How the Recent Supreme Court Ruling on Student Debt Forgiveness Impacts on Borrowers

By Giselle Castaneda and Dr. Benjamin M. Drury

The Supreme Court’s ruling against Joe Biden’s student debt forgiveness plan will have a significant impact on the stability of millions of borrowers who were hoping for relief. The decision means that these borrowers will not receive the debt forgiveness they were counting on, which can have far-reaching consequences for their financial well-being and overall stability. In response to accusations of failing to deliver on his promise, Biden deflected the blame onto Republicans, highlighting what he perceives as their hypocrisy. He pointed to the higher cost of the paycheck protection program approved by Republicans in 2020, which provided loans to businesses and allowed loan forgiveness. Biden argues that Republicans did not hesitate to support such loan forgiveness when it benefited businesses, including some members of Congress. However, when it came to providing relief to hard-working Americans burdened by student loan debt, Republicans obstructed and opposed the plan. Contrast between loan forgiveness for businesses and the resistance to student debt relief is seen by Biden as evidence of Republican hypocrisy. He argues that Republicans were willing to support loan forgiveness when it served their own interests but obstructed relief when it would have benefited millions of Americans. This perceived hypocrisy strengthens the sense that the Supreme Court’s ruling against the student debt forgiveness plan was unfair and inconsistent with the treatment of other forms of debt relief.

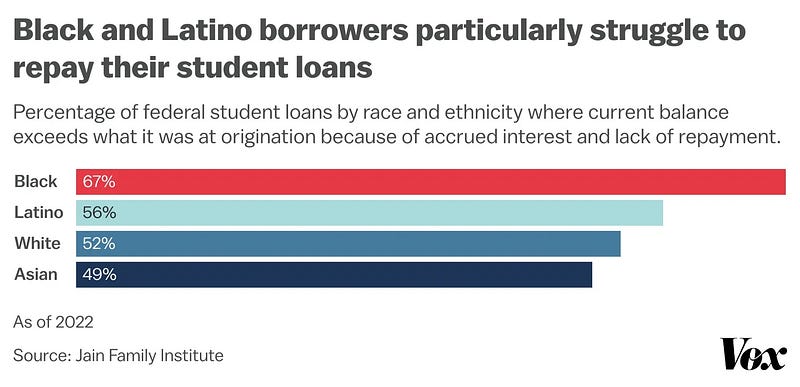

One of the immediate effects of the ruling is the continued burden of student loan debt on borrowers. Many individuals have been struggling with high monthly payments, which can eat into their disposable income and make it difficult to meet other financial obligations. Student loan debt can limit borrowers’ ability to save for the future, invest in assets such as homes or businesses, or pursue other financial goals. By denying debt forgiveness, the Supreme Court’s ruling prolongs this burden, making it harder for borrowers to achieve financial stability. Another effect of the ruling is the continued rapid expansion of generational wealth inequality. Student loan debt disproportionately affects younger generations, particularly millennials and Gen Z, who have taken on substantial debt to pursue higher education. By denying debt relief, the ruling perpetuates the disparity between those burdened by student loan debt and those who have already paid off their loans or never had to take on significant debt. This unequal distribution of debt places an additional strain on borrowers and can hinder their ability to build wealth and achieve economic stability. Another way the ruling is impacting borrowers extends beyond immediate financial considerations. High levels of student loan debt can lead to mental and emotional stress for borrowers. Anxiety and pressure associated with mounting debt can affect individuals’ overall well-being, mental health, and quality of life. Our Supreme Court’s decision to reject the debt forgiveness plan prolongs the uncertainty and stress that borrowers experience, potentially hindering their ability to thrive personally and professionally.

What is perhaps most curious about the potential effects of this ruling moving forward is the continued emphasis on loan repayment reinforces the idea that the primary objective of higher education is to acquire marketable skills and secure a job that can generate income to repay debts. Placing education in this lens with such narrow focus on job outcomes can overshadow the broader goals of education, such as personal growth, critical thinking, cultural enrichment, and civic engagement. In a fundamental way, this ruling will undoubtedly reinforce the view that education is primarily transactional, where students invest in degrees solely to maximize their future earning potential. Commodification of higher education has turned your average Division I college campus into an expensive resort with an emphasis on comfort over academics. America is home to the prevailing belief in meritocracy, which asserts that anyone can attend college and achieve anything with a college degree. This reality has led to our current situation where our collective pursuits of the American Dream through education now comes with the burden of trillions of dollars in educational debt because the jobs they are promised are not there. We graduate millions of students every year for an available thousands of jobs. In many ways, student loans and student loan debt are hindering the growth promised to a graduating class of highly educated baristas.

Student loan debt has been identified as a drag on economic growth and mobility. Stability of our broader economy is also a consideration as it may be affected by the ruling. Think about it…limiting borrowers’ ability to invest in homes, start businesses, or make other significant financial contributions, the ruling can impede economic activity and innovation. We’re stalling out the economy by forcing these borrowers to pay back into a broken education system. Overwhelming student loans may also contribute to a decrease in consumer spending as borrowers allocate a larger portion of their income to debt repayment, potentially impacting various sectors of the economy. Our Supreme Court’s ruling against student debt forgiveness has significant implications for the stability of millions of borrowers. It prolongs the burden of debt, exacerbates generational wealth inequality, affects borrowers’ mental well-being, and potentially hampers economic growth. If anything, the ruling reinforces the need for comprehensive solutions to address the student debt crisis and underscores the challenges faced by individuals seeking financial stability in the face of mounting debt.