The Beginners Guide to Understanding Your Startup Options

The visual “get smart fast” guide to understanding your options and key questions you should be asking

DISCLAIMER: I am not a financial advisor, and the contents of this article should not be taken as “the law”. Always consult with an actual financial advisor or an attorney when working with your options. I just know this stuff is really complicated, and even having an understanding of the basics is tremendously valuable.

We’ve been hiring a lot lately for our companies, Learn In and BookClub. One of our founding principles is to bring people on who are aligned to our mission, and one way to help do this is by offering stock options as part of every compensation package.

Many of these amazing people have never worked in a startup before, and haven’t had to deal with stock options. As such, they have a lot of questions trying to understand them, what exactly they’re being granted, and how exactly they work.

Options are complicated. After 7 years of dealing with them, I still feel like I learn something new in every discussion or question a new team member brings up. As a new employee in a startup, you may or may not have dealt with stock options before, and either way, they can be infuriatingly frustrating to get your arms around and understand their ultimate value to you. Thus I wanted to get share my understanding in writing to at least help establish a foundation for others as they’re trying to figure out how in the world they work.

As we go through this article, key terms in understanding your options will be in BOLD and will either have an explicit definition or one that can be taken in context.

What is an option?

Let’s first get a clear understanding of what exactly an option is.

Suppose I own a 2018 Tesla Model S P100D (I wish!).

Typically vehicles are seen as depreciating assets, meaning they lose value with time. However, Elon Musk has been extremely vocal about Tesla’s being appreciating assets that theoretically increase in value over time, as many of their features are software-based and they can continue to release new features to the vehicles via over-the-air software updates. Theoretically is the operative word here.

One of the big features Musk has touted is fully-automated self-driving. By this, he means you get in the vehicle, punch in your destination, and it drives from point A to B without any human intervention.

He claims this feature would dramatically increase the value of owning a Tesla.

Suppose Musk announces all Tesla’s will receive the fully-automated driving feature in June of this year (it is now March).

I, as a staunch skeptic who has been burned by Musk previously, don’t believe this will happen, whereas you are a big believer in him, and bank on it.

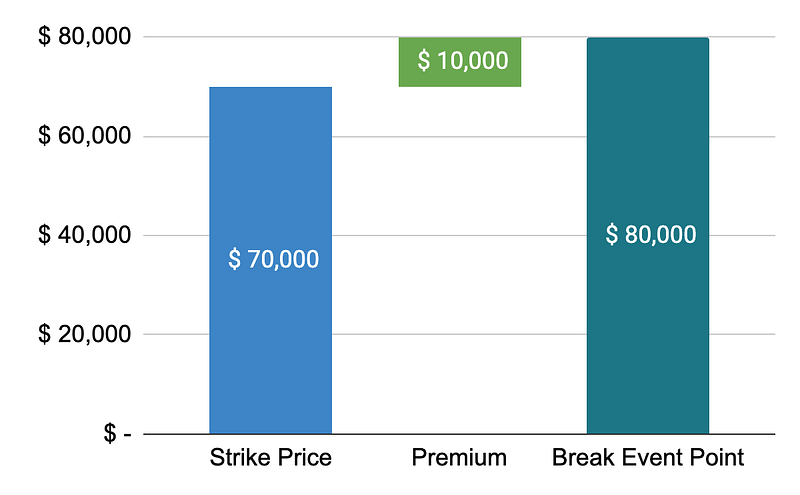

In an effort to get in on the appreciation, you propose a deal to me. The current FMV (Fair Market Value) of my Tesla is $70,000. FMV is the value of an asset, in this case, the Tesla, that the market is generally willing to pay.

You think the value of the vehicle is going to go up a ton this summer and you know that I don’t, and believe this is a chance to get in early on a big opportunity.

You offer to give me $10,000 today (the PREMIUM) for the OPTION to purchase my vehicle sometime within the next three months for $70,000, which we’ll call the STRIKE or EXERCISE PRICE. This option gives you the right, but not the obligation, to purchase my vehicle at the strike price sometime within the next 3 months.

The bet you‘re making is you think the future value of the vehicle is going to be greater than $80,000 (the BREAK EVEN POINT) since you’d be paying $10,000 for the premium plus $70,000 for the vehicle.

