How to raise money before launch

An analogy we use at KV is that building a company is like laying cement. Early on the cement is liquid and malleable – you can stir it around with your hands. As time passes, the cement hardens. Once it solidifies, adjustments require a jackhammer. And jackhammering leads to cracks and lots of noise.

As a result, we prefer to get involved as early as possible in a company so we can help founders lay the foundation correctly. In fact, our favorite checks to write are $1–3M checks where we provide the first institutional capital in the company. But since we get involved so early, there aren’t many metrics or traction to help us build conviction. In fact, many of the companies have not even launched a product yet. For example we’ve funded all of these before launch (Opendoor, Forward Health, IndigoFair, Go Insurance, Ever. AI).

In order to build conviction, we rely on founders to tell us a compelling story, almost always in the form of slides. We’ve funded companies almost entirely because of the quality of their seed decks. Poor deck? We’ll likely pass on the opportunity.

Because seed decks are distinct from later fundraising decks, which often rely on metrics, cohorts, and other empirical evidence of traction, here are the best patterns we’ve seen from some of our favorites. Full links to the decks here (Opendoor, Wanderjaunt, Even)

The one-liner on the first slide

The best companies are founded from a simple-to-understand value proposition. The first slide highlights that value proposition.

Your first slide is your first impression to investors; the one-liner on it should describe the company vision to employees, and the value to potential customers.

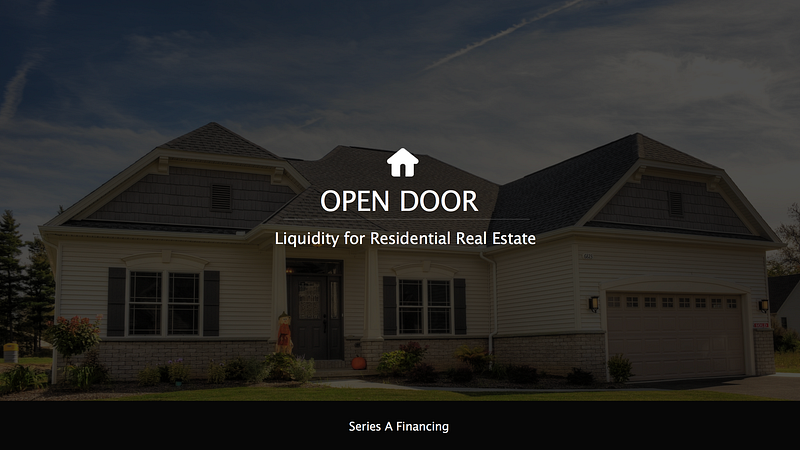

Opendoor was founded off a single value proposition. “Liquidity for Residential Real Estate”

Great decks often provide analogies to help investors understand the business they pitch, e.g. a new twist on a well understood business model. This one got a little clever, and it works:

Each title tells a story

The next step in building your deck is distilling the story you’ll tell into a single paragraph. Each slide in your deck should then dive deep into each particular sentence from that paragraph – the sentence is the title. Below are the titles of each slide in the Opendoor deck:

You can read those headers out loud one after another – it’s essentially an elevator pitch for Opendoor. The goal is to have the investors think QED at the end.

What problem are you solving? What about the current state of the world sucks?

One powerful technique is to tell a customer persona story. Even introduced a single mom who works at Starbucks, Amy. Amy’s landlord calls her one day and says he will no longer accept late rent payments, and wants this month’s rent by tomorrow or he is evicting her:

Amy takes out a payday loan to cover this sudden expense, but the fees and high interest of the loan spiral her into poverty.

Even’s team ends the story with a powerful single slide:

The problem is clear, the current world sucks, and it makes a reader want to drive change.

How is your state of the world better?

