Risk Management: Understanding Credit Risk

This article serves as an overview of counterparty credit risk and outlines terminology used in credit risk management. It also explains how credit risk can be measured, reduced and mitigated. This article will help form a solid foundation for credit risk management.

Article Structure

The article is composed of three parts:

- Credit Risk Management Importance

- Measuring Credit Risk

- Reducing Credit Risk

Please read the disclaimer before proceeding.

Credit Risk Management Importance

Credit risk management is a major component of risk management in financial organisations. A large team is dedicated to calculating credit risk measures. The team includes technologists, financial and quantitative analysts. Credit risk measures help the management board in making calculated decisions to mitigate risk and further increase return.

What Is Counterparty Credit Risk?

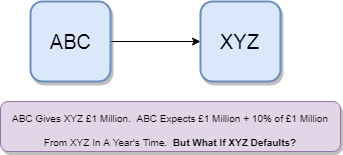

Assume:

- ABC and XYZ are two financial institutions e.g. banks.

- ABC lends XYZ £1 million pounds loan at 10% interest for 1 year.

This means ABC will receive £1.1 million pounds back in a year’s time from XYZ. But what if XYZ defaults?

Counterparty credit risk for ABC is the uncertainty that its counterparty XYZ is unable to meet the contractual obligations and will default before paying the money back.

If XYZ defaults, ABC will lose the money. Credit risk management teams measure credit risk for transactions that can expire in future. The transactions could be simple as explained in the example above or they can be complex in structure.

Counterparty credit risk can be bilateral (two-way) in nature.

Counterparty credit risk is 2-way when both counterparties exchange a series of payments periodically such as in interest rate swap transactions as explained in my Derivatives blog.

In short, counterparty credit risk for each party in a transaction is that the counterparty might fail to meet its financial obligations.

Some trades are considered to have zero counterparty credit risk

- Counterparty credit risk is mainly present in security financing and OTC derivative trades. Exchange Traded contracts, for example, Futures, do not have counterparty risk as the counterparty in Exchange Traded contracts is the Exchange itself.

- In theory, there is a small credit risk present in exchange-traded contracts because exchanges have a very low probability of default but holistically, exchange-traded contracts can be considered credit risk-less.

- Counterparty risk is calculated at trade, portfolio and counterparty levels.

How Do We Measure Counterparty Credit Risk?

Credit risk measures can be used to take calculated decisions. These decisions can help organisations manage risk better. Measuring credit risk starts with pricing your transactions. Once we know the value of trades, we can measure credit risk. There is always a possibility that a counterparty in a contract might default. Subsequently, some counterparties have a very low probability of default such as Exchanges or Central Clearing Houses, while others have a high probability of default such as D-rated counterparties.

There are a large number of risk metrics available to calculate credit risk exposure. All of these measures have their own calculations and uses. This section outlines common risk measures and their types.

Let’s Understand Risk Measure Types

There are essentially two classes of risk measures:

- Scalar risk measures are measures that represent risk as a single value i.e. one value to represent exposure for the entire life of contracts with a counterparty.

- Profile risk measures are measures that represent risk over a time period i.e. one value for each time point.

Trades are grouped into groups such as netting sets. A number of risk measures are then calculated at each netting set level and they are then summed across the netting sets to reach counterparty level. Risk measures can also be aggregated across different groups such as product type, books etc.

Let’s Briefly Discuss Counterparty Credit Risk Measures

We can utilise mathematical formulae to price the current value of all transactions. However, this calculation will be based on the state of current market data. Market data is constantly changing and hence the price of transactions is also varying over time. Additionally, we are required to compute credit risk exposure for future dates. Therefore to accurately price transactions over the lifetime of a portfolio, advanced mathematical sampling and forecasting techniques are being used.

The credit risk methodology team, therefore, utilise the Montecarlo simulation technique to simulate market data on a range of scenarios. These scenarios are generated over future time points. These scenario-specific market data points are known as simulated paths. The simulation of market data relies on the probability distribution of variables such as interest rate curves. Trades are then priced on the simulated paths.

The price of a trade is known as Mark To Market (MtM). MtMs across scenarios and time points are calculated and they are then used to calculate a number of risk measures. These risk measures are combined with other inputs such as the probability of counterparty default, the recovery rate of getting money back from the counterparty along with a range of other statistical measures to compute credit risk measures.

