I Can’t Believe I Have to Say This But Stop Burning Your Life Savings

The long-term impact of reckless investing and how it may have cost one investor $768,000.

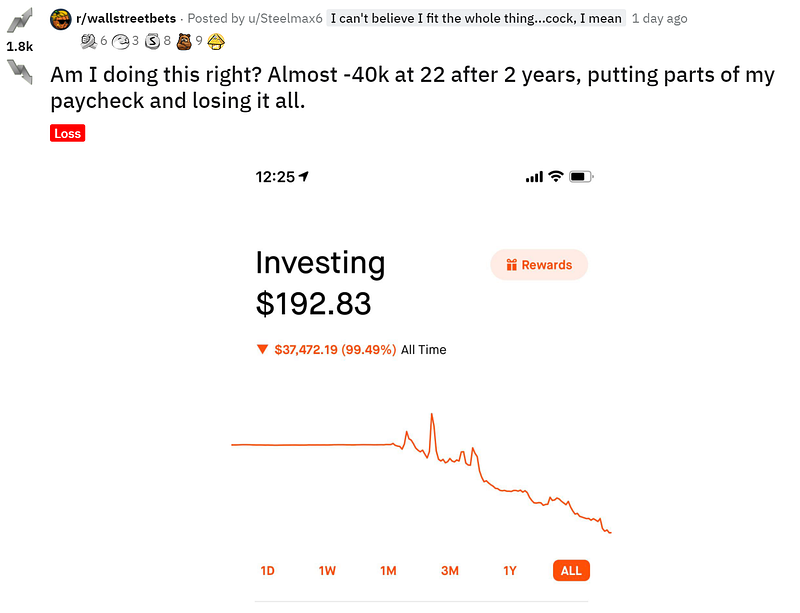

30 years old. Life savings gone. Since April of 2020, I’ve finally amassed a 6 figure loss. Looks like I’ll be eating ramen until retirement.

This is the verbatim text from a thread on Reddit, specifically the infamous WallStreetBets community.

Redditors keep outdoing themselves. Each day, investors flock to this social media community to share their wins and losses. The stories of reckless investing decisions are baffling (and seemingly endless).

One user’s portfolio is having a helluva year — in the worst way possible.

Stupid financial mistakes aren’t uncommon, especially as a teen or an inexperienced twenty-something-year-old. And, sure, you could make the argument that time is still on the side of a young investor. Assuming Steelmax6 is gainfully employed, he could make up for lost ground.

But that doesn’t mean there aren’t financial consequences. Let’s explore the lasting effects of massive losses due to reckless investing.

The long-term impact of reckless investing

No matter how you spin it, it’s rough to lose a chunk (or all) of your hard-earned savings.

One way or another, Steelmax6 managed to already have $40,000 of savings by the time he could legally drink. He also managed to burn through 99% of his savings over the last year, leaving him with just shy of $200.

From the looks of it, Steelmax6 had all of his savings in cash until about a year ago, at which point he moved into options trading. (I’m guessing he did so without doing any research whatsoever.)

Makes you wonder — what if he took the exact opposite approach to investing and developed a conservative portfolio of stocks and bonds? Let’s play the what-if game.

