How I Keep a Budget — Tracking Expenses vs Planning Ahead

Budgeting is fun, exciting, stress-relieving, and generally leaves me feeling warm and fuzzy all over, or that may be the cat.

I have always been a budgeter. Starting in my early 20s with pencil and paper, the system I use has evolved including graph paper, a budgeting notebook, Excel spreadsheets, a zero-based budgeting system on paper, and finally landing at YNAB (You Need A Budget) subscription service. Yes, I am paying a subscription fee for access to budgeting software. And yes. I find that annual expense annoying. But it works brilliantly for my partner. So there ya go.

The benefits of keeping a budget (feeling financially secure, minimal fighting with spouse over unexpected spending) far outweigh the time spent setting it all up and the weekly maintenance. And even the annual subscription fee. I do have to admit that YNAB is very convenient across the desktop computer and both phones. There is really no excuse for overspending a category.

What Is the Best Budgeting Tool to Use?

The best tool to use, hands down is . . . the one that works bests for you. Sorry, but you’re not getting out of it that easy.

All the tools I have used have worked equally well in different ways, with pros and cons for each. Part of the reason I have used so many different tools is simply that the evolution of technology has allowed me to. A spreadsheet is a spreadsheet whether it is pencil and paper or on a computer. Putting my paper budgeting spreadsheet into Excel was an easy and obvious jump to make because the computer would do the math for me, which made updating go faster. It streamlined the process.

Jumping from my perfectly good and free spreadsheets to the paid subscription for YNAB was much harder for me. YNAB actually doesn’t do anything I wasn’t already doing in my spreadsheets. YNAB just does it prettier and more convenient. My partner weighs heavily into this choice. He respects the boundaries of YNAB better than he did the spreadsheets, our impulsive spending has gone down, and our savings (preparing for future expenses) has gone up. We both win and the cost is within our means.

Try a few different tools, make notes of the pros and cons of each, and choose what you like best.

Best Budgeting Style

Forecasting

I started out using a forecasting system which meant at the end of each month, I would look back at the expenses of that month and layout a plan of what I expected my income and expenses for the next month to be. In my spreadsheet there was a budgeted column where I would record those forecasts and next to it was the actual column where I recorded what I had actually spent. The third column, labeled over/under, recorded how much my spending was over or under the budgeted amount.

It was a simple system and did exactly what was expected: track my spending. What it didn’t do was help me plan for future expenses. If I remember correctly, I set up all my bills to be paid monthly and the electric company put me on their budget system so I paid the same amount all year round. I paid ahead during summer to cover the higher bills in winter.

Zero-based or Allocating

In a zero-based budget, I record my income as it comes in each week and allocate it to the line items for future spending. The line items are sorted into categories of regular expenses: food, phone, internet, rent, etc; occasional regular expenses: electricity, water, car registration, birthdays, etc; and occasional irregular expenses: car repairs, homeschooling excursions, clothing, public trans, etc.