This section briefly highlights the common risk measures.

Expected Mark To Market (EMtM):

Price of a transaction is calculated from its cashflows during the lifetime of a contract. EMtM considers both positive and negative amounts. EMtM profile is one MtM value for each timepoint.

Expected Exposure (EE):

EE amount indicates the positive amount that the trading party will lose if the counterparty defaults. Negative MtMs are capped to 0. EE is a profile risk measure and is the average of MtM distribution. EE is usually greater than MtM.

Negative Expected Exposure (NEE):

This is a mirror image of how EE is calculated. Positive MtMs are floored to 0. NEE tells trading entity how much counterparty is exposed to it. NEE is a profile risk measure.

Expected Potential Exposure (EPE):

Once EE is calculated, an average value of EE is computed. EPE is a scalar risk measure.

Expected Negative Exposure (ENE):

Mirror image of EPE. It is the average value of NEE. ENE is a scalar risk measure.

Effective Expected Exposure (EEE):

For each time, maximum of (current EE value and maximum EEE) is selected. This then results in increasing EE profile. EE is a profile risk measure.

Effective Expected Positive Exposure (EEPE):

EEPE is the average of EEE profile. EEPE is a scalar risk measure.

Potential Future Exposure (PFE):

Based on a confidence level (e.g. 97.5 percentile or 99 percentile), the distribution of MtM is computed and a value is taken from the distribution for each time point. We can think of PFE as the worst case scenario exposure to a counterparty. PFE is usually greater than EE. PFE is a profile risk measure.

Potential Exposure (PE):

As PFE is calculated over a number of time points, PE is the maximum value of PFE across all time points. PE is greater than PFE. PE is a scalar risk measure. I have also seen PE as a risk measure profile whereby maximum PFE of each timepoint is selected to create a peak exposure profile.

Exposure At Default (EAD):

EAD is a scalar risk measure. It is calculated as EEPE x 1.4

Credit Value Adjustment (CVA):

CVA is the market price of a counterparty. This amount indicates how much a trading entity should charge the counterparty. It is calculated as:

Sum of EE x Counterparty Probability of Default (time point) x (1-Counterparty Recovery Rate)

Probability of default indicates the chances of a counterparty defaulting. It is usually calculated from credit spreads.

Recovery rates indicate the amount that can be recovered if the counterparty defaults.

There are also different measures related to CVA e.g. incremental CVA which is the impact on CVA if a transaction is added and marginal CVA which is netting level CVA disaggregated to trade level CVA.

Funding Value Adjustment (FVA):

Amount banks need to keep if they are trading in OTC derivatives.

Default Value Adjustment (DVA):

Market price of a trading entity to the counterparty. It is a function of

Sum of NEE x Trading Entity Probability of Default (timepoint) x (1- Trading Entity Recovery Rate)

Bilateral Credit Value Adjustment (BCVA):

It calculates net effect of CVA and DVA and is calculated as CVA + DVA.

Capital Value Adjustment (KVA):

To support uncollateralised OTC derivatives.

Margin Value Adjustment (MVA):

Amount required to support posting of collateral.Note, netting and collateral can reduce counterparty credit risk measures.

In this section, I wanted to concentrate on the PFE profile shape as it is one of the most common credit risk measures.

Let’s Understand PFE Profile Risk Measure

Once PFE is computed for a set of time points, for example, 100 years, it can be drawn on an XY line chart with time points on X-axis and exposure on the Y axis. The shape of the line chart can help us understand counterparty credit risk and portfolio decomposition better.

Let’s consider a portfolio of trades.

Assume:

- All trades are with a single counterparty

- All trades belong to a single asset class e.g. FX or Interest Rate etc.

- Now consider that the trading entity runs a Monte Carlo simulation that simulates market data for each future time point and then calculates MtM for each scenario within the time point.

- PFE is computed after taking netting and collateral into account. PFE profile is finally produced over future time points.

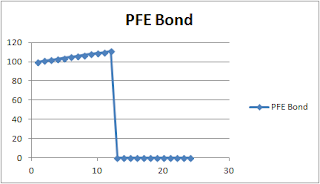

Consider A Portfolio Of Trades With Only Fixed Income Trades

For example Bonds or Repos of £100

PFE at each timepoint is approximately equal to the notional value of the trades as shown below, £100 in this case.

