Millennials and Finance

How to Become Financially Literate

Not just a problem for students and schools

Last Saturday and out of the blues, my best friend texted me:

It is really a shame that we did not learn about investing ten years ago!

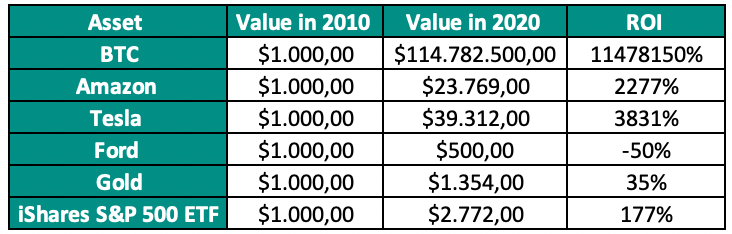

I couldn’t agree more with his words. Funny enough, as he texted me, I was preparing an Excel table to demonstrate a financial “what if” scenario for a presentation I was about to give the next day. I shared the following table immediately with him to annoy him even further — just something friends do to each other.

In my presentation, I was going to talk about the importance of financial literacy and why it is vital to start saving and investing at an early age.

With the current situation worldwide, the majority of people are struggling to make ends meet. On top of that, the student debt in the U.S. is at a staggering record high of $1.6 trillion. Financial literacy is now more critical than ever. The question, however, remains, who is responsible for teaching financial literacy?

Teens and financial literacy

A study published in 2014 evaluated the financial literacy of 15-year-olds in 18 countries. The U.S. ranked at best 8th and at worst 12th among the 18 countries in the Organization for Economic Cooperation and Development’s assessment. These poor scores are a national problem in the U.S., today’s 15-year-olds are just a couple of years away from potentially taking out student loans — a dept decision that will follow them for the years and decades to come.

The study showed a correlation between a student’s background and financial literacy. For example, Kids from higher-income families, or had at least one parent in a skilled occupation (especially in finance) tended to score higher. Students with their own bank account or a job also scored high in the study.

Countries, in which schools taught financial literacy, scored relatively high in this study. Australia and New Zealand, for example, have both developed mandated educational components within their national financial literacy strategy. Another correlation was found in this study between high performance in mathematics and reading and financial literacy skills.

The U.S. released its National Strategy for Financial Literacy in 2011 with educational components relegated to the states. Currently, only four states require students to attend a personal finance course to graduate. Other states require some kind of financial literacy component in classwork.

However, studies also showed that the retention rate on financial lessons is two years at best. This means that financial literacy programs at high school do not necessarily prepare someone years later to buy a home, understand his employer benefits, or save for retirement. Let us not forget that financial products and tools are rapidly shifting and changing. Also new financial model are emerging, such as cryptocurrencies.

Financial literacy is not something to learn only once in your lifetime. It is a process of continuous learning and adapting to new financial products, tools, and challenges.

DIY financial literacy

“Give a man a fish and you feed him for a day; teach a man to fish and you feed him for a lifetime” — Maimonides

A study by the University of Arizona on college students found out that three things help with their financial behavior: parental involvement, taking a personal finance class, and having a part-time job or other hands-on money experience.

However, some parents cannot help their kids with these topics because they are not financially literate themselves. The solution is a mix of personal finance classes and a continuous DIY learning process. The following points are relevant to an excellent financial literacy DIY:

- Learn the basics

- Do the research

- Stay informed

Learn the basics

Learning the basics of finances is pretty straightforward. The basics can be taught at schools, universities, and other educational centers. Financial savvy parents can teach their kids the basics as well. The internet is also a great source of information for financial literacy.

There are also great books to improve financial literacy and to teach you the basics. Rich Dad Poor Dad, The Intelligent Investor, and The Millionaire Next Door are good examples to start the journey of financial literacy.

Financial basics are: Budgeting, saving, and investing. These points are handled later in this post.

Do the research

Do not take the first offer you receive in your mailbox. There are plenty of websites to compare competing products, such as credit cards, loans, and broker accounts. Admit that you do not know everything and utilize the power of the internet to help you make better decisions. Dig in deep just before you make a decision, search for YouTube videos, reviews, and other information sources. Believe it or not, personal finance products change fast and rapidly.

