How to Create the Investment Diversification Heat Map in Python

Cordell Tanny has over 24 years of experience in financial services, specializing in quantitative finance. Cordell has previously worked as a quantitative analyst and portfolio manager for a leading Canadian institution, overseeing a $2 billion multi-asset retail investment program.

Cordell is currently the President and co-founder of Trend Prophets, a quantitative finance and AI solutions firm. He is also the Managing Director of DigitalHub Insights, an educational resource dedicated to introducing AI into investment management.

Cordell received his B. Sc. in Biology from McGill University. He is a CFA Charterholder, a certified Financial Risk Manager, and holds the Financial Data Professional charter.

Visit trendprophets.com to learn more.

This article is part of my series sharing tools and tips used by professional investment strategists. The Python code can be found at the end of the article.

How to Create the Investment Diversification Heat Map in Python

Investment diversification is a must in any portfolio. While this is incredibly true, it has also become an investment lingo cliché. And whenever markets hit a crisis, the pros will always preach that diversification helps prevent extreme losses that can (and will) result by putting all your eggs in one basket.

And I fully subscribe to this!

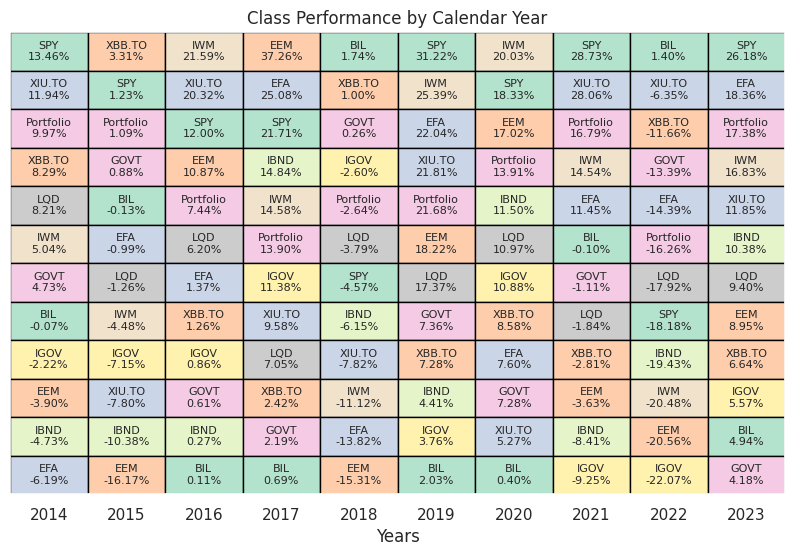

Diversification is a pillar of a long-term investment plan. And here is the visual everyone will use to prove it. I’m sure you’ve seen it.

The point of this heat map is to show you that you never know which asset class will be the best performer in any given year, and that by diversifying with stocks and bonds, you can create a smoother ride. The pink cell in the graph above is a balanced portfolio of 60% SPY and 40% AGG. We can see that it is never at the top, and more importantly never at the bottom.

It’s a very powerful visual and you can put anything you want into this. Your favourite stocks, ETFs, crypto currencies, etc.

And here is the code so you can do this yourself! Enjoy.

Note: I love sharing the many things that I have learned over the course of my career as a quant. Not everything you see on Medium needs to be a deep learning model that has no application in the real world. I want to give you some of the small things that will make you a better investor, a better quant, and innovate! If you like free code like this, subscribe to the Digital Hub newsletter at dh-insights.com

And if you want to really see what I can do, subscribe to Trend Prophets!

Cheers.