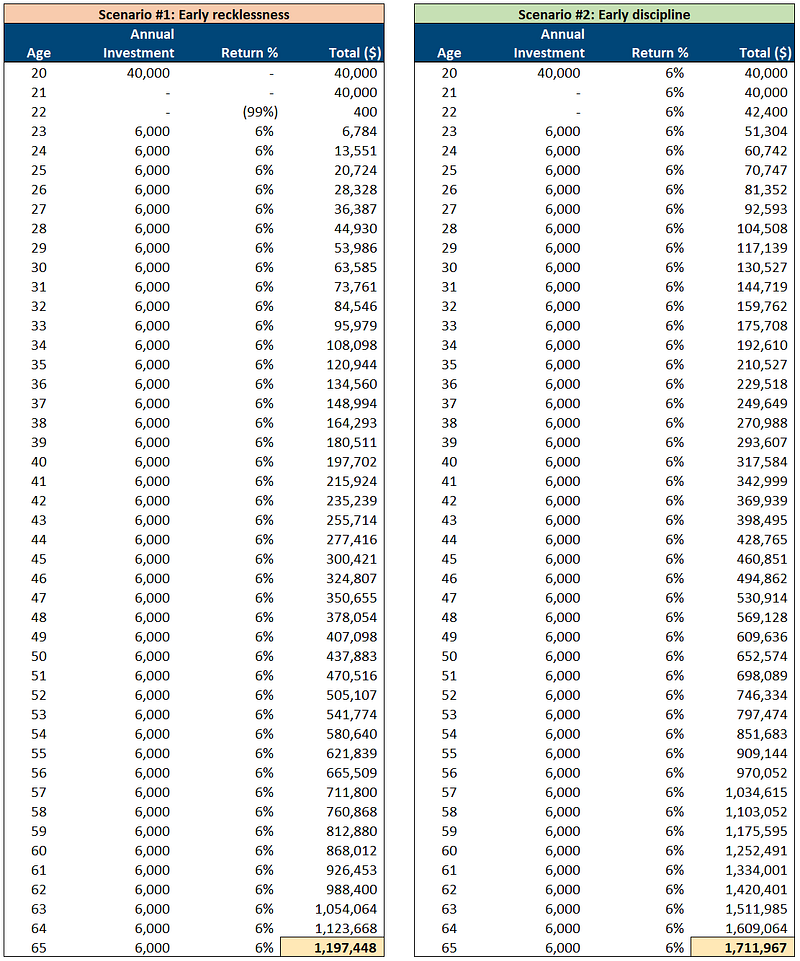

In both of the following scenarios, Steelmax6 gets his act together and adopts a conservative investment strategy. Let’s assume he invests $6,000 each year until he retires at age 65 and maintains a steady 6% annual return.

However, the difference is timing — scenario #1 assumes he commences this conservative approach after losing everything at the age of 22. Scenario #2 assumes he took this approach from the moment is started saving at age 20.

Under these conditions, that early investing mistake didn’t cost him $40,000 — it cost him over $500,000.

While financial needs are subjective (who knows how much Steelmax6 will need during retirement), $500,000 is a significant lifestyle difference. But, this somewhat reinforces the idea that we can make up for lost ground if we make dumb mistakes when we’re young.

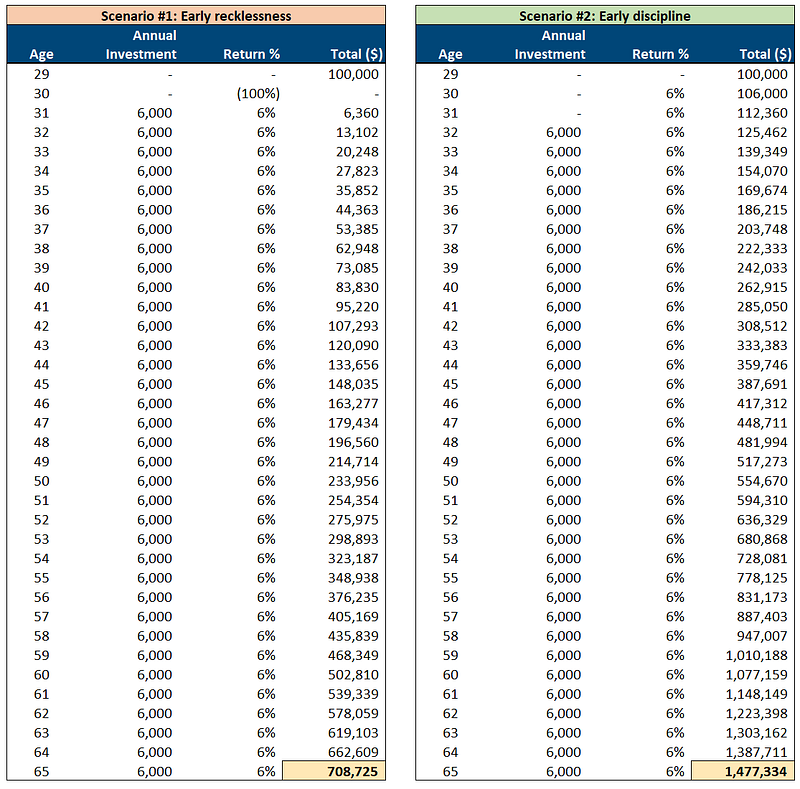

What if we’re a little older? Another user, Abject_Resolution, proclaimed that they finally amassed a six-figured loss at the pivotal age of 30. Remaining life savings? Zero.