Because I think Musk is blowing smoke, this seems like a great deal to me, and here’s why.

There are basically three potential outcomes from here for me, and in the worst-case scenario — I sell you the car for what I believe is market value plus retain the premium.

1. Out of the money

June comes and goes without the announcement. This means the vehicle continues to depreciate (as is normal), and it doesn’t make sense for you to EXERCISE your option, or to actually purchase the vehicle from me. I make $10,000 from your premium and I retain ownership of the vehicle.

2. At the money

June comes, and the announcement is made; you have the option to purchase the vehicle. However, it turns out the appreciation adds exactly $10,000 to the value of the vehicle. You have to decide if you think it still makes sense to purchase the vehicle with the hope of future appreciation. You’ll either be out $10,000 with no vehicle or you pay $80,000 for a vehicle worth $80,000 that might appreciate or depreciate.

3. In the money

June comes and the FMV of Tesla’s explode with the announcement. My vehicle, with an FMV of $70,000 when you purchased the option, is now going for $150,000. You immediately exercise your option and purchase the vehicle from me at the strike price.

This is an amazing deal for you now, as you paid $80,000 in total for a vehicle now worth $150,000. Your faith in Musk heavily paid off, whereas my skepticism cost me the increased value of the vehicle that I already owned, which I was paid what I believe was a fair price.

As the vehicles’ new owner, you can decide what to do with it — whether you want to keep it and drive it, hold onto it in the event of future appreciation, or sell it and realize a quick ROI on your investment.

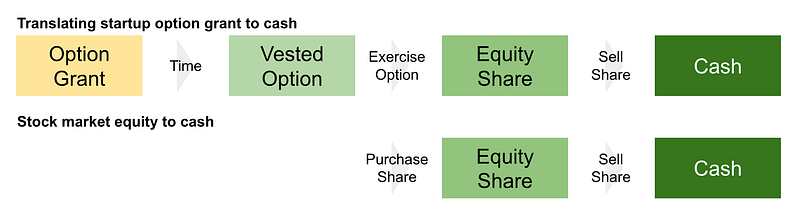

Stock options work in the exact same way, except substitute a share in a business for the Tesla.

What’s different about startup stock options from traditional options or equity?

There are many, but two of the big differences between the options you get at your startup and what you purchase on the stock market: (1) how they’re acquired and (2) how they’re valued.

For the next two sections, we’ll use the following scenario to illustrate the points.

Suppose you’ve recently joined a startup, and you’ve been GRANTED 100,000 options. The grant is the right to acquire up to the option amount at the strike price. It’s kind of confusing because it’s like an option on an option that you pay for with vesting.

Stick with me, it’ll make more sense after these next two parts.

1. How they’re acquired

When the startup grants you the 100k options, instead of your paying a premium for them, like in the Tesla example above, you pay for them over time with your participation in the company through a process called VESTING. Once an option has vested, you actually own the option, and you now have the right to exercise it (refer to the Tesla example for clarification on exercising the option if needed).

There’s what’s called a VESTING WINDOW, which is the period of time over which you earn the options, and a VESTING SCHEDULE, which is the timing on how those options are earned. The GRANT DATE is when the vesting schedule commences.

That’s a lot of information to digest, so let's look at some examples to help illustrate.

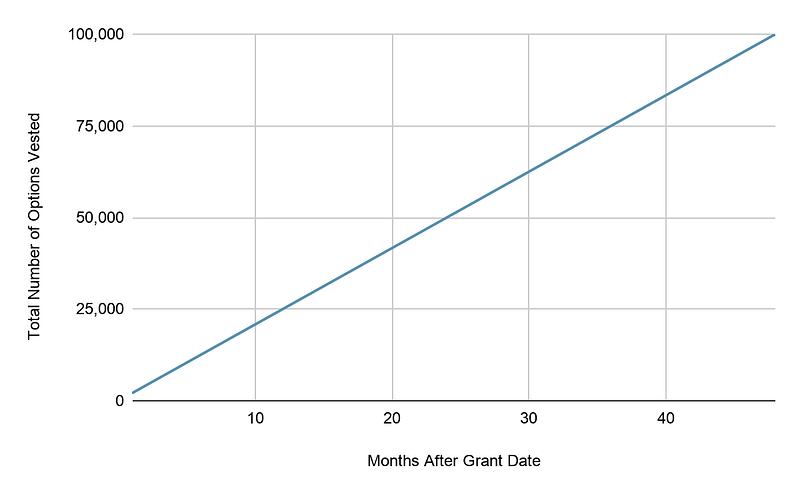

EXAMPLE #1 — Flat Vesting

Suppose your startup has a 48-month vesting window, meaning it takes 48 months for you to earn all of your options. Suppose the scheduled vesting is 1/48th per month. If you were granted 100k options, then that means you would be vesting 1/48th, or ~2,083 options per month.