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import seaborn as sns

import yfinance

from matplotlib.patches import Rectangle

sns.set()

# declare the tickers

# Create a list with the tickers to use.

tickers = ['SPY', 'IWM', 'GOVT', 'LQD', 'EFA', 'EEM', 'IGOV', 'IBND', 'XIU.TO',

'XBB.TO', 'BIL']

# select the start and end dates

start_date = '2013-12-31'

end_date = '2023-12-31'

# retrieve the prices, resample to yearly

df_prices = yfinance.download(tickers, start_date, end_date)['Adj Close']

df_prices.index = pd.to_datetime(df_prices.index)

df_prices = df_prices.resample('Y').last()

# convert to returns

df_returns = df_prices.pct_change().dropna()

# create a diversified portfolio

portfolio = (df_returns['SPY'].mul(0.6)) + (df_returns['GOVT'].mul(0.4))

portfolio.name = 'Portfolio'

# inspect the results

print(portfolio)

# add the balanced portfolio returns to the dataframe

# multiply all decimal format returns by 100 and round to 2 decimals

df_returns_final = pd.concat([df_returns, portfolio], axis=1).mul(100).round(2)

# inspect the final returns dataframe

print(df_returns_final)

# function for plotting

def calendar_year_heatmap(df_returns):

"""

Creates a heatmap showing the annual performance of various asset classes,

with each column representing a year and each cell showing the performance

of an asset class in that year. Asset classes are sorted by performance within

each column, with the highest returns at the top.

Parameters:

- df_returns: A pandas DataFrame with a DateTimeIndex representing dates and columns

representing different asset classes. The values are the annual returns

of the asset classes.

The function plots a heatmap where each cell's color is associated with its asset class,

and the cell is annotated with the asset class ticker and its annual return. Black borders

separate the cells.

"""

fig, ax = plt.subplots(figsize=(10, 6))

# Extract just the year part from the DateTimeIndex to identify unique years

unique_years = df_returns.index.year.unique()

num_years = len(unique_years)

# Assign a unique color to each ticker for identification across the heatmap

tickers = df_returns.columns

color_map = {ticker: plt.cm.Pastel2(i % len(plt.cm.Pastel2.colors)) for i, ticker in enumerate(tickers)}

# Iterate through each year, creating a column in the heatmap for each

for i, year in enumerate(unique_years):

# Filter the DataFrame for the current year and transpose for easier sorting

df_year = df_returns[df_returns.index.year == year].T

# Sort the transposed DataFrame to have the highest returns at the top

df_year_sorted = df_year.sort_values(by=df_year.columns[0], ascending=False)

# Plot each ticker's return for the year, using the assigned color and adding a black border

for j, (ticker, row) in enumerate(df_year_sorted.iterrows()):

return_value = row.iloc[0] # Extract the return value from the row

# Create a rectangle representing the asset class's annual return for a given year.

# The rectangle's position and size are determined by (i, j) for the bottom-left corner

# and width & height set to 1, ensuring each cell in the heatmap is uniform.

# 'facecolor=color_map[ticker]' assigns a unique color to each asset class based on the ticker,

# making it easy to identify across different years. 'edgecolor='black'' adds a distinct black border

# around each cell, enhancing the visual separation between different asset classes' returns.

rect = Rectangle((i, j), 1, 1, facecolor=color_map[ticker], edgecolor='black')

ax.add_patch(rect)

# Annotate the rectangle with the ticker and its return value

ax.text(i + 0.5, j + 0.5, f'{ticker}\n{return_value:.2f}%',

va='center', ha='center', fontsize=8)

# Set up the axes, labels, and title

ax.set_xlim(0, num_years)

ax.set_ylim(0, len(tickers))

ax.set_xticks([i + 0.5 for i in range(num_years)])

ax.set_xticklabels(unique_years)

ax.set_xlabel('Years')

ax.set_yticks([]) # Remove y-axis tick marks

ax.set_yticklabels([]) # Clear y-axis tick labels

ax.set_title('Class Performance by Calendar Year')

plt.gca().invert_yaxis() # Invert the y-axis to have the best returns at the top

plt.show()

calendar_year_heatmap(df_returns_final)

# note: the color palett I chose doesn't accomodate 11 tickers. You are

# better off creating your own!