How to Figure out How Much You Need to Save for Retirement

A guide for DIY retirement planning

One of the most critical questions in personal finance is “how much money do I need to save for retirement?” Being able to confidently answer that question and put a plan in place to follow through on your savings goal is one of the most critical problems you need to solve in your financial life.

The problem is that many people don’t have a retirement plan. They know they should, but they don’t. There are two straightforward reasons for that disconnect between the importance of the issue and the lack of follow-through.

- Figuring out how much to save for retirement feels too complicated.

- The consequences for failing to act won’t be felt for decades down the line.

When the human brain is met with a complex issue that it does not have to deal with for a long time, the natural inclination is to deal with it, later on, focus on more pressing issues of the day.

Even if you don’t feel the consequences for many years, you need to treat retirement savings as a priority that needs to get solved today. This article serves as a guide for DIY retirement planning. It’s important to note that any DIY retirement plan will have a trade-off between simplicity and customization.

- A very simple DIY retirement plan will be simple but very general and not based on the specifics of your life.

- A DIY retirement plan that is tailored to your life will be very complex and involve a lot of work.

If you can afford to pay for a professional financial plan, that is a great way to get a customized retirement plan that is explained to you. If you want a simple, generic ballpark figure, there are plenty of free online retirement savings calculators you can play around with.

For those who want to learn how to create a DIY retirement savings plan tailored to your life, continue reading.

How to figure out how much you need to save for retirement

Figuring out how much you should be saving for retirement is a four-step process.

Step 1: Decide how much income you will need in retirement.

Step 2: Determine how much money you need to have saved on the day you retire to generate your retirement income.

Step 3: Calculate how much you need to start saving right now.

Step 4: Ensure your success by automating your savings.

What happens if you don’t save for retirement?

If you have nothing saved by the time you reach retirement age, one of two scenarios will play out.

- You work until you die.

- You become dependent upon your children or the government to take care of you.

When working until you die is the best-case scenario, you know you are dealing with some terrible options.

I’ve heard some people say that they wouldn’t mind working forever. They love their job and don’t see themselves ever retiring, so saving is not a priority.

Here is the problem with that kind of thinking. It’s easy to say you don’t mind working forever when you are young and healthy. I am 32 years old, and I love what I do. I would keep doing it forever if I could remain a healthy 31-year-old forever. But I can’t. One day I’ll get old, and my health will begin to fail. Working may be a lot less fun when it hurts to get out of bed in the morning. I have to be realistic and come to terms with the fact that there may come a day where I don’t want to do any work at all.

When I think of how much my goals and dreams have changed between the age of 22–32, I can’t imagine how much they will change by the time I am 72. It’s not fair for my 32-year-old self to write checks that my 72-year-old self can’t cash.

For the sake of argument, let’s assume that even when I am 72 that I don’t mind continuing to work. That decision may not be up to me. The future state of the economy or my health may prevent me from working.

If I’ve reached retirement age with very little savings and am unable to work, what would become of me? I would have to rely on my family and the government to support me. The thought of being that type of burden stresses me out.

That is why it’s crucial to save for retirement. If nothing else, to at least provide yourself the option to retire by a certain age and live financially independent.

Saving for retirement and having more money than you need is a much better outcome than not saving for retirement and not having enough money.

To answer the question of how much you need to save for retirement, you must first answer another question.

How much income do you need in retirement?

Most financial professionals recommend that you aim to replace 70% of your annual pre-retirement income in retirement. If you made $100,000 per year before you retired, your goal would be to have $70,000 per year going forward in retirement.

The technical term for how much of your pre-retirement income you generate in retirement is referred to as a “replacement ratio.”

Replacement ratio= Retirement income ÷ pre-retirement income

Retirement income can come from any combination of your personal savings, workplace and government pensions, and income from rental properties or any other consistent form of income you can depend on during your retirement.

Is 70% of your income really enough to fund your retirement?

The goal of replacing 70% of your pre-retirement income is a rule of thumb. Like all rules of thumb, it is severely limited and does not take any of the specifics of your life into account.

The 70% replacement ratio should be the starting point, not the endpoint when creating a goal for how much income you need in retirement. Depending on which of your living expenses increase and decrease during retirement a 70% of your pre-retirement income may be too much or not enough money to fund your desired lifestyle in retirement.

The critical thing to remember is that your income replacement ratio has a direct effect on how much you need to save for retirement. The more income you want to replace, the more you need to save for retirement.

If you can replace 70% of your income in retirement, you will be in a better position than most people. However, if you want a retirement income customized to your life (who wouldn’t?), you need to think about what you’ll be spending money on in retirement.