After 48 months, you would vest all 100k options and they would be available for you to exercise accordingly.

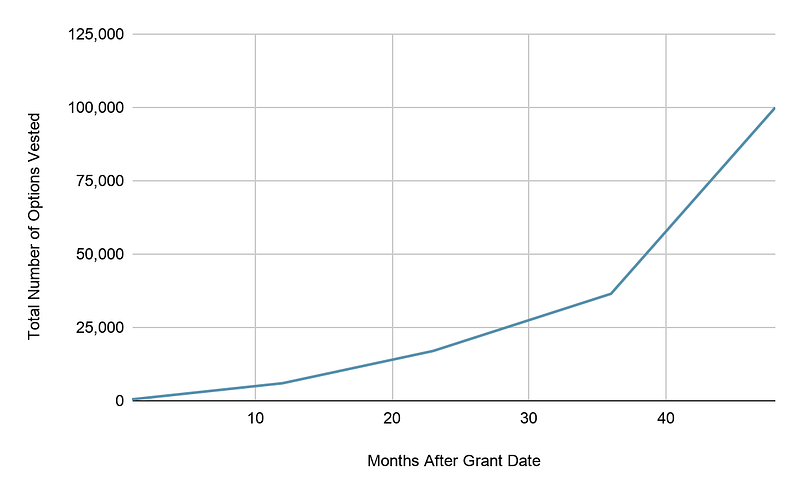

EXAMPLE #2 — Accelerated Vesting

I haven’t seen this, but a vesting schedule could potentially accelerate over time, meaning you vest options faster in the later months of the window than you do in the first months.

Suppose the startup has a 48 month window, and vests 500 options per month for the 1st year, 1,000 per month in the second year, 1,500 per month in the 3rd year, and 5,292 per month in the fourth year.

I use this example to illustrate two points.

First, vesting schedules don’t have to be linear — they can change according to how the company wants to incentivize specific behaviors (and to account for potential tax issues, which we’ll discuss shortly). In this example, perhaps the behavior they’re trying to incentivize is maybe they have a high early drop-out rate, and they want more people sticking around into the 4th year.

Second, vesting can actually be milestone-based. I’ve seen some grants, particularly with “outcome” oriented roles (i.e. sales, business development, recruiting) where vesting occurs in conjunction with the individual hitting specifics deliverables. In those instances, graphing the vesting schedule may look something similar to this example.

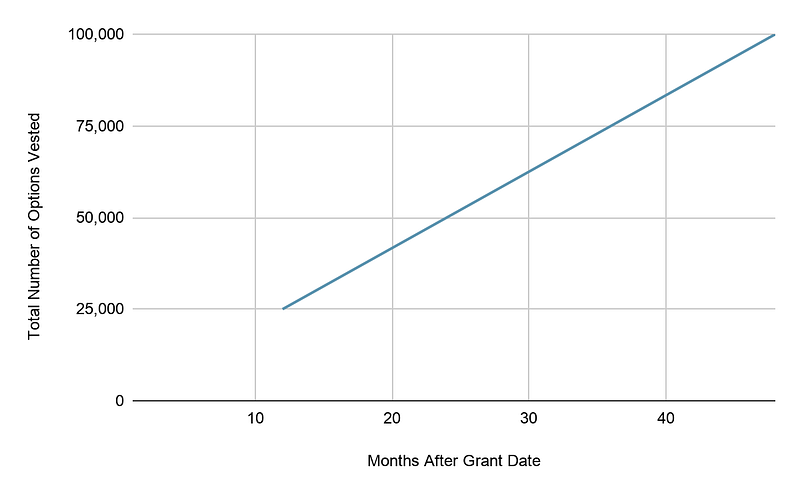

EXAMPLE #3 — The Vesting Cliff

The most common vesting schedule I’ve seen is a 48-month window with a 12-month VESTING CLIFF, and flat monthly vesting thereafter. The vesting cliff basically states if you leave before the cliff, you don’t earn into any of your options.

