Impact Venture Debt in Africa: 5 things we learnt co-building the Young Entrepreneurs Fund

We have a real and urgent need to re-invent financing instruments for entrepreneurs in Africa, this issue is especially acute among the young which in addition to being ignored by banks, commonly do not yet have sufficient social capital and networks to access alternative financing sources like angel investors.

Over the last few months, backed by Omidyar and together with the team at the African Leadership Academy (ALA), we’ve structured a simple, rules-based, matching debt fund for young entrepreneurs — and these are a few of my initial lessons.

We intend to be as open source as possible with the Young Entrepreneurs Fund (YEF) and will continue to share more insights in the coming months. Oh and if you’re looking to launch a fund or would like to learn more about the work we’ve done please do reach out directly too!

1. Focus on CORE competency

The African Leadership Academy is one of Africa’s leading institutions when it comes to training young leaders and through it’s 15 year history has seen 1000's of bright aspiring changemakers come through its doors, most for its flagship diploma program, but also for other programs like the Anzisha program for Very Young Entrepreneurs (VYEs).

It’s 3 key competencies are a) Identity Potential b) Simulation & Practice and c) Connect to Opportunity.

A large part of how early stage investors make decisions is really through identifying founding teams with high capability, drive and integrity, something which ALA has a 15 year history for doing exceedingly well (McKinsey, Dalberg and many other top firms jostle for its graduates every year).

The team did not presume to understand how to evaluate the market potential of very specific businesses in the wide spectrum of markets that exist in Africa but they sure could spot and vet the individuals that could.

Hence, the decision to focus on building a matching fund, which would rely on on-the-ground investors to give the fund that capability.

Could ALA have built that capability to deeply understand these markets over time? Absolutely, but to truly deliver immediate additionality to the markets it operates in — the team focused on that bit of the value chain they do incredibly well — talent identification and training.

2. Listen, Get Creative, Build for Purpose

I felt ALA had a deep culture of constantly iterating and enhancing its interventions to achieve ever stronger outcomes for the aspiring leaders that go through its programs — the approach to the fund was no different.

The team and I went through a heap of interviews with potential recipients across the spectrum of stage, background, country and sector. To really help them understand the fund’s objectives and help us co-build something that would actually fill a gap they see firsthand.

We asked for perspectives on all elements of the fund’s terms and processes from its potential recipients.

Listen. Because what is the point of a fund that isn’t deployed?

We wanted to creatively offer month-on-month flexibility and found that the idea of a revenue share arrangement not only allowed the entrepreneur the comfort of knowing we won’t come knocking if she went through a few months with no revenue and was unable to make payments. (incidentally, the idea of revenue share is increasingly gaining prominence — at least in discussions- as an alternative to equity in tech startup VCs)

But with monthly payments varying — which has the minimum tenure of the loan potentially also in flux — how do we then approach interest rates? What is a fair interest rate across the wide variety of markets the fund will serve? But perhaps most importantly:

How do we communicate a simple number that doesn’t complicate it with terms like effective vs nominal rates, principal vs interest payment allocations, compounding vs. simple?

We landed on something our recipients overwhelmingly understood, total return.

Once funding was disbursed, the total amount outstanding was either 1.05, 1.2 or 2x, payments were still flexible and revenue linked but founders had a clear idea of what was due from Day 1 — and this number did not change.

3. Stay Simple, Stay Firm

One further challenge we gave ourselves was to keep this as rules-based and simple as possible. From the ground up we designed simple decisioning criteria vetted by our board of industry leaders like Sawa Nakagawa, most recently CEO of Allan Gray’s E Squared investments in South Africa.

Without a deal-by-deal investment committee and with clear published criteria, our founders were much more confident when they applied — knowing exactly the bar they need to hit to be issued a Letter of Guarantee (LoG) from the fund.

What we also were lucky enough to see is that despite requests for exemptions, like disbursement of funds before the funds to be matched were evidenced in the business’ accounts, by sticking to the published requirements — the right founders had no problem overcoming challenges to meet these.