Stay informed

Subscribe to finance podcasts, blogs, or YouTube channels to stay informed about updates and new products in the financial sector. Staying informed might be the last thing you need to pursue investment in a specific asset like Cryptocurrency. Robinhood, for example, allowed investing in fractional shares in 2020, the sources above would have informed you about this update, and you might have bought some fractional shares to expand your portfolio.

Financial basics

Let me ask this, do you know how to manage your money? Watching YouTube finance videos makes me think that people currently spend way too much money on convenience and for some reason, finance YouTubers announced coffee to be their sworn archenemy.

Simple money management is summarized in budgeting, saving, and investing.

Budgeting

Know your reoccurring costs. These costs are the first thing to go from your monthly budget. Reoccurring costs are costs that are due monthly, bimonthly, quarterly, semi-annually, or annually.

Write down these costs, and the remaining is what you have to spend in the given period. Stick to a strict budget and do not overspend. Plan a strict budget for food, outings, clothes, etc. and control monthly if you can optimize this budget even further. Do not forget to put some money aside for investing, saving, and other goals — budget monthly for your goals, such as your next vacation, your next laptop, or phone.

There are multiple apps that you can use to plan a budget and to track your spending. You might also develop your own Excel-file to track it down — This is what I do.

Saving and investing

My parents always asked me to save money, but they never taught me how to invest my money. I had my savings in a saving account. Sadly, I learned about investments, compound interest, and the stock market in my early 30s.

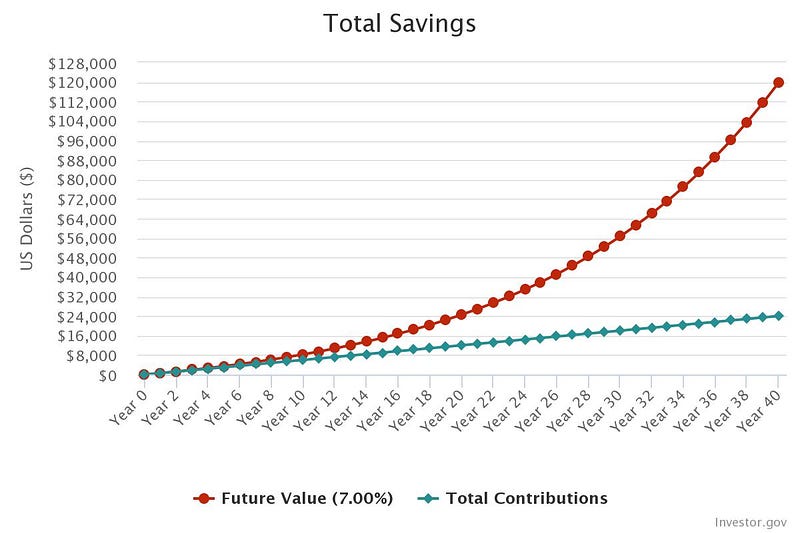

If a college student started investing 50 dollars monthly with an assumed annual interest rate of 7%, in 40 years, this student would have saved almost $120 thousand, even though the student only contributed $24 thousand. This is the power of compound interest. No one taught me this as a teenager or as a college student and I still regret it.

The takeaway

Financial literacy is essential, and it is the responsibility of each one of his to teach himself. We can argue that schools or colleges should mandate a financial literacy course, but we should also be aware that financial literacy changes and updates frequently. It is up to us to stay informed and know the new products and aspects. I doubt schools currently teach cryptocurrencies. Use the power of the internet to gather information, find online courses, and continue learning. Financial literacy is a never-ending subject.

Sources

-------------------------------------------------------

1- https://www.cnbc.com/2014/07/08/teen-financial-literacy-test-country-with-most-money-smarts-not-the-us.html

2- https://www.cnbc.com/2015/04/02/financial-literacy-not-just-a-problem-for-students.html

3- https://medium.com/illumination/its-time-schools-focus-on-financial-literacy-d7a7560d4380

4- https://www.investor.gov/financial-tools-calculators/calculators/compound-interest-calculator

Walid Al Otaibi -WAO- works at an engineering company in Germany as a Project Manager. He manages mainly sustainable energy projects.

He comes from a multicultural background and is located in Germany since 2003. He is writing about Arab Culture, Multiculturalism, Finance, and Trending topics.

The information in this article is not intended to encourage any lifestyle changes without careful consideration and consultation with a qualified professional. This article is for reference purposes only, is generic in nature, is not intended as individual advice and is not financial or legal advice.