There are multiple reasons for this, the primary of which is as a startup, you don’t want to put all the effort into hiring and have people leaving after only a few months with small bits of vested options. Not only is it messy to handle, it also doesn’t properly align incentives between individuals and the startup.

The good news is, the clock actually starts ticking on the grant date, so as long as you stick around past 12 months, you will never know the vesting cliff even existed.

2. How they’re valued

To start, remember that with a startup, there is no premium you have to pay for the option — they’re granted over time with vesting. Therefore, the strike price is the break event point.

So if there isn’t a premium, the two numbers we actually care about are the strike price and FMV.

Calculating the Strike Price

When determining the strike price, companies typically want to make this as low as possible. The reasoning for this is because it maximizes the value to their employees and reduces the tax burden.

To illustrate this, recall our Tesla example. If you were getting the option to purchase the Tesla, would you rather the strike price be $70,000, or $10?

Yeah, I’d rather it were $10 as well, and that’s exactly why companies want the strike price to be low. For employees, it minimizes the cost of actually acquiring the asset and maximizes the potential margin when you sell the asset.

Unfortunately, there’s this thing called the IRS that wants to make sure nobody gets preferential treatment, and that everyone is paying their fair share of taxes.

The way this plays out is, assume a company arbitrarily assigns a super low value to the strike price of their options. The company grows and eventually exits through an acquisition. If the acquisition is big enough, the IRS may require an audit (again, to make sure everyone is paying the right taxes), and if they determine the strike price was too low, it can cost employees (and the company) a ton of money in taxes and fees.

Therefore, to minimize the risk of this scenario, there’s what’s called a 409a VALUATION. The 409a is an independent appraisal of a company that utilizes a number of generally accepted methods to valuing the business to assign a “per share” value to the business.

There are a handful of companies that have strong 409a reputations, such as CapShare and Carta, and are generally trusted to provide directionally correct valuations to businesses.

In going through the 409a valuation process, a company will try to help figure out the minimally defensible value of the per-share price, meaning “what is the lowest share value they can provide the business that the IRS would find acceptable in an audit?”