It feels sometimes that impact investors or entrepreneur support organisations (ESOs) are pushed to make all kinds of customisations and go out of their way to meet the needs of the founders they want to support — I’m proud that with the Young Entrepreneurs Fund, we’ve been sticking to our processes and requirements, no exception.

4. The power of the community is amazing

I just wanna dedicate this whole bullet point to everyone that’s volunteered help and advice — many really going out of their way to help us think through this. You know who are .

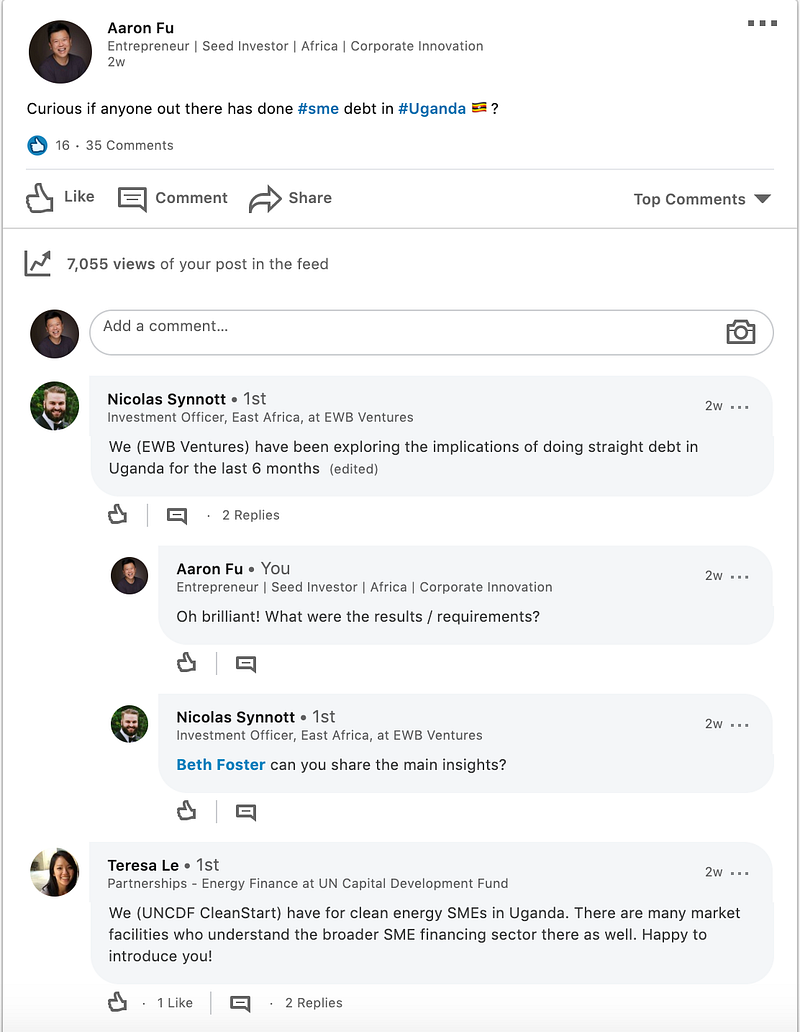

But one specific case I do want to share though is this, we wanted to get a better sense of the regulations and considerations around funding one of our prospective fund recipients in Kampala — I put up a simple one-liner on LinkedIn.

Curious if anyone out there has done SME debt in Uganda?

Within a few days, there were 35 comments — all sharing advice and pointers to people we should be speaking with.

What we’re doing isn’t easy but man is it helped along by a collaborative and generous community of investors and enablers driving the ecosystem forward.

5. Expect the Unexpected

The fund structure went through dozens of revisions, most often as we discovered country specific inbound or outbound regulations.

Guess this is what it feels like to be on the frontier, where most of what you’re trying to do isn’t explicitly regulated and/or is a micro-percentage fraction of total flows.

We’ve had to adapt the processes and structures to be adaptable, with backup processes upon backup processes to cater for almost all scenarios we can currently map out.

Will there be more that will surprise us? I am almost certain that it is a yes, but did we build in a mechanism to revise the modular process when we need to? Absolutely. After all…

Change is the only Constant. — Heraclitus