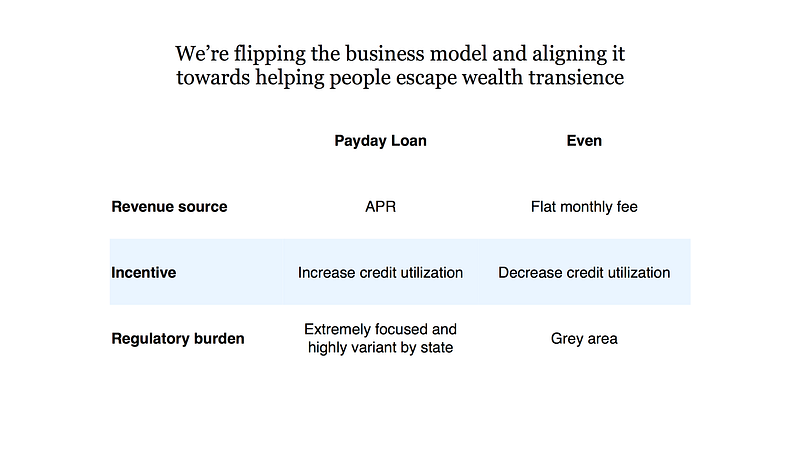

Even’s deck continues with the story, and shows how the world is better with it around: Even is the friend who can spot Amy, as opposed to the predatory sharks like payday lenders.

Even better if your business model explains why; rather than being incentivized to increase credit utilization, Even is incentivized to decrease it. Even will also cut out most of the costs of running a lending business (e.g. the brick and mortar retail locations).

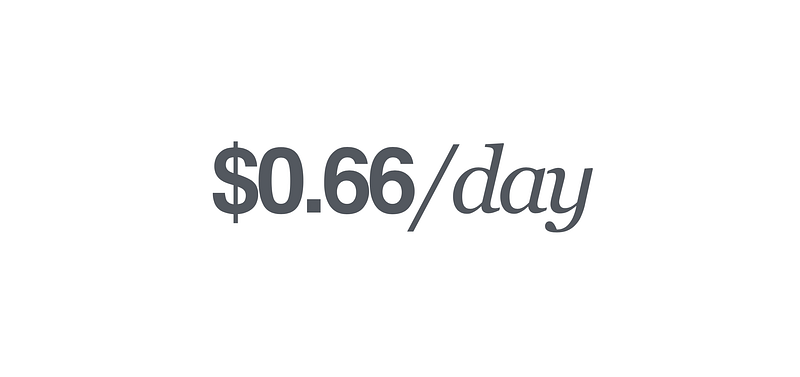

Where’s the money?

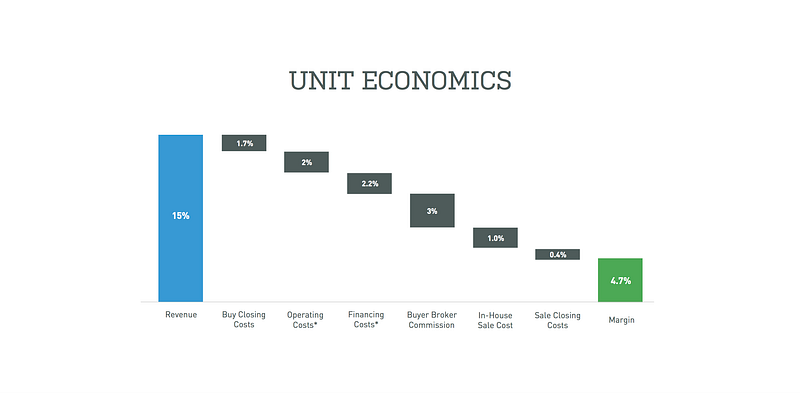

The next section should explain who you expect to buy for what. These can be as complex as your projected unit economics:

Or as simple as a headline price for a subscription:

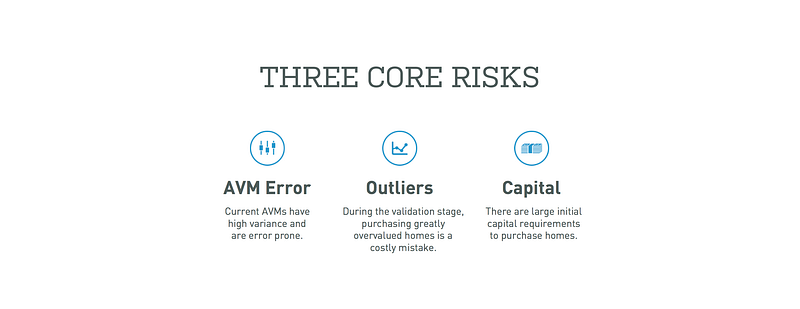

What are the risks? What needs to happen for your state of the world to exist?