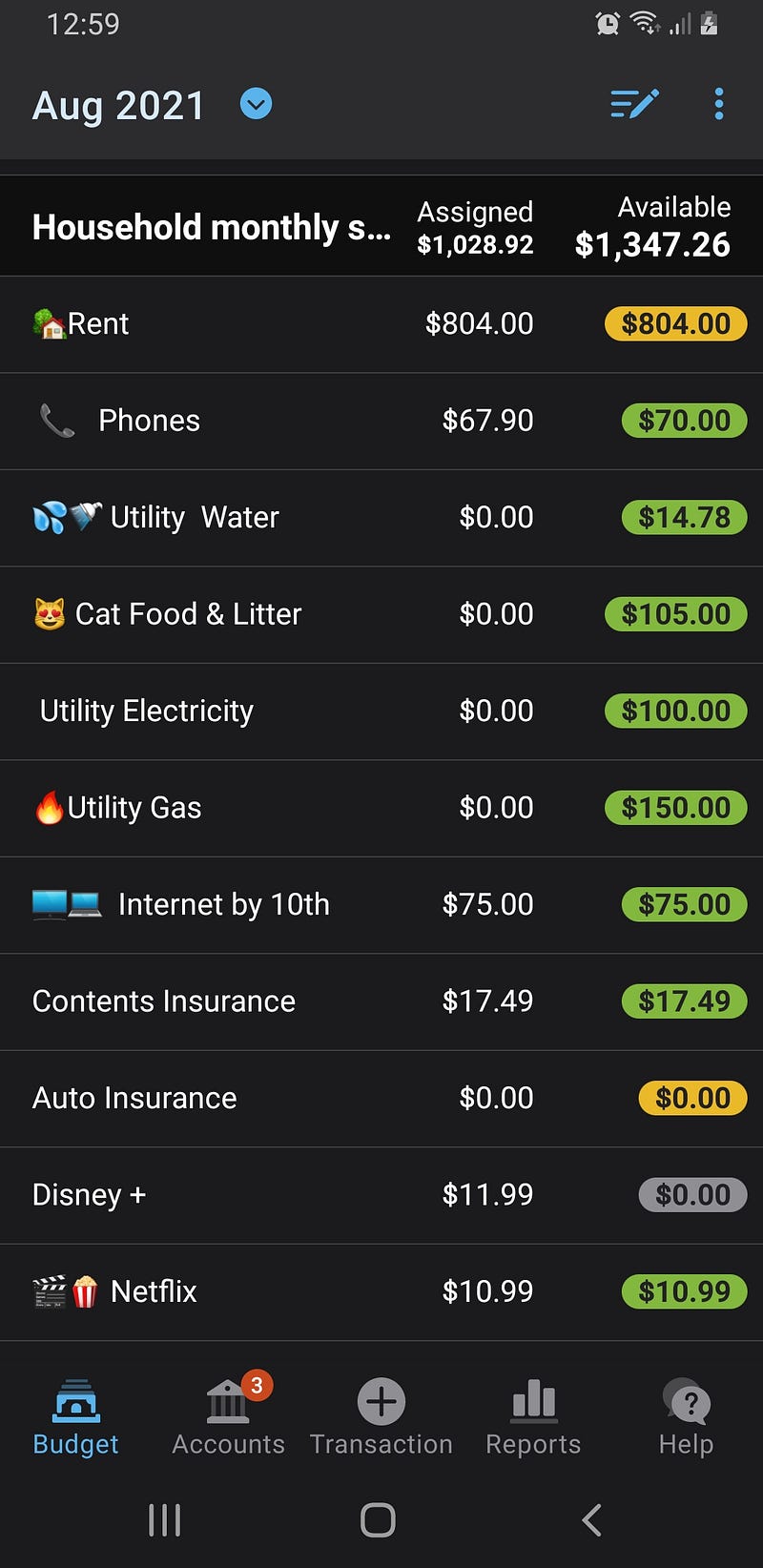

Then I record the spending as it happens. It looks like this:

Category names are on the left. The assigned column shows how much money I have allocated for that category this month. The available column shows how much of the allocated amount is available for spending.

They don’t always match such as in the Phones category where available is more than assigned. This is because there was money carried over from last month when the bill came in lower than expected. Electricity doesn’t match because it is a bucket category. I fill the bucket with the same amount each month, but the bill only comes every other month.

The occasional irregular expenses could be lumped together and called emergency expenses, but considering I know they will happen at some point in time, they aren’t unexpected expenses; therefore I can plan for them. The timing is unexpected, but that is just an inconvenience, not an emergency. An emergency is when there is suddenly no income at all.

All of the occasional, regular and irregular, expenses are what I call my buckets of money. The money all sits in the bank until it is needed for spending. It is there when needed and that is what I call financial security. Knowing I can cover those expenses when they happen, expectedly or unexpectedly.

Conclusion

I keep a budget because it feels good to me, warm and fuzzy even. Knowing the money is in the account to cover all of my regular expenses for at least the next month is comforting to me. Not having financial security is the highest cause of stress in adults, second only to divorce.

Keeping a zero-based, allocation budget reinforces good and mindful spending habits. It keeps me and my partner on track for our goals, both individually and together. And when life doesn’t stick to the plan, which is most of the time, it also allows me to make adjustments as needed. There is room in the budget to move money between certain categories as needed. That feeling of financial security is always there.

I’m not willing to give up the warm and fuzzy feeling that financial security gives me and that is my motivation for keeping the budget up to date and pay the annual subscription fee. I love the buckets of money sitting there waiting for the next bill to arrive or the next sale on the homeschooling curriculum. When the money is already allocated to be spent, life is simple.

How do you plan and track your spending? Let’s talk about it in the comments below.

Another article by me:

Affiliate Links*

YNAB offers the first 34 days of use for free. When you subscribe using this link, you get an additional free month and I get a free month.

*When you subscribe or become a member through an affiliate link, I make a small commission, but this does not increase the price. Thank you.

Originally published at https://letstalkabout.com.au on August 16, 2021.