We can see a gradual increase in exposure due to interest until payments are paid. When the payments are paid from the counterparty, exposure drops are 0.

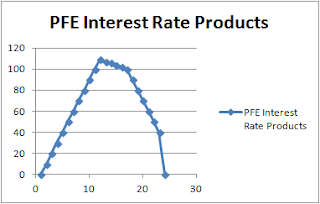

Consider A Portfolio Of Trades With Only Interest Rate Products

For example Interest Rate Swaps

PFE is upside-down U-shaped and results in the peak in the middle of the profile. This is due to rollover risk, interest rate risk and frequent payments over the life of the interest-rate products. Interest rate risk always results in slowly increasing and then slowing decreasing profile.

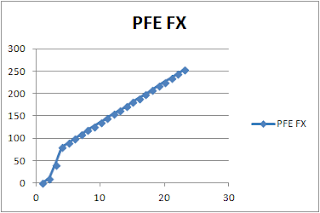

Consider A Portfolio Of Trades With Only Foreign Exchange Products

For example FX

FX trades are exposed to exchange rate risk. High exchange rate volatility results in an increasing profile:

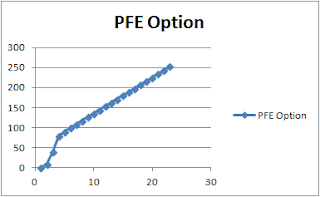

Consider A Portfolio Of Trades With Only Options

For example: Call/Put Options

We can see an increasing profile until the option is exercised.

The profiles are non-zero for the life of trades. This implies PFE of a portfolio after 9th-year timepoint will be 0 if all trades mature within 9 years.

How Is Counterparty Credit Risk Reduced?

Counterparty credit risk can be reduced by diversification, netting and collateral.

Diversification

Counterparty credit risk can be transferred by diversifying and entering contracts with a large number of counterparties with different probabilities of default. For example, a trading party can enter into some of its contracts with an Exchange.

This is known as Diversification And Hedging Risk by entering trades with a range of counterparties to reduce the counterparty credit risk.

There are several rating agencies such as Fitch And Moody’s, S&P etc. that gather valuable information on counterparties to provide counterparty credit ratings.

Netting, Closeouts And Collateral

There are several other ways to mitigate counterparty credit risk too. These methods include netting, closeouts and collateral.

How does Netting Work?

Netting is often referred to as offsetting.

- Derivative trades are priced and their value is calculated. This is known as calculating transaction mark to market (MtM). Each transaction is priced using its own mathematical model. In general, cash flows are calculated and summed across the maturity of the trade to calculate the price of a trade.

- The price can either be negative or positive. A negative amount implies what you owe your counterparty whereas a positive amount reflects the money that you require from your counterparty.

- Trades can be grouped together if they belong to the same legal agreement such as ISDA. If a group of trades belong together then their grouping is known as a netting agreement. It is also known as a netting set. Netting agreements can be bilateral (involves the trading party and the counterparty) or multi-lateral where a group of counterparties are involved to reduce the credit exposure.

- Prices of grouped trades are summed to produce a single value. As a result, positive and negative prices end up netting or cancelling each other off.

- If a group of trades do not belong to a netting agreement then the negative MtMs are ignored and negatives are capped at 0.

- As a result, without netting sets, negatives are ignored whereas netting sets reduce exposure because a positive amount is offset by a negative amount in a netting set.

Reduction in exposure reduces counterparty credit risk.

Netting Calculation With Example

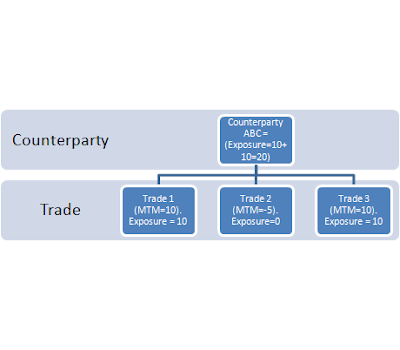

The diagram below illustrates a set of trades in a portfolio and how total exposure is reduced due to netting sets:

The diagram below illustrates that the exposure without netting set presence is £20. MtMs of all trades are summed to give us exposure of £20.