What costs will go decrease when I retire?

Many costs typically decrease or go away entirely in retirement. The three most significant expenses that may decrease in retirement are;

- Saving for retirement.

- Childcare costs.

- Housing costs.

Saving for retirement

Once you retire, you no longer need to save for retirement. That might sound obvious to the point of being silly. However, it plays a massive role in how much cash you need each month in retirement.

Ironically, the more you save during your working years, the smaller your income replacement needs to be during retirement. That is because there is an inverse relationship between your saving rate and your income replacement ratio. If you were saving 20% of your income during your working years, that is 20% of your income that does not need to be replaced during retirement.

What percentage of your income you save for retirement is something that you need to factor in when deciding on your retirement income replacement ratio.

This is yet another illustration of how saving early and often makes your life easier.

I should make clear this is referring specifically to your retirement savings. You’ll still need to save and budget for specific purposes like vacations during retirement.

Childcare costs

It’s no secret that having children is expensive. How expensive is it to raise a child these days? The USDA breaks down the annual cost of raising a child as follows.

- Age 0–2: $12,680

- Age 3–5: $12,730

- Age 9+: $13,180

- Age 15–17: $13,900

If you currently have two kids aged 5 and 9, you might be spending around $26,000 per year on child-related expenses. If that seems like a lot, remember these are averages, and that includes all costs of raising a child from childcare to extra groceries, to higher utility bills. All those costs add up quicker than you might think.

The good news? That $26,000 per year that you will not need to spend in retirement. This plays a massive role in your income replacement ratio.

Of course, this assumes your kids are grown up and financially independent from you by the time you retire. If you have grandkids that you want to spoil, you will want to factor that into your retirement budget and the amount of annual income you’ll need.

Mortgage payment

If your mortgage is fully paid off by the time you retire, your housing costs will drop by the amount of your mortgage. You’ll still have to pay for property taxes and maintenance, which both tend to be around 1% of the value of your house per year.

If you retire with no mortgage and a house worth $500,000, you would still need to budget for at least $10,000 per year plus your heating and utility costs.

If you choose to sell your house when you retire, that decision will impact your retirement lifestyle in two ways.

- Adding that lump sum of money to your retirement savings will allow you to increase your expected income in retirement.

- If you choose to rent or take out another mortgage, your housing expenses will increase.

Whether or not selling your home in retirement is a good financial decision will depend on whether the lump sum from selling your home will be large enough to cover any additional housing costs in retirement.

Geographical arbitrage

Geographical arbitrage is when you move from an area with a high cost of living to an area with a low cost of living. This allows you to enjoy the same quality of life you currently enjoy on a smaller income.

If you lived and worked in New York City your whole life and then, in retirement, decided you wanted to live in a small beachside community in Mexico, your cost of living in retirement would only be a fraction of what it was during your working years. The lower your cost of living in retirement, the less of your pre-retirement income you need to replace in retirement.

Currently, my wife and I live outside Toronto, which is one of the highest cost of living areas in Canada. When we retire, we plan on moving to Nova Scotia, which is where I am from originally. If we sold the house we live in right now, we could buy a few acres of oceanfront property in Nova Scotia and still have several hundred thousand dollars left over.

If appropriately done, geographical arbitrage can have the dual benefits of increasing your current standard of living while at the same time reducing your cost of living and therefore reducing how much you need to save for retirement.

Geographical arbitrage is not something that you need to do. If you are happy living where you are, that is great. However, if you plan to move to a new city or country when you retire, you will need to consider how your cost of living will change as that will decrease or increase the amount of your pre-retirement income you must replace to fund your lifestyle.

What costs will increase during retirement?

Three costs generally increase during retirement.

- Healthcare

- Travel

- Social costs

Healthcare

Healthcare is likely the most significant increased expense for retirees, especially in the U.S. According to a report from Fidelity, the average married couple retiring at 65 in the U.S will need to plan on spending $285,000 on healthcare-related costs in retirement.

Healthcare is a significant issue you will need to contend with in retirement, and you must consider health care costs when planning how much annual income you will need in retirement.

Travel

Travel is the most obvious expense that increases in retirement. When they have nothing but free time, many people decide to spend more money on travel. The more you value travel, the more this cost will increase in retirement.

This is a tricky issue because, for some people, this could be their most significant retirement expense. For others, it may not change at all. You will want to think about how often you plan on traveling and what that will do to your cost of living in retirement.

Eating out and other social costs

When do you spend most of your money during your working years? For most people, the answer is on weekends and vacations. When we have time to catch up with friends and family, we are more likely to go out to dinner, for drinks, or to other social events.

