If SoftBank made me the CEO of WeWork for a day… 🦄

A valuation of $47 Billion USD at its peak. Thanks to SoftBank.

Is SoftBank crazy enough? Yes.

As crazy as that it would make me the CEO for a day? No.

Then why did I get this thought of becoming the CEO out of no where? Cause I was challenged by Tian Shou to it when I was waiting for the espresso machine to fill up my cup. (P.S. the coffee was pretty bad but a millennial who is saving to clear his/her debt off never says no to free coffee)

Fresh off from reading a plethora of WeWork debacle articles, my initial answer to that question was a straight up no. I went like,

No, I would never be taking up that role and it’s a sinking ship that cannot be saved.

And I walk off with that pretty bad cup of coffee I mentioned about earlier.

While I shrugged the question off and left it where I was asked, it did never leave me and followed me everywhere for the next couple of days.

So I started to think about it…..

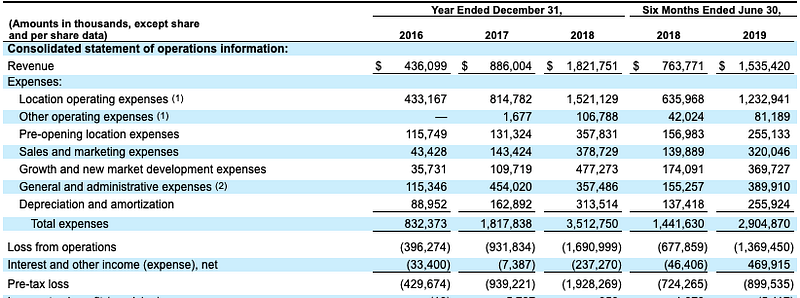

Where did WeWork’s biggest losses come from?

$1.4 Billion USD loss from operations might seem to be arguably fine compared to other companies in SoftBank’s portfolio. Uber. 🚕

But upon taking a closer look at the financial statement, a whopping 90% of WeWork’s Expenses come from what’s mentioned as “Location operating expenses.” Of which, close to 28% is accounted for location operating costs and the rest 62% is accounted as lease costs which amounts up to a staggering $800 Million USD. 🤑

And as per their SEC S-1 filing, here is what exactly WeWork means when it talks about the above mentioned lease costs in its financial statements.

We enter into leases with landlords that have an average initial term of approximately 15 years. These leases typically provide for a specified annual base rent, with annual escalations later in the term of the lease, as well as a reimbursement by us for costs such as common area maintenance charges and real estate taxes (collectively “lease costs”).

TLDR; WeWork’s business model is to lease out spaces for a long period of time and then offer it out to its members on a per seat basis i.e. a “space-as-a-service” offering as they call themselves.

And how do the forecast for “lease costs” related expenses in FY20 look like…? 📈

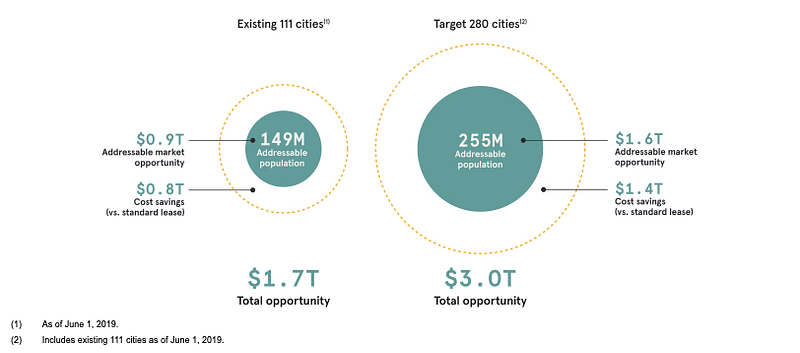

WeWork right now operates in 528 locations across 111 cities and has been incurring a lease cost of $800 Million USD (approx.) for the first 6 months, which comes down to a cool $3 Million USD per location per year.

And just like how every other unicorn startup wishes to grow on steroids (noun; a pile of burning cash), WeWork had its own plans of growth too.

As seen in the above infographic, WeWork planned on scaling to 280 cities (inclusive of the existing 111 cities) which roughly translates to an additional 845 locations based on its historic trend.

Basic math, this means WeWork would have been operating in 1,373 locations across 280 cities had the IPO not been stalled. And just the “lease costs” related expenses would now be sitting pretty at $4 Billion USD.

What about the revenue then…?💰

Based on the historical data as per its SEC filing, for every new location opened, WeWork has been successful in enrolling an average of 1000 members to its “space-as-a-service” offering.

Running the numbers again, 845 locations*1000 members*$250 USD/month*12 months = $2.5 Billion USD

Profitability still seems to be a mirage. And the business model is likely to be unsuccessful no matter whether the growth is 10X or 100X.