Between now and you becoming a billion dollar company, what needs to be true? These things can be simple, like “can we scale our customer acquisition while keeping our payback period reasonable”. Or complicated, like “the laws of physics may not permit our technology to be viable”. Opendoor’s were valuation error, outliers, and capital:

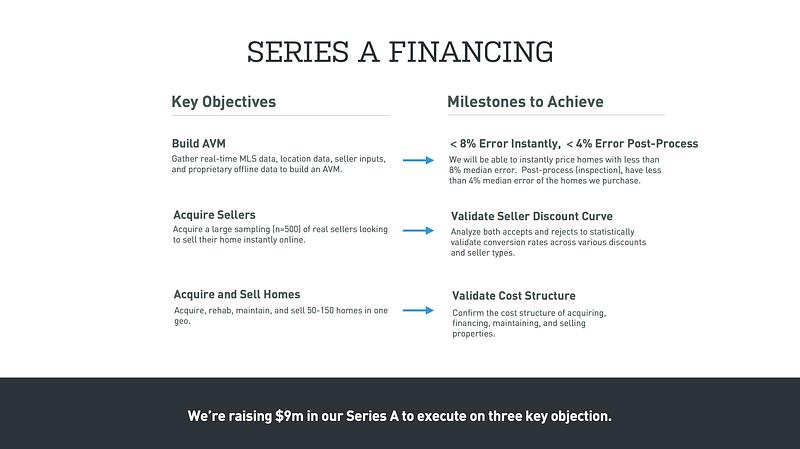

How much money do you need to remove what risks in what timeframe?

A common metaphor used in VC is investing is like playing poker. At the beginning, we only have a single card in our hand. It might be an Ace; the next four cards could be terrible, or they could be a royal flush.

In order to get the next card and find out, you have to invest more capital. At the beginning of the hand, the possibilities are endless. As you get closer to 5 cards, the possibilities become more limited.

You want to show how the first money in will let you draw a good card. Or better yet, two good cards!

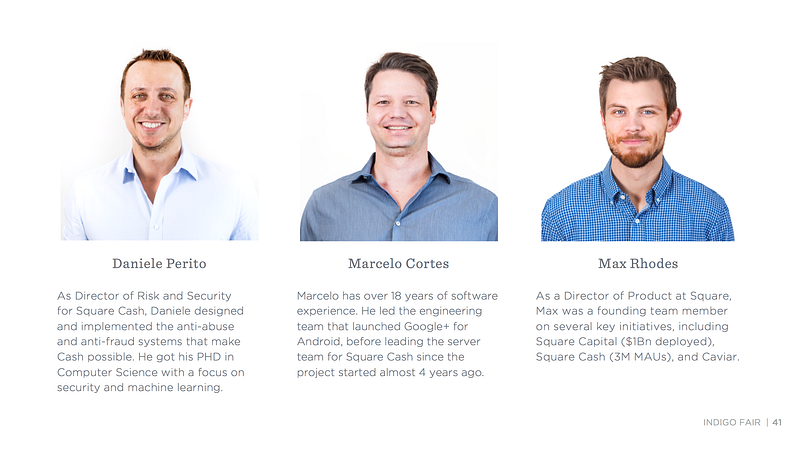

Why are you the team that can do this?

The best thing you can do is explain why you are the team best suited to tackling this problem, over anyone else in the world. Startups are really fucking hard, why do you have an unfair advantage?

The worst thing you can do is give us a bunch of photos, names, logos, and university emblems. This is complete fluff and tells me nothing about why you’re more likely than others to solve a specific, hard problem.

One of my favorite team slides is from IndigoFair:

When you see this slide, you immediately grok that these guys have an unfair advantage serving SMBs.

If you’ve followed this guide then please send us your seed deck, we’d love to chat. Email me at [email protected]