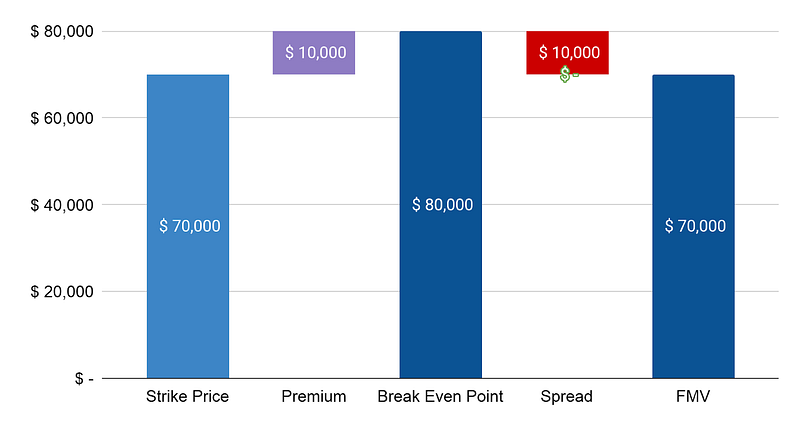

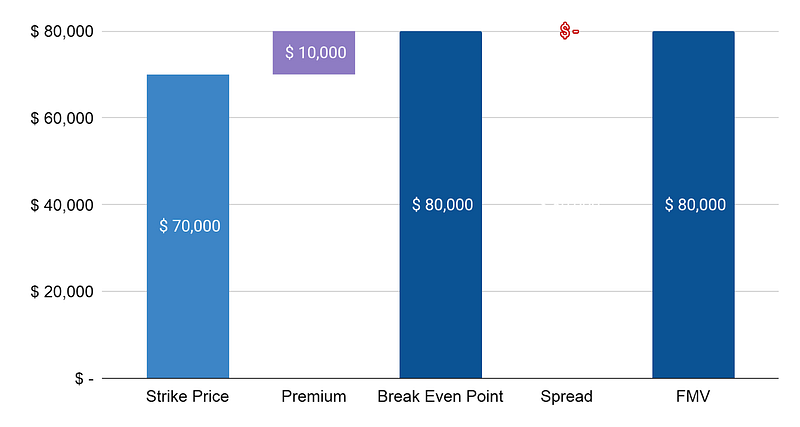

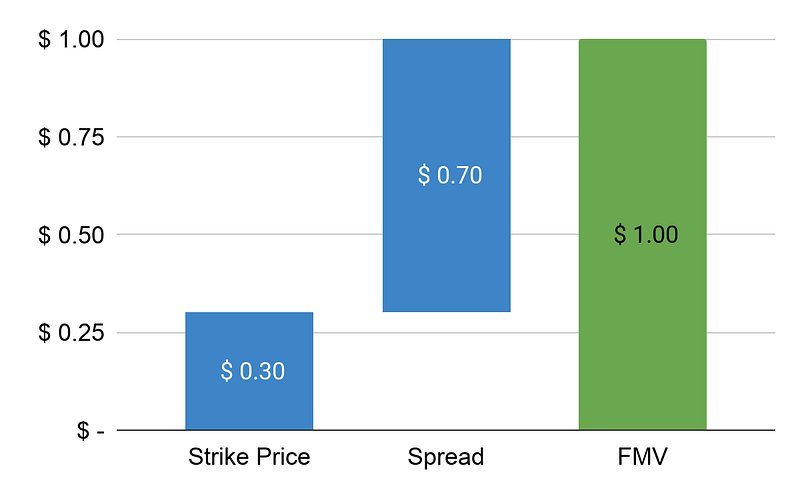

The value assigned in this process is usually used to set the strike price for an option. For our further discussion, assume the strike price of your 100k options is $0.30 per option.

There’s a lot more about 409a valuations that we could talk about, but I’ll leave that for another day. They’re fascinating! :)

Calculating FMV

With our Tesla example, there are numerous resources to help dictate the FMV of the vehicle — like Kelly Blue Book or CarGurus. When you purchase options on the market, you can use what people are willing to pay to dictate the price (the stock market has entire exchanges for this). It’s publicly available information, and the market finds equilibrium.

However, with a startup, there is no public market to set the price. There are no resources that can tell exactly what the company is valued at, thus the TLDR of this section is: at the end of the day, FMV is whatever you can sell your shares for.

That said, there are some actual values you can reference to triangulate their value.

One is the 409a per share price. But remember, the goal of the 409a is to get the lowest defensible per share price. If you’re trying to maximize your spread, then probably not the best benchmark to reference.

So for private, venture-backed companies, one of the better data points to use is the preferred share price of the latest fundraising round.

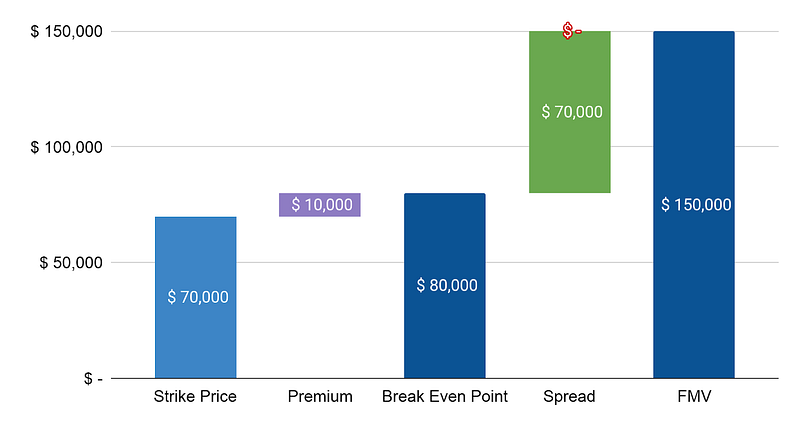

With our example, the $0.30 strike price was determined via a 409a valuation. Assume the company raised their latest round at $1.00 per share.