So getting back to the purpose of this whole write-up;

What would I do if SoftBank made the CEO…? 🙋♂️

- Brainstorm on where the value proposition comes from.

Value proposition to my understanding is something inimitable by anyone in the business except by the firm which set out to provide it. And upon taking a closer look, WeWork’s strongest value propositions lies across two areas;

a) Tangible value proposition i.e. Technology to run a “space-as-a-service” business

Be it for providing access to shared workstations for teams or private spaces for freelancers/individuals as needed, WeWork has perfected it by the minute, by the hour or by the day across any location in the world with the help of its technology offerings.

b) Intangible value proposition i.e. The brand and the value added services that come along

One needs no introduction about how aesthetically WeWork locations are crafted across the world, and just like how Apple perfected the art of creating a perfect retail store, WeWork I believe has nailed the art of creating perfect workspaces both in terms of features and benefits. It’s the treasure chest of tacit knowledge gained from running global co-working spaces over a span of 9 years that WeWork sits on, if put into explicit use would result in further business advantages.

2. Ditch the current business model for a much leaner one.

I’m a firm believer of the ideology that McDonald’s is a fast food company at its heart but more importantly is a real estate company when it comes to business.

And applying that ideology to WeWork means that it should position itself as a technology company that enables space-as-a-service offerings rather than that of a real estate business as mentioned in its SEC filing.

While the value proposition identified above solidifies the positioning of WeWork as a technology company, what it means for its fundamental business model is to move away from leasing spaces upfront for 15 years and shift towards enabling spaces to be consumed on a pay-as-you-go model by licensing its brand and providing the technology to do so.

Which is a saving of $2.53 Billion USD from avoiding the so called “lease costs” and a reduced operating expenditure by at least 50%

Going back to the WeWork’s proposed plans of adding in 169 new cities over the next few months, how it would work out is WeWork opening up expression of interest from space owners to host new co-working spaces under its brand. Based on the responses and due-diligence, the selected spaces would be branded as WeWork and a consulting fee would be charged to the space owners for doing so. Finally, the technology needed to run the space also would be provided by WeWork and annual royalty could be charged to the space owner or a percentage cut can be taken per seat occupied depending upon the bargaining power of the supplier.

And what happens to the quality?

Quality in the community can also be monitored by setting a stringent set of guidelines that the space owners should adhere to, violating of which might lead to termination of their license.

Would the space owners buy into this new business model? 🤝

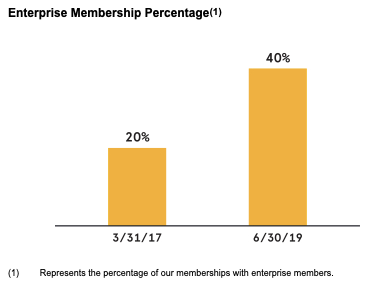

I firmly believe that the space owners would buy into this new business model as WeWork’s memberships numbers suggest that more and more enterprises are adopting to the idea of a flexible and remote co-working spaces. More than 40% of WeWork’s members are enterprise clients and that number is believed to grow by further in the coming days.

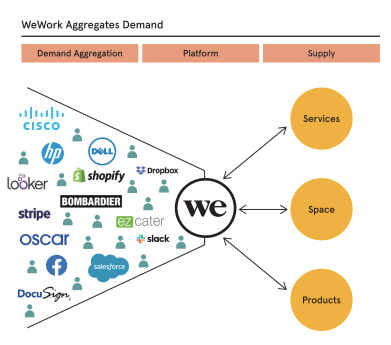

While the above stats prove that WeWork has been increasingly appealing to enterprises, it also sheds a clear light on the fact that WeWork’s efforts to generate and channel demand from enterprises has been paying off and the only challenge at the moment is to prove their ability to retain them.

With that said, channeling the demand like WeWork is an impossible task for the space owners to do by themselves and it’s also clear that enterprises are moving away from the traditional methods of renting out buildings/floors to meet their staffing needs. So it’s either WeWork or retailers for their spaces, but oh wait, I bet they’ve heard of ecommerce before approaching retailers to take up their spaces. 😬

Conclusion ✍️

Yes, WeWork’s valuation was a inflated by a lot as it was a business with a huge addressable market and achieved product/market fit early on, but its underlying business model went uncorrected for 9 years now and no one including SoftBank tried to correct the course of it which I believe ultimately led to a debacle when the wall street had a look at its SEC filing for an IPO.

Maybe a new business model would revive it or maybe it won’t, but there definitely is a need for WeWork 2.0

Update 🔔

Here’s SoftBank Group’s latest take on getting WeWork to profitability. Via. CNBC

Ironic how they talk about reducing operating expenditure (OPEX), but not exactly mentioning the measures about how will they do so. 😅

https://www.cnbc.com/2019/11/07/softbank-plan-to-save-wework-detailed-in-bizarre-charts.html