right now, and most of my previous writing on investing focuses heavily on this stage:

The Wealth Preservation Stage

In the previous stage,market crashes could be safely ignored. If you are investing money consistently and have time to wait out the storm, you’re going to be fine. But if the market takes a dive during a period where you need to take money out, you’re in trouble.

One way to protect your money is to take it out of the volatile stock market and put it in a more conservative investment. There are two problems with this approach:

- Inflation is constantly eating away your purchasing power and most conservative investments have trouble outpacing inflation (low risk, low reward)

- The stock market is possibly the greatest tool in human history for passively building wealth. It’s tough to sit on the sidelines and watch other peoples’ money grow

Another approach is to diversify your money among asset classes (if you invest in index funds you are already diversified in terms of companies and industries).

If we try to reason from first principles when picking an asset class to use to curb some of the risk from the stock market, I think we’ll come up with two criteria:

- We want an asset class that’s less volatile than the stock market

- We want an asset class that isn’t correlated with the stock market

In my mind the solution is clear: we want bonds.

Bonds don’t experience the crazy swings in value that stocks do. Sometimes they lose money, but the key is that most of the time they go up in value, and when they do lose money, it’s not a catastrophic crash like we saw with stocks in 2008.

The other nice thing about bonds is that they don’t seem to be correlated with stocks at all. Bonds can go up in value even when stocks go down.

Contrast this with the international stock market, another popular tool for diversification. The international stock market is more volatile and can experience wilder swings than the US Market. Even worse, both the US and international markets seem to be very highly correlated with each other; when one is going down the other one is likely to be as well.

Bonds allow us to diversify our investments to protect us from losses.

But the real value of bonds is that they force us into good investing behavior: buying low and selling high. Let’s illustrate using some real numbers from this year.

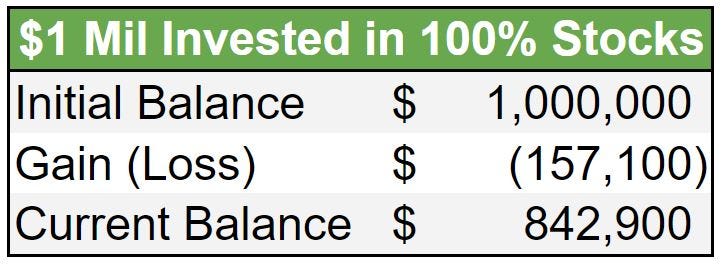

According to Vanguards website, their total stock market index fund VTSAX is down 15.71% so far this year. This means that if you are in the wealth preservation stage and started the year with a million bucks, you’re down a lot of money:

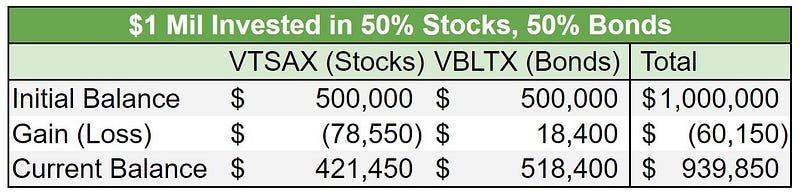

But according to Vanguard, their total bond fund (VBLTX) is up 3.68% so far this year. Here’s what your million dollars would look like at the moment if it was split between stocks and bonds:

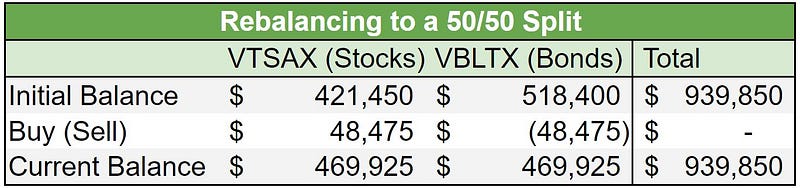

Here, only half the portfolio was exposed to a loss, and the other half actually experienced a gain. But the best part is what happens next. If today was the time where you were scheduled to rebalance your portfolio, you would need to sell bonds and buy stocks to get back to a 50/50 split:

In this situation, you are selling almost $50k in bonds and buying almost $50k in stocks. The stock market has gone on a huge sale and you are poised to take advantage of it.

Because rebalancing causes you to sell the asset that appreciated the most, you end up “selling high” relatively speaking. And because you are buying the asset class that performed poorly, you are “buying low.”

You don’t need to worry about timing the market, you just need a strategy that takes advantage of the current situation.

Of course, there is always a risk in investing and even a diversified portfolio isn’t ever fully safe.

But to have money is to have risk. If you invest it in any form, you might lose money. If you stash it under the bed, your house could burn down. If you leave it sitting in the bank, inflation will eat away its purchasing power.

You don’t get to choose whether or not to take on risk, but you do have some influence over how much risk you are exposing yourself to as well as how much upside.

The upside to the stock market is high and the risks can be mitigated — if not eliminated — by a sensible strategy.

My strategy calls for saving money during this stage of my life, so whether this dip turns into an extended bear market or we see the return of the raging bull of the 2010s, I’m not changing what I’m doing.

This article is for informational purposes only, it should not be considered Financial or Legal Advice. Consult a financial professional before making any major financial decisions.