How to Become a Millionaire — The One All-But-Guaranteed Way to Wealth

You don’t need to be a entrepreneur or real estate mogul to be wealthy

Prepare to have your mind blown.

I guarantee, everyone reading this article has the ability to grow wealth. It’s not rocket science.

As of 2024, there’s about $2.32 Trillion in circulation, and the US stock market assets add up to an estimated $50.8 Trillion.

There are only 8 Billion people on this planet.

If you can’t find a way to collect, keep and grow even a small amount of that money, you’re either lazy or just lacking creativity.

Odds are, it’s not your fault though, true financial education has been kept out of schools for decades. This is one of the many things keeping the wealthy, wealthy and keeping the poor, poor, it’s time to change that.

Here’s your answer dished and plated for you.

Get Rich Slowly

Let’s say every 16-year old took a class in high school called Money 101.

In that class, each student was given $100 by the state, feds, tax dollars, I don’t care who, but $100 to invest.

- $100 invested at age 16

Age 16 is when most people in the US get their “first” job.

Instead of taxing the shoes off these youngsters, 10% of their pay automatically went into that same investment account.

$12 per hour job

20 hours per week

12 X 20 = $240

10% of $240 = $24

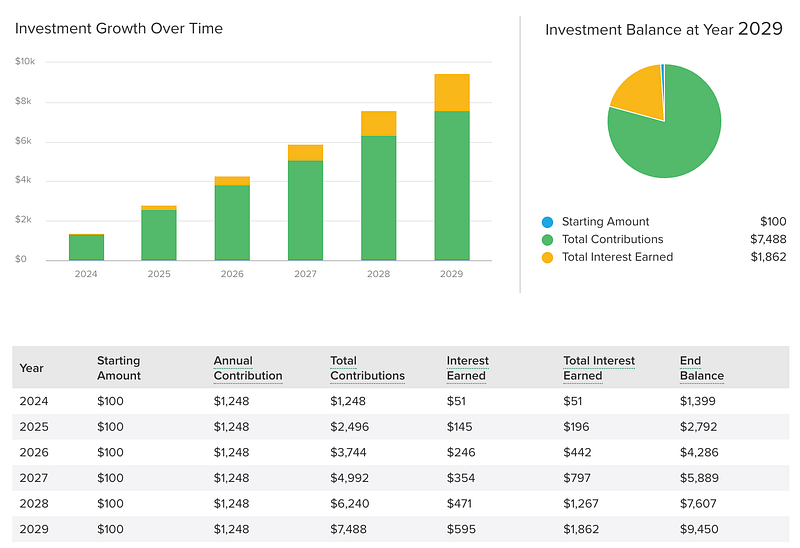

$24 invested weekly for 52 weeks = $1248We’ll start here, here’s what that growth looks like between ages 16–22 with no raises or additional contributions:

That’s $9,450 in an investment account by the time they graduate college

That’s more than the average 30-year old has in their 401K these days.

Now let’s say that 22-year old got their first job out of college earning $45,000 per year.

- 10% is $4,500 invested per year

- 15% is $6,750 invested per year

- 20% is $9,000 invested per year

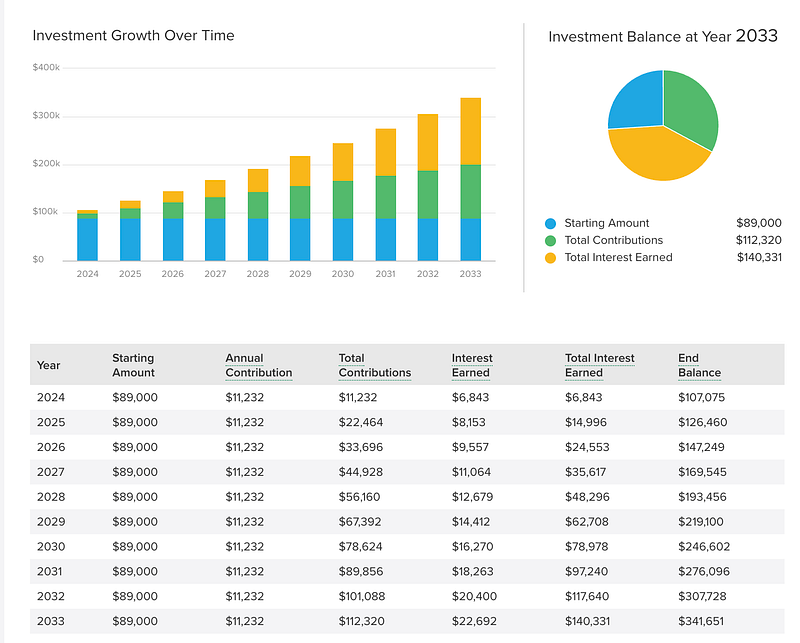

Let’s take the middle of the road approach, 15% is $130 per week.

That’s $89,000 invest by the age of 30

Again, this is accounting for

- No raises

- No additional contributions

- No 401K match

- No additional money coming in from writing on Medium or blowing up as a TikTok star

- 15% of $45,000 per year

This example is meant to show how even the simplest amount of money can grow over time.