You need to ask yourself if every day was a Saturday, how would your social life change, and how much would that cost? Because guess what? In retirement, every day is a Saturday.

Emergency fund

It’s a smart idea for you to increase the size of your emergency fund in retirement. This is especially true if your retirement income is largely dependent upon investment returns, which can be very volatile.

If the bulk of your retirement income comes from investments and the value of your investments and the income they produce drops significantly, that could jeopardize your retirement.

However, if you had a big pile of cash sitting on the sidelines, you could draw down on that cash while you wait for your investments to recover.

There is no magic number to determine how much money you should hold in cash during retirement. It will depend largely on your retirement income sources, level of risk in your investments, and personal preferences. If you were comfortable with a 3–6-month emergency fund while you are working, perhaps you want to consider a 12+ month emergency fund in retirement.

Crunching the retirement savings numbers

To determine how much you need to save each month to fund your retirement, you only need to know the following variables.

- Your current age.

- The age you want to retire.

- Your Current Income.

- Your desired Income replacement ratio.

- Your current retirement savings.

- Whether or not you have a workplace pension or retirement plan.

- How much you are entitled to in government pensions and benefits.

The massive impact of workplace pensions and retirement plans

If your employer offers a pension or a matching contribution retirement plan, you need to make sure you are participating and maximizing your benefits, as these tools have a massive impact on your retirement savings plan.

To illustrate the impact workplace retirement plans have on how much you need to save for retirement, let’s consider an example under three different scenarios.

- Where you have no workplace pension or retirement plan.

- Where you have an employer matching retirement plan.

- Where you have a defined benefit pension plan.

The assumptions

Let’s say you are 35 years old, making $85,000 per year, and want to replace 70% of your income when you retire at 60. Let’s also assume you have $60,000 in retirement savings right now. Finally, I’ll assume your retirement portfolio earns an annual return of 5%.

How much do you need to save for retirement every month?

Scenario 1: No workplace pension or retirement plan

In this scenario, you are entirely on your own when it comes to retirement savings, and to fund your retirement by age 60, you would need to save $2,147 per month to reach your retirement goals.

Scenario 2: Employer Matching retirement plan

If you are lucky enough to have a defined contribution retirement plan or a 401k, the retirement saving math gets much easier.

Let’s say your employer matches up to 5% of your salary into a retirement saving plan. Both you and your employer contribute $4,250 per year for a total of $8,500 in annual retirement savings.

You would still need to save $2,147 per month, but your employer would be paying $354 per month through the matching contribution. That means You would need to save $1,793 per month out of your pocket.

Scenario 3: Defined Benefit pension plan

Defined benefit pensions are the ultimate retirement planning tool because a pension is designed to replace a certain percentage of your pre-retirement income. If you have been following along, the entire point of saving for retirement is to replace pre-retirement income, so it’s pretty great to have a tool designed to accomplish that exact goal.

The problem with defined benefit pension plans (apart from how few people have them) is that they are very complex. There are a lot of weird formulas and assumptions that go into calculating your pension.

The critical question you will want to ask Human Resources or your company pension committee is what percentage of your income will your pension replace if you retire at your desired retirement age?

If you had a defined benefit pension that will replace 40% of your income when you retire at age 60, then your additional savings would only need to replace 30% of your income (70%-40%).

In this scenario, you would only need to save an additional $720 per month to top up your pension income in retirement.

Government pensions and old-age benefits

Whether or not your workplace offers a pension, it’s important to calculate how much you are entitled to from government-sponsored pensions and old-age benefits when you retire.

The more income you expect from government benefits in retirement, the smaller your income replacement ratio needs to be. Every dollar you receive in government retirement benefits is a dollar you will not have to save and replace using your personal retirement savings.

- For those in the U.S: The United States Social Security Administration has provided a calculator to help you determine how much you might receive from social security in retirement, click here to access the calculator.

- For those in Canada: The government of Canada has information here reviewing how much income you might expect to receive from the Canadian Pension Plan (CPP) in retirement. The Canadian government has also provided information detailing how much income you might expect to receive from Old Age Security (OAS) in retirement here.

Everything you need to know to crunch your own retirement savings numbers

Let me teach you exactly how I calculated the monthly retirement savings numbers under each of the above three scenarios. Once you have decided what level of income you want to replace in retirement, you only need to calculate two numbers.

- The lump-sum you need to have saved on the day you retire.

- How much do you need to save each month to save up that lump-sum.

I will teach you how to easily calculate each of these so you can calculate for yourself how much you need to be saving for retirement each month.

The 25 times rule and the 4% rule

The 25 times rule and the 4% rule are two rule of thumb estimates that are popular in DIY retirement planning.