Eight years might not seem like much — 22 and 30 are both young ages, relatively speaking. However, it carries much greater weight in the world of compound interest.

Let’s run our scenarios based on Abject_Resolution’s financial situation.

In this case, poor financial decisions shaved this Redditor’s future wealth in half.

This much is clear: the older you are, the less time you have to make up for catastrophic investment losses.

Although the above tables accentuate the impact on retirement, I want to shed light on another point in time too. Buying a house is a common life event — and it usually takes place sometime between your late 20s and 30s. Now, imagine if Abject_Resoltuon needed to put a down payment on a house at 32? They’d be pretty strapped for cash.

The money disparity is alarming — but what does it really translate to?

Financial stress and instability. Cutbacks in other areas of life. Missed goals and opportunities.

Why does this keep happening? What differentiates a good investor from a speculative gambler (or even a naive investor)? Let’s try to answer these questions before I walk through more logical alternatives.

Why investors continue to suck at investing

Investing can massively benefit financial stability and accelerate wealth generation. If there was an unexpected silver lining to the pandemic, it was that many people started to recognize the importance of investing. Hordes of investors flooded the stock market — many of which had minimal experience with investing.

Unfortunately, the typical investor sucks at investing.

I’m not saying everyone sucks. I’m not saying you suck.

I am saying that if you plucked a random person out of a crowd, there’s a good chance they don’t know much about investing or personal finance in general. (Considering you’re here, there’s a better chance you know what you’re doing compared to the average investor.)

But why do people suck at investing? A few reasons.

The learn-as-you-go paradox

Education systems rarely mandate Investing 101 courses, so the typical person is responsible for figuring it out on their own. In turn, we have two options:

- Patiently learn and wait to invest until we’ve developed a better understanding

- Invest and employ the learn-as-you-go approach

If I had to guess, most people choose the latter. It’s not a stretch to say that most new investors will make mistakes along the way. Returns will reflect those mistakes.

Unwillingness to perform independent due diligence

“Do your own research.” “Do your own due diligence.”

As an investor, you’ve likely heard this repeatedly. Yet, without fail, people continue to shun the idea of performing their own independent analysis of an investment. It’s much easier to trust other people’s recommendations than to form our own opinions.

But what if a recommendation is a pump-and-dump scheme or just a shoddy idea? Unquestioning trust can lead to trouble.

Ignorance of implicit biases

People are biased. We can’t help it.

And our biases can easily influence our investment decisions. For instance, we like to follow the crowd, which is known as herding. We see people posting about their newfound small fortunes from buying a random crypto or meme stock and we’re inclined to mirror their decisions.

Everyone’s buying dogecoin? I don’t want to miss out.

While some people can profit from momentum swings, others will lose badly.

How to not suck at investing

Obviously, there are dozens of better investing strategies than uneducated options trading and sporadic stock purchases. But here are a few tips for the gamblers out there.

Avoid social media

For starters, stay off of social media if your investing strategy aligns with the aforementioned Redditors. The random social media ‘investing guru’ does not care about our well-being. The wild get-rich-quick investment is more likely an accumulate-losses-quick scam.

They say “don’t watch the news” if you don’t want to get emotionally invested in the market’s volatility. The same goes for social media.

Calculated speculation

It’s okay to take risks — even if that means putting a sizable chunk of change in something you believe in, like crypto or a disruptive tech stock. However, there’s a difference between calculated speculation and wild speculation. The latter could jeopardize your financial stability for years to come.

Before you dabble with options or trust cryptos wholeheartedly, consider limiting your speculative bets to 5–15% of your total investable assets. Keep in mind, this excludes things like your emergency fund or general checking account for daily expenses.

Whatever amount you choose, be comfortable with losing it.

Long-term index investing

There’s nothing wrong with taking a passive approach to investing (such as index investing) while you learn about stocks, crypto, real estate, or whatever. For instance, you could compile a simple portfolio of index ETFs that mirror certain industries, asset types, or the broader market.

That way you aren’t missing out and you decrease the chances of easy mistakes.

If you want to understand what makes a “good” investment, sign up for the Due Diligence newsletter.