Starting with $89,000 at age 30 is where the financial picture starts to change

Let’s say you’re now making $75,000 per year (maybe it’s you and your partner)

- Avoid life style creep and continue investing 15% of your income

- 15% of $75,000 is $11,250

- $216 invested per week

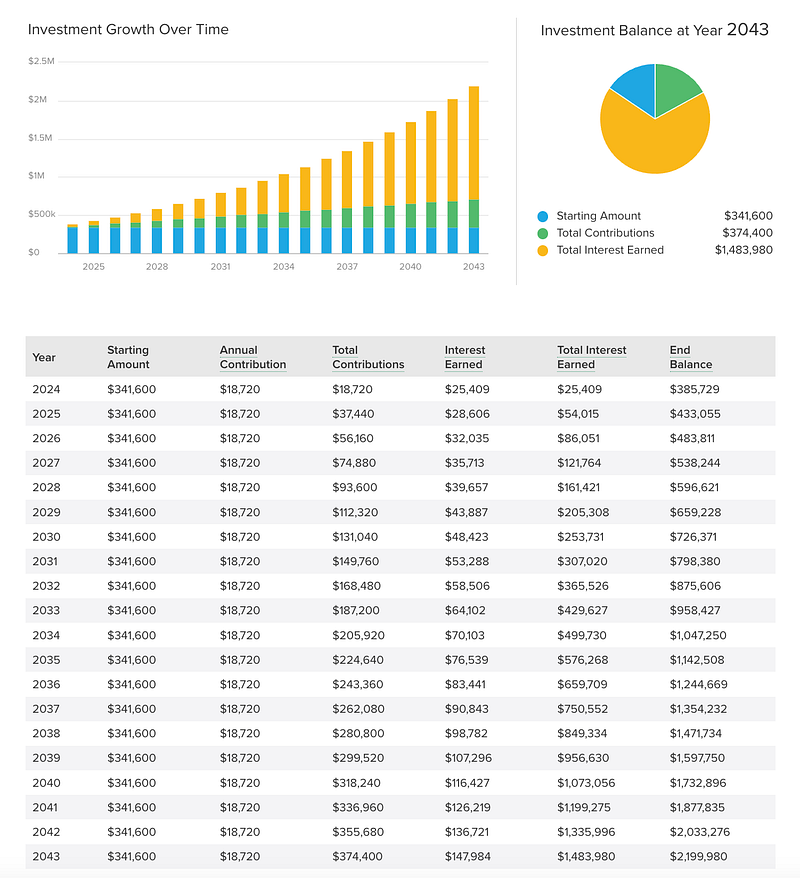

That’s $341,600 invest by the age of 40

Now you’re starting to see the power of compound interest take effect.

- No raises

- No additional contributions

- No 401K match

- 15% of $75,000 per year

- Earned over $140,000 in interest in 10 years

Now let’s become millionaires 🤑

You’re 40 years old, starting with $341,600 invested and making a household income of $125,000 annually.

- 15% of $125,000 is $18,750

- $360 invested per week

Congratulations, you are 60 years old, and you’ve got $2.2 million invested

In most places in the US, that’s a very healthy number to retire on (sorry for all you Californian’s like me, this won’t get you too far)

None of these numbers are astronomical.

Remember the biggest factors we left out:

- Not once did we account for an annual raise other than the salary jumps between equations.

- We didn’t include any 401K matches, retirement savings, HSA, or IRA contributions.

- No bonuses, side hustles, inheritance from grandma.

All we did was invest consistently between the ages of 16 and 60, 44 years.

But wait… how would you like to double this money?

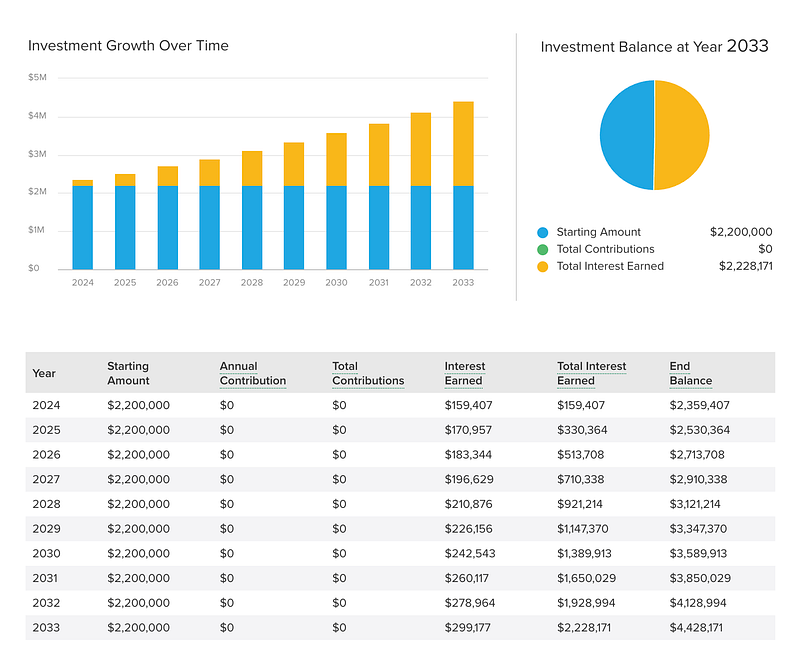

Say that at 60 years old, you decided you were not ready to retire with your $2.2 million but you wanted to take a break, exit the corporate world, and take a fun job that just paid for your living expenses.

- No more contributions to your investment account.

- You get to keep all the money you make.

- You don’t touch the money invested.

- Your investments continue to grow for 10 more years.

You are now retired at 70 years old with $4.43 million dollars

Go live your days on the golf course, laying at the beach, or chilling with your grandkids.

You’re set.

What do you think of this math?

- Do you think students should learn to invest in high school?

- Do you think it’s attainable to invest 15% of your income consistently?

- How do you think these numbers would change if you invested more up front earlier in life?

Let me know in the comments.