- The 25 times rule states that once you save 25 times your annual living expenses, you have enough money to retire.

- The 4% rule is then used to determine how much of your retirement nest egg you could live off each year.

If your annual expenses were $50,000, the 25 times rule would say you need at least $1,250,000 to retire ($50,000 X 25). If you followed the 4% rule, you could withdraw a maximum of $50,000 per year ($1,250,000 X 4%) and cover your living expenses.

Modifying the 25 times rule to calculate your lump-sum retirement savings

The trouble with the 25 times rule is that it is based on your current living expenses, which, as we have covered, will change dramatically in retirement. You can, however, use the 25 times rule to answer one remaining retirement planning question; “how much money do I need to have saved by the time I retire?”

Returning to our previous example, assuming you have a pre-retirement income of $85,000. You would like to replace 70% or $59,500 of that income in retirement.

Here is how we can use the 25 times rule and 4% rule together to figure out how much money you need to save to provide you $59,500 in income in retirement.

- Simply multiply you’re desired retirement income by 25 to arrive at the minimum amount you need to save by retirement. In this example, you need to save $1,487,500 ($59,500 X 25) by the age you wish to retire.

- Then you would use the 4% rule to withdraw $59,500 ($1,487,500) each year in retirement.

Here is a handy DIY retirement formula to determine the minimum amount you need to save to fund your retirement.

Retirement savings goal= (Pre-retirement income X replacement ratio) X 25

This assumes that you are funding your entire retirement from your personal savings, which is not the case for most people. The formula can easily be adapted to reflect how much of your pre-retirement income is covered by pensions and other sources of retirement income.

Returning to our three scenarios above, let’s calculate the lump sum required with and without a defined benefit pension.

- Lump-sum retirement savings goal (no pension)= ($85,000 X 70%) X 25= $1,487,500

- Lump-sum retirement savings goal (with pension)= ($85,000 X 30%) X 25= $637,500

Remember, in this example, you had a pension that would replace 40% of your pre-retirement income. That means you only needed to save a lump sum big enough to cover 30% of your pre-retirement income.

Using Excel to calculate your monthly retirement savings

Once you have your lump sum, you are ready to calculate how much money you need to start saving today to ensure you have that lump sum on the day you retire.

Here is how you can easily calculate how much you need to be saving for retirement each month using Microsoft Excel.

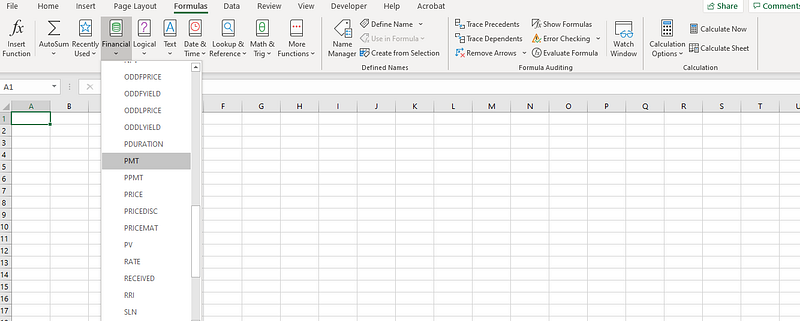

Open up Excel, scroll over to “Functions,” and under “Financial,” select “PMT.”

Click on “PMT,” and Excel will open up a panel that looks like this.

Here is how to fill out the field to use the PMT formula to calculate monthly retirement savings.

- Rate: Enter the assumed return on retirement investments and divide by 12. In our example, we assumed a 5% rate of return, so under Rate, enter “5%/12”

- Nper: Enter the number of months until you retire. In our example, we wanted to retire in 25 years, which is equal to 300 months, so under Nper, enter “300”.

- PV: Enter the total amount you have saved for retirement right now. In our example, we assumed we had $60,000, so under PV, enter “60000”. Do not enter a comma or use a dollar sign.

- FV: This is the amount of the lump sum we need to save by the time we retire. If you did not have a pension, this was equal to $1,487,500; we will go with that and enter “-1487500”. Again enter this number without a comma or dollar sign. Also, make sure you put a “negative” before the number, or you’ll get the wrong result. I know it seems odd, but we are modifying another formula to fit our purposes, so make sure you input everything precisely right.

- Type: leave this blank.

Hit enter and poof; Excel spits out how much you need to save each month to accumulate a lump sum of $1,487,500 in the next 25 years.

- Without a pension, you need to save $2,147 per month to have a lump-sum savings of $1,487,500 by retirement.

- With a pension, you need to save $2,147 per month to have a lump-sum savings of $637,500 by retirement.