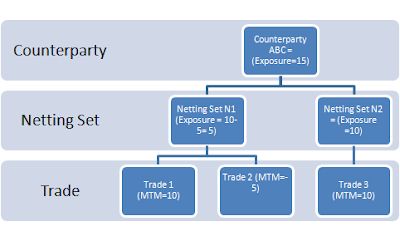

We can reduce credit risk exposure by introducing netting sets.

As shown in the image, exposure is £15 at the counterparty level. This reduction is due to the grouping of trades within the netting sets. Without being set, it would have been £20. Netting set, therefore, reduces counterparty credit risk.

What Is A Netting Factor?

For netting across different asset classes, a netting factor is calculated as:

Netting Factor = Square Root (Number of exposures +(Number of exposures — 1)) /Number Of Exposures)

A higher Netting factor implies lower netting benefits. The netting factor decreases with a larger number of exposures.

How Does Closeout Work?

When the counterparty defaults, all of its contracts are closed. Closing out is the process of immediate transfer of the netted amount to the trading party. If a trading party owes a counterparty money then the feature that allows a trading party to terminate the contracts when the counterparty defaults is known as walkout.

Credit risk can also be reduced by posting and receiving collateral.

How Does Collateral Work?

Collateral is also known as margining. Two parties can enter into a collateral agreement. A collateral agreement outlines the collateral amount that the parties need to post to reduce counterparty exposure. Collateral agreement is also known as Collateral Support Annex (CSA) which is a document associated with a netting agreement. The CSA document outlines collateral rules. When a CSA exists between two counterparties then firstly trades between the trading party and counterparty are netted together and then the collateral calculation is applied.

Not only collateral reduces counterparty credit risk, it also reduces capital required to trade with a counterparty.

It’s Important To Understand Collateral Support Annex (CSA)

When a CSA is part of a netting agreement then parties are required to post collateral on a periodic basis.

Let’s Understand the Role Of CSA

The presence of CSA can reduce counterparty credit risk as counterparties are obliged to post collateral.

Are there any issues with posting collateral?

Posting of collateral has administrative and transactional costs associated with it therefore collateral is only posted on a timely basis.

How does collateral work?

The collateral amount can reduce the exposure to 0

- If the netted amount is negative then the trading party posts the collateral amount to the counterparty.

- If the netted amount is positive then the trading party receives a collateral amount from the counterparty.

CSA Properties

CSA outlines a number of important legal details, for example how to resolve disputes, timing of collateral, rounding of collateral and credit quality etc.

In this section, I will highlight a number of useful parameters that are stated in a CSA:

- Initial Margin (IM) or Independent Amount (IA) — Amount required to enter into a contract. It is mainly dependent on the credit quality of a counterparty and not on the exposure level.

- Minimum Transfer Amount (MTA) — Amount that can be recalled by a counterparty at any time.

- Threshold — MtM of a netting agreement can alter on a daily basis and can result in 0, positive or negative value. As negative MtM implies posting collateral amount, posting of collateral has its own administrative costs associated with it. The threshold is the minimum MtM amount that needs to be exceeded before collateral can be posted.

- Collateral Amount — The collateral amount that counterparties can call.

- Haircut amount — Amount to reduce the value of the collateral. It accounts for the possibility that the collateral amount can fall between a previous collateral call and a counterparty default. Haircut “cuts” the collateral amount that is required to be posted. Collateral can be posted in cash, government bonds, MBS, equity etc. The discount (haircut) is expressed in percentage and is dependent on the type of collateral posted. For example, a haircut of 2% implies 2% of the collateral amount needs to be posted. Riskier assets have a greater haircut percentage. Cash has the least haircut percentage.

What Is CSA Direction?

CSA can be one or two ways and it dictates who posts collateral. The direction of a CSA is usually dependent on the credit quality of the counterparty.

Summary

Counterparty Credit Risk is a big area in risk management. This topic introduced counterparty credit risk and highlighted common terminology used in risk management. It also explained how credit risk can be measured, reduced and mitigated.

Hope this article introduced you to the counterparty credit risk. Please let me know if you have any feedback.