As you can see in the graph, since there is no premium, your break-even point is the strike price. So if the latest round raised above the strike price, your options are instantly “in the money”.

Venture-backed companies typically go through multiple rounds of financing, with (ideally) each round increasing the share price, therefore increasing the spread of your options and the value of your time-based investment.

How do I actually make money with my options?

At the end of the day, this is the main reason you get options. So let’s discuss how that actually happens.

We’ll talk about the mechanics of how you actually translate your options into cash, but then there’s also this ever-present, unavoidable tax factor you need to account for in your process. Let’s start there, as this heavily influences your strategy.

NSO’s and ISO’s

One of the first things you need to understand is stock options come in two flavors: NSO’s (Non-statutory Stock Option, a.k.a. non-qualified stock option, or NQSO) and ISO’s (Incentive Stock Option).

There are a ton of great articles on the differences (I love this one from Cooley Go) so I won’t go deep here; there are just three things I think are most important for you to know.

- ISO’s are only for employees (people who receive a W2 from a company). NSO’s can be for employees, but also anyone else (contractors, service providers, advisors, etc.).

- ISO’s have better tax treatment than NSO’s.

- If you have ISO’s, only the first $100k in exercised options per year will count as ISO’s. Anything over that will automatically be treated as NSO’s.

How do taxes work with NSO’s and ISO’s?

One of the benefits of options is that neither type are taxed when they’re granted (or when they vest). So companies can make these big option grants, and for you as the employee, you won’t pay any taxes on them until you exercise them.

There are two events you need to be mindful of with your options.

(1) When you exercise the option

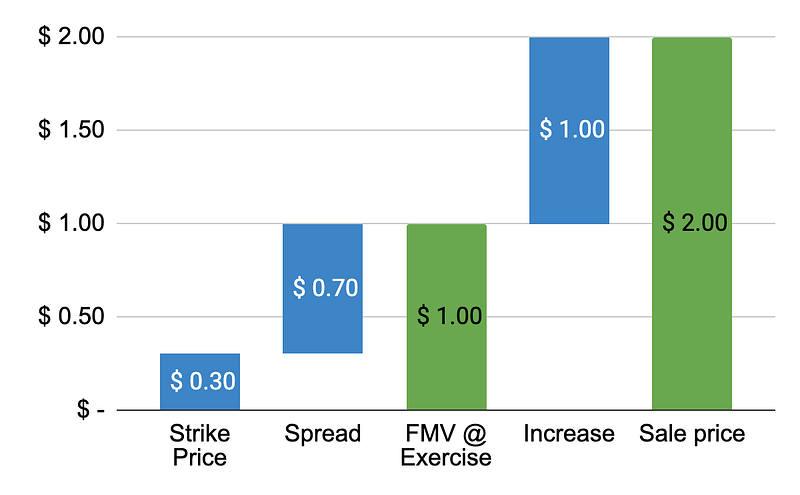

Consider the following scenario when you exercise your option, still with the 100k options from before.

Your options were granted with a $0.30 strike price per share, and when you exercise the option, the current FMV is $1.00 per share. It will cost you $30,000 to exercise your options, but the value of the shares you receive is $100,000.

If your options are ISO’s, then there is no explicit tax on this event.

I should note that the difference between FMV and the strike price is included as income in calculating your Alternative Minimum Tax (AMT), and could result in AMT taxes. This usually only applies if you’re making a ton of money. Nerdwallet has a good article on AMT if you think this could apply to you.

If your options were NSO’s, then exercising your option counts as a taxable event — the IRS sees the spread as ordinary income, and it will count on your taxes.

In this instance, with 100k options, the IRS would see $70,000 as ordinary income, and tax you accordingly.

For this reason alone, if you have the option, you should push to get ISO’s. Otherwise, if you have NSO’s, you should only plan to exercise your options when you’re in a financial position to pay the taxes on this delta.

NOTE: There’s an incentive for NSO recipients to exercise their options as soon as they receive them, to try and minimize the spread between FMV and the strike price. It’s not a bad strategy if you have a high level of confidence in the future value of the company stock. However, it can be a really expensive bet, for not only are you paying the strike price, you’re also paying taxes on a highly risky and volatile asset.

