How Saving $20K on PMI with a Bigger Mortgage Down Payment Probably Costs You Over $250K

30Y in 30D • Y17. It’s crazy how high the actual — but avoidable — cost is of following advice from real estate pundits. Larger down payments don’t always pay off.

Related and recent articles

(Full list of “30 Years in 30 Days” Series articles at bottom of this page.) • 30Y in 30D • Y16: The Total Cost of Ownership of Your House • 30Y in 30D, Y15: Simple Question, Complex Answer — The True Purchase Price of Your Home • 30Y in 30D, Y11: Dream Home or Financial Freedom? Rethinking the True Cost of Stretching • 30Y in 30D • Year 3: Early Extra Payments Are Magical • Kickstarting “30 Years in 30 Days” — Decades of Mortgage Wisdom in 1 Month • Has U.S. Healthcare Really Become a Mob Protection Racket?

(Subscribe to receive email notifications when I post new articles in this series and on other topics.)

I had a late night phone call a couple weeks ago with a friend that I’ve known forever.

My friend bought a house recently on the East Coast — his first one — and he was catching me up on how his first year of living there has gone.

One of the things he mentioned was that he had made a larger than planned down payment on the house of 20% in order to not have to purchase PMI (private mortgage insurance.) Everyone had advised him to do this if he could swing the extra down payment, and he felt as though he had made a savvy move in following their advice.

After we got off the phone, I thought more about what he had told me.

First off, pundits always, always, always recommend making a 20% down payment as a savvy financial thing to do if you have the money to do it. So my friend getting that advice — and then following it — wasn’t a big surprise.

But I kept wondering whether anyone had actually run the numbers in a thoughtful, “what-if” kind of way to see if it really did make sense.

And yes, even though this advice is so well-accepted that it’s considered common wisdom, I was still questioning whether anyone had ever actually run the numbers from the homebuyer’s perspective.

Not to give the game away here, but when I ran the numbers, I was shocked.

And yeah, the pundits sure as hell seem to be wrong on their “common wisdom” about how it’s clearly a savvy move to make a bigger downpayment in order to eliminate the need for PMI.

They aren’t just wrong — they are breathtakingly wrong.

Our starting point