Assumptions, limitations, and a word of caution

The 25 times rule and the 4% rule are “rules of thumb,” which means they are never 100% accurate. It’s essential to understand the assumptions made in these rules of thumb to understand their limitations better and consider them when determining your DIY retirement plan.

Early retirees should not rely on the 4% rule

The first limitation you need to know about the 25 times and 4% rule is that the research that informs these rules was intended for a 30-year retirement. If you are planning for a retirement longer than 30 years, you run the risk of running out of outliving your money.

Investment assumptions and sequence of return risks

The 25 times rule and the 4% rule assume you’re invested in a 50/50 portfolio made up of 50% stocks and 50% bonds. Given where bond yields are today, it may not be realistic to assume that a 50/50 portfolio will have high enough returns to sustain a 4% withdrawal rate for 30 years.

One solution to that problem could be to weigh your portfolio to include a higher share of stocks compared to bonds. Doing so will increase the expected return but increase the overall level of risk in your portfolio. A higher weighting towards stocks opens you up to what is called sequence of returns risk.

Sequence of return risk refers to the possibility that in your early years of retirement, the stock market could decline significantly. If you are withdrawing 4% from your portfolio at the same time it is dropping 20% or more in value; it will be unlikely that your portfolio will be able to sustain your desired annual income during retirement.

Choose a realistic withdrawal rate

A 4% withdrawal rate does not make sense for everyone. You may want to consider a lower withdrawal rate if you are not confident your portfolio could generate enough income to sustain your retirement.

If you are planning for a retirement longer than 30 years, have a portfolio that is too conservative, or are concerned about sequence of returns risk, you might consider a more conservative withdrawal rate such as 3.5% or 3%.

Returning to our previous example, here is how much you would need to save to generate $59,500 in retirement income using a 4%, 3.5%, or 3% withdrawal rate.

- Using a 4% withdrawal rate, you would need to save $1,487,500.

- Using a 3.5% withdrawal rate, you would need to save $1,700,000.

- Using a 3% withdrawal rate, you would need to save $1,983,333.

You will notice that the lower our withdrawal rate, the larger of a lump sum you must save by retirement. Which makes perfect sense if you think about it; if you want the same income in retirement and you are withdrawing a smaller percentage from your savings to provide that income, the total savings must be larger for the .math to work.

Here is how to quickly and easily find out what lump retirement sum savings you need for any withdrawal rate you select.

Lump-sum retirement savings goal= (Pre-retirement income X replacement ratio) ÷ withdrawal rate.

Here is how much you need to have saved to replace 70% of an $85,000 income using a 3% withdrawal rate in retirement.

(70% X $85,000) ÷ 3%=$1,983,333.

Choose a realistic withdrawal rate based on your circumstances, including the length of planned retirement, other retirement income sources, and portfolio characteristics.

The importance of Automating your retirement savings

Once you have figured out how much you need to save for retirement, you need to do only one more thing to ensure you meet your retirement savings goal; automate your savings.

If you know you need to save $1,793 per month to meet your retirement savings goal, call up your bank and set up an automatic withdrawal from your checking account into your retirement accounts each month.

It should go without saying, but of course, you should only do this if you can afford to save $1,793 (or whatever your number is). A retirement savings plan only works if you can afford it.

DIY retirement planning takes a lot of work but is worth it

As we have covered, there is a lot of work to figure out how much you need to save for retirement.

It’s important to remember that if you don’t save for retirement, your best-case scenario is working until you die.

There are four steps to figuring out how much you need to save for retirement.

- Decide how much income you will need in retirement.

- Determine how much money you need to have saved on the day you retire to generate your retirement income.

- Calculate how much you need to start saving right now.

- Ensure your success by automating your savings.

The amount of income you’ll need to replace in retirement will be determined by which living expenses will go up and which will go down in retirement, and by how much. A 70% replacement ratio is commonly used and is a good starting point in your analysis.

How much money you need to have saved by the time you retire is determined by the withdrawal rate you choose. A 4% withdrawal rate is commonly used, but it’s important to customize a withdrawal rate that fits your circumstances.

Once you know how much you need to save each month to fund your retirement, guarantee your success by automating your savings.

It’s not easy, but if you put in the work, you can have the retirement you deserve.

Did you love this article and want to follow me? Join Medium here and keep reading! Want more of me? You can also find me on Twitter, and exclusive content on Substack, showing how I’m building financial freedom.

This article is for informational purposes only. It should not be considered Financial or Legal Advice. Not all information will be accurate. Consult a financial professional before making any significant financial decisions.

Originally published at Benlefort.com