How to Manage Your Money using the 50/30/20 Rule

Quite possibly the most beginner-friendly budget

Introduction

I previously wrote an article on debt repayment methods. We discussed the advantages and disadvantages of the debt snowball and the debt avalanche.

Though many of us agreed that the debt snowball works best for most people, there were those of you who voiced your support for the debt avalanche. The discussion was truly enriching!

One of the comments really got me thinking. There was a comment from a guy we’ll call Austin. Austin mentioned that he has spending issues and experiences difficulty sticking to a budget.

I’d like to thank Austin for his honesty and bravery in mentioning that. I prefer to think of Smart Money viewers as a community. If one of us in the Smart Money community has a personal finance problem, then it’s likely that others might also.

It seems like Austin hasn’t found a budget that he can stick to. So I set out to find a beginner-friendly budget that might work best for Austin and anyone else having trouble sticking to a budget.

The 50/30/20 Rule

That’s where the 50/30/20 rule might be useful. The 50/30/20 rule, also known as the 50/30/20 budget, is a term coined by Senator and former presidential candidate Elizabeth Warren in her book “All Your Worth: The Ultimate Lifetime Money Plan”.

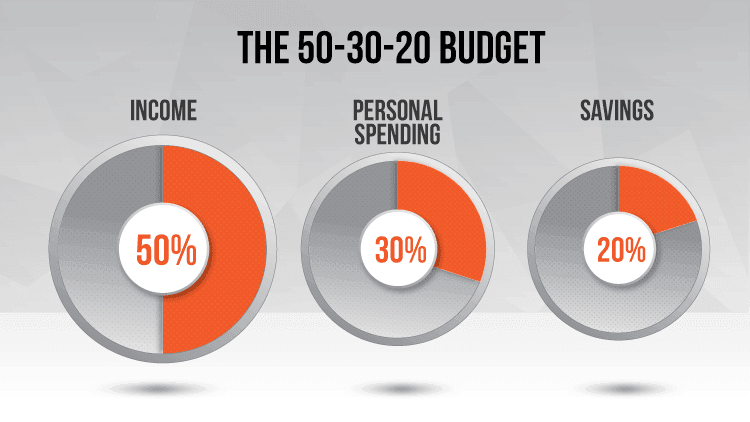

The rule is very simple. You break down your take-home, or net income into three categories: Needs, Wants, and Savings/Debt Repayment. Each of those categories should account for a certain percentage of your earnings.

Needs should account for no more than 50% of your earnings. A need is an expenditure that you can’t avoid. These include basic utilities, child care, groceries, housing, insurance, and transportation.

Now, what about things that make life worth living? Things like cell phone service, dining out, internet service, and gym memberships?! The 50/30/20 rule would categorize these things as wants. Many people might define wants as extras that make your life easier, but aren’t needed to live. The plan calls for you to allot 30% of your spending on your wants. These would also include entertainment, monthly subscriptions, and travel.

Lastly, the plan requires that the other 20% of your net income be devoted to your savings and debt repayment. This would include activities like building an emergency fund, funding a retirement plan, and paying all debts you might owe.

Problems with the 50/30/20 Rule

The 50/30/20 rule is a very good budget for those of us getting started in personal finance. Its beauty is in its simplicity. However, it does have some problems that should be addressed.

Broad Spending on Wants

The 50/30/20 rule allows for broad spending on one’s wants. This can make it easy for the less disciplined among us to spend at or beyond our means. Other budget plans tend to call for a tightening of the purse strings. However, the 50/30/20 budget provides the opportunity for clever categorization of miscellaneous spending as “wants”.

For example, theStreet.com cites a report from the Bureau of Labor and Statistics stating that the median income in the United States in 2019 was $48,672. If this is true, that would mean the median monthly income is $4056/month.

For the sake of this exercise, let’s assume this is all net income. This would mean that the plan allows for $1216 to be spent on a person’s wants every month. In my opinion, this money could be better spent on wealth creation.

Insufficient Spending on Debt Repayment

That brings me to my next point. The 50/30/20 rule as prescribed doesn’t have much of a focus on debt repayment. This may work out well for those of us who have no debts outside of our mortgages. However, Experian.com suggests that the average American has a debt of $78,459, not including mortgages ($203,296) or Home Equity Line of Credit ($45,191), or HELOC.

Keeping with our previous example, if the median income in the United States is $4056/month, the 50/30/20 rule would only allow for $811 to be spent on debt repayment. This means, barring interest, this hypothetical American would take 97 months to pay his/her $78,459 of debt.

Improvements to the Rule

As I said previously, the 50/30/20 rule is a good beginner-friendly budget. I think it could be a great long term if there was a key tweak made to how one’s income is to be assigned.

I would suggest keeping spending on one’s needs at no more than 50% of net income. This is a solid rule that doesn’t require much tweaking if any.

I would switch the percentage of the budget allocated to wants and savings and debt repayment. In my opinion, it would be more financially responsible to spend 30% of one’s income on savings and debt repayment, and 20% on wants. I believe it’s this kind of financial belt-tightening that makes having a budget admirable.

Conclusion

The 50/30/20 rule is a very good beginner-friendly budget. It allows a person who finds it difficult to stick to a budget to manage their money successfully. The budget allocates 50% of one’s earnings to their essentials, 30% to their wants, and 20% to their savings and debt repayment.

The rule works well but can use some adjusting. One adjustment I’d make is to switch the percentages for wants and savings and debt. It’s better to spend more of your money on wealth building than on fun and entertainment.

I create media geared towards people who are new to personal finance. Sound like you? Sign up for my newsletter and be the first to know when I create new content on personal finance, investing, economics, and other money-related topics!