If the FMV goes down in the future, you end up paying more taxes than would have been necessary if you’d have waited. Also, if the FMV drops below the strike price, you’re underwater, and if you’d have waited — you likely wouldn’t have exercised your options at all. It’s a gamble and totally depends on your confidence in the future of the company.

2. When you sell the shares

Following your exercise of the options, suppose the share price value doubles, and you’re able to sell your shares for $2 per share. This is a taxable event.

For ISO’s, the taxes are calculated on the difference between the sale price and the strike price. In our example, this difference is $1.70 ($2.00–$0.30), and for 100k shares, would be $170,000 of taxable income.

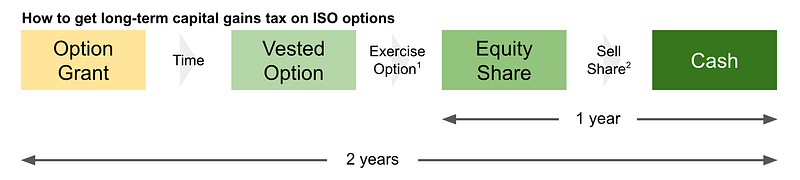

One big thing you’ll want to be aware of here is you can take advantage of long-term capital gains tax here IF

- You hold the shares for at least 1 year after you exercised your option AND

- You wait for at least 2 years after the options were granted to you

As of this writing, depending on your AGI, long-term capital gains could be 15–20%, whereas ordinary income tax could be as high as 32%.

For NSO’s, the taxes are calculated on the difference between the sale price and the FMV @ Exercise. In this instance, the difference would be $1.00 per share and $100,000 of taxable income.

Again, you could take advantage of long-term capital gains tax with NSO’s. The difference is you only have to hold the shares for at least a year after exercise — there is no grant holding period requirement.

What is this $100k ISO limit mentioned above?

The IRS only allows the first $100k worth of options vested in a calendar year to receive the ISO treatment.

You calculate the value of vested options by multiplying the number of options vested in a year by the FMV of the stock at the time the options were granted (as opposed to the current FMV of the stock when the option is exercised or whatever the current FMV is when the option vests).

For instance, suppose this time you were granted 400k options at a $0.30 strike price, and they had an FMV of $1 per share when granted with a 12-month cliff, 48-month window, and monthly vesting after the cliff.

After the cliff, you would have 100k options vest immediately. All of those options would be treated as ISO’s.

However, this is one of the potential downsides of the vesting cliff, because in the first year your cliff hits the $100k limit, and then every month of the year that continues to vest, all of those options will be treated as NSO’s for the remainder of the year.

Carta has a good article on this topic if you’re interested in learning more about it.

Why options and not RSU’s?

Sometimes I’ll hear new hires ask for RSU’s (Restricted Stock Units) instead of options, since that’s what they’re familiar with in their previous roles. This can sometimes be a tricky conversation and is one of the things I hope this article can illustrate.

It’s actually a huge benefit to both the employee to work with options instead of RSU’s and the company as well. With RSU’s, they’re typically vested, however once that vesting hits, the IRS recognizes RSU’s as ordinary income, and taxes them accordingly.

Imagine the following scenario.

Two employees start with a startup at the same time. Employee A is granted 100k in ISO options with a $0.30 strike price, and Employee B is granted 100k RSU’s. For simplicity, assume both have a 12-month cliff, a 48-month vesting window, and vest every 12 months after the cliff.

After the first 12 months, the cliff passes, both employees vest into their grants. The company has just raised money at $1 per share, providing an FMV value for the shares. Employee A vests into 25k options, and since the options are ISO’s and un-exercised, there is no tax obligation.

Employee B, however, vests into 25k RSU’s which the IRS sees as $25k of income and the employee will need to pay taxes on the shares immediately.

Over the next 36 months, every year the grant vests, Employee B will need to report the vested shares as income, and be taxed at the then-FMV of the shares. As the company continues to raise money and increase the valuation, the tax burden of the vested shares will continue to increase.

The challenge for the employee with RSU’s in this scenario is they are carrying a substantial amount of risk. They are paying taxes on an asset that has no easily accessible market to liquidate the shares. Meaning, they could pay taxes on shares over the entire 4-year vesting window, and then the company could go belly-up at the end, leaving Employee B out thousands of dollars without anything to show for it.

