I Think I’m Taking The Comfortable And Easy Path To Home Ownership

You tell me, but this alternative feels like my best option

I have always believed that home ownership only makes sense if it makes you better off financially today and for the duration than you were yesterday.

And if it fits with your lifestyle. Particularly where you like to live and how and how much you want to work. In other words, unlike so many friends and acquaintances over the years, there was no way in hell I was going to give up city living or some shit just to become a homeowner. There was also no way I was going to do a job I don’t like or work long ass hours just to become a homeowner.

I’m not too proud to admit that if I didn’t think this way, I probably could have bought a house 20 or 25 years ago. I’d at least be on the verge of paying it off completely. And I’d go into relative old age the way I know I need and want to go into relative old age — with a relatively low overall housing expense.

However, I wasn’t willing to make the personal, professional and overall lifestyle sacrifices. Fast forward to days after my 48th birthday and I’m still not willing to make those sacrifices. Especially not now.

Renting for the 28-plus years I have been out on my own has helped give me a life — over the course of those 28-plus years — I know I absolutely could not have had if I chose to become a homeowner. Many homeowners must wait to really live. This was never, is not, and will never be for me.

Which leads to the present day…

As I explained in a recent Medium article about people paying $7,000 a month for housing —

- I can’t afford to buy a home where I live now in Los Angeles.

- Even with rent control, our rent — one way or the other — will become too expensive for our lifestyle really soon.

- I don’t want to live here anyway during the second half of my life.

- My partner and I plan to move to Spain and buy a small apartment there within the next couple of years.

Spain — particularly Valencia — offers the type of lifestyle we want at a price we can afford.

I ran the numbers recently in a newsletter post about putting down roots. In the shell of a nut — if we save our pennies over the next couple of years, we can buy a nice, but modest apartment in the type of neighborhood we love for around 200,000–300,000 euros. A rough sketch of the numbers shows we’ll keep our mortgage payment under 1,000 euros.

To get there, we will have to sacrifice a bit. Like by going out to eat and drink in restaurants and bars much less. But this hardly stings given the how dissatisfied we’ve been with the experience lately.

When we get there, the plan is for my partner to do different work than she does now. Something she’s excited about. And for me to keep doing what I’m doing with an eye on scaling things back a bit within a few years or so. We’ll have more money left over to spend as we see fit, travel and pay down our mortgage more quickly thanks, largely, to what we’ll save on transportation, healthcare, hospitality, grocery shopping and other aspects of day-to-day life in Spain.

This approach feels backwards. Probably because it is.

However, I wonder why more people don’t do it.

In America, we tend to — and we’re taught to — graduate to home ownership as fast as our income will allow. For many people, this requires considerable sacrifice. You can put your own color around the personal, professional and overall lifestyle sacrifices I referenced earlier.

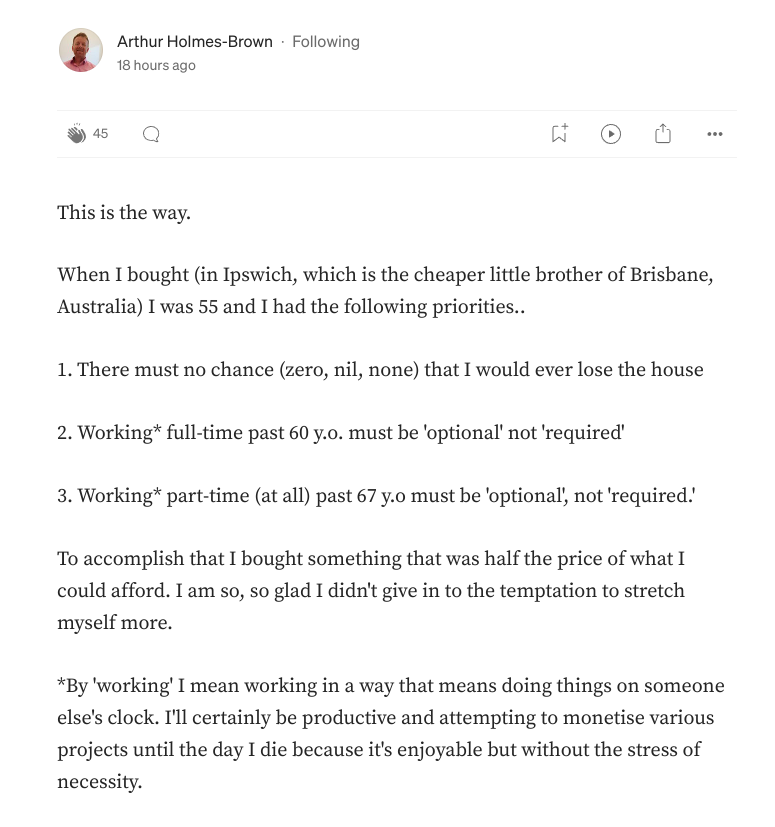

Arthur Holmes-Brown, who is from Australia, made a comment to one of my recent articles that resonated big time. It also inspired and made me feel like we’re on the right track —

I love that so much.

Around the same time I read Arthur’s response, I saw an Insider article about a couple who made the choice to buy a house using only one spouse’s salary. These people are very different than I am. However, specifics of our situations aside, the similarities lie in the idea of only taking the plunge into home ownership if — yes — it makes you better off financially today and for the duration than you were yesterday.

This isn’t a great sales pitch for lenders and Realtors who, for example, irresponsibly encourage people to commit to 7% interest rates today because they can refinance when rates come down. They’d rather you bite off as much, if not more than you can chew.

The path my partner and I are on — which looks and feels awfully similar to Arthur’s — isn’t part of Home Depot’s business model or any of the other entities who benefit from home ownership dominating people’s lives somewhere between 25 and 65.

So, yeah, I think we’re on the comfortable and (relatively) easy path to home ownership. Home ownership that will — as we see and envision it — put us in the best personal, professional and lifestyle positions possible as we approach and enter the second act of our lives.

To receive a notification each time I publish a Medium article, go here. In future articles, we’ll go more in-depth on the things I touched on today.

To subscribe to my Never Retire: Living The Semi-Retired Life newsletter where we get even more personal, go here.

This article is for informational purposes only. It should not be considered Financial or Legal Advice. Not all information will be accurate. Consult a financial professional before making any major financial decisions.