Employee A, however, wouldn’t have spent a dime on their shares or taxes, and the risk is very low, other than the time they invested.

In the event the company exits after both employees have fully vested, again, it’s a better scenario for Employee A. They get to follow the exercise flow we discussed previously, and depending on the timing of their exercise, may only have to pay long-term capital gains tax when they liquidate their shares.

Employee B, similar to how NSO’s work, again has to pay taxes again, this time on the appreciated value of their shares. The good news is, depending on how long they have held their shares, they may be taxed at the long-term capital gains tax rate as well.

Other things to be aware of with options

Options typically have windows within which they need to be exercised.

If you’re terminated, ISO’s typically expire the day of your termination. So if you want to exercise them, you’ll need to (a) be confident and (b) move quickly.

For ISO’s, typically they must be exercised within 3 months of when you voluntarily resign your position. However, even if you remain employed, there’s typically a window within the grant date they need to be exercised — it’s usually just a lot longer, like 6–10 years.

For NSO’s, it’s usually called out in the agreement. Typically it’s around 10 years.

In any instance, if you fail to exercise your options within the window, you forfeit your position.

Questions you should ask when receiving options

Now that you’re equipped with a foundational understanding of how options work in a startup, you should feel more confident getting into the nitty-gritty of the negotiation of your option position in the business.

To help aid your conversation, here are some questions/topics you should ask the founders about to help flush out any pertinent details.

- How many options am I receiving? What is the strike price? What is the current FMV / what share price did you raise your last round? What you’re trying to ascertain through these questions is the value of the grant you’re receiving. If you know the number of shares and their strike price, you know how much it’ll cost you to execute your fully vested grant. If you know the current FMV of the shares, you can have an idea of the current value of the grant. Use that value to determine if the options are worth it to you. NOTE: One big fallacy I see is people often ask what % of the company their grant represents. This is the wrong way to think about options. If you are getting options, you aren’t joining the company as a founder. You shouldn’t anticipate you’ll be receiving material ownership in the business. If you want to know the % of the company your grant represents, and make your decision based on that information, the % will be so small, you’re all-but-guaranteed to be disappointed. Instead, consider the total value of what you’re being offered, of what it could be worth someday, and make a decision from there.

- Is there a vesting schedule? Tell me about it. You need to understand if there is a cliff, over what period of time it should take for your options to vest, and what the vesting calendar looks like. Usually it’s monthly, but sometimes it can be quarterly or even longer. You’ll want to have an idea of what that looks like so you can help plan your participation in the company. If you get a great offer to join another team, you don’t want to leave just before an important date milestone in the vesting calendar.

- Do you anticipate raising future rounds of funding? If so, how many? With this question, you’re looking to understand how dilution will work. You’re always going to get diluted, but what you should have an idea of is exactly how much dilution the founders are planning for. Obviously plans don’t always work out, but having an idea of where things are headed should help you to understand the future value of your shares.

- What is the exit strategy? Exits typically come in two flavors — acquisition or IPO. You should understand how the founders are thinking about their exit, and over what time frame. This is critical, as this should give you an idea of what you’re signing up for. Planning for an IPO in <12 months means your options could quickly move to liquidation. It also means there probably isn’t as much upside as if they say they’re looking to sell the business in 5 years. In the first situation, you’ll have <12 months for the company to generate value, in the other, you’ll have 5+ years. It’s a bigger time investment, but it could also mean higher upside potential.

- Is there potential for secondary sales? Secondary is when people have the chance to sell personal shares of stock during rounds of financing, or to private parties. It’s a way of getting liquidation in advance of an acquisition or IPO. This isn’t always available to everyone in the business, but it’s worth checking as it could provide a chance for quicker liquidation of your shares if that’s interesting to you.

- Can I see the Stock Option Plan and a sample grant agreement? It’s not that you don’t trust all the answers they’ve provided, but it’s very possible that the founders don’t understand how their options work. So they may be giving you honest answers to the best of their knowledge, but it just isn’t right. You should trust but verify.

Have ideas of other questions you should ask when taking a new role? Let me know in the comments, I’d love to learn from your experiences and add them here.

Thanks for reading! If you have any questions or would like to hear more about something specific, feel free to leave comments below or send me a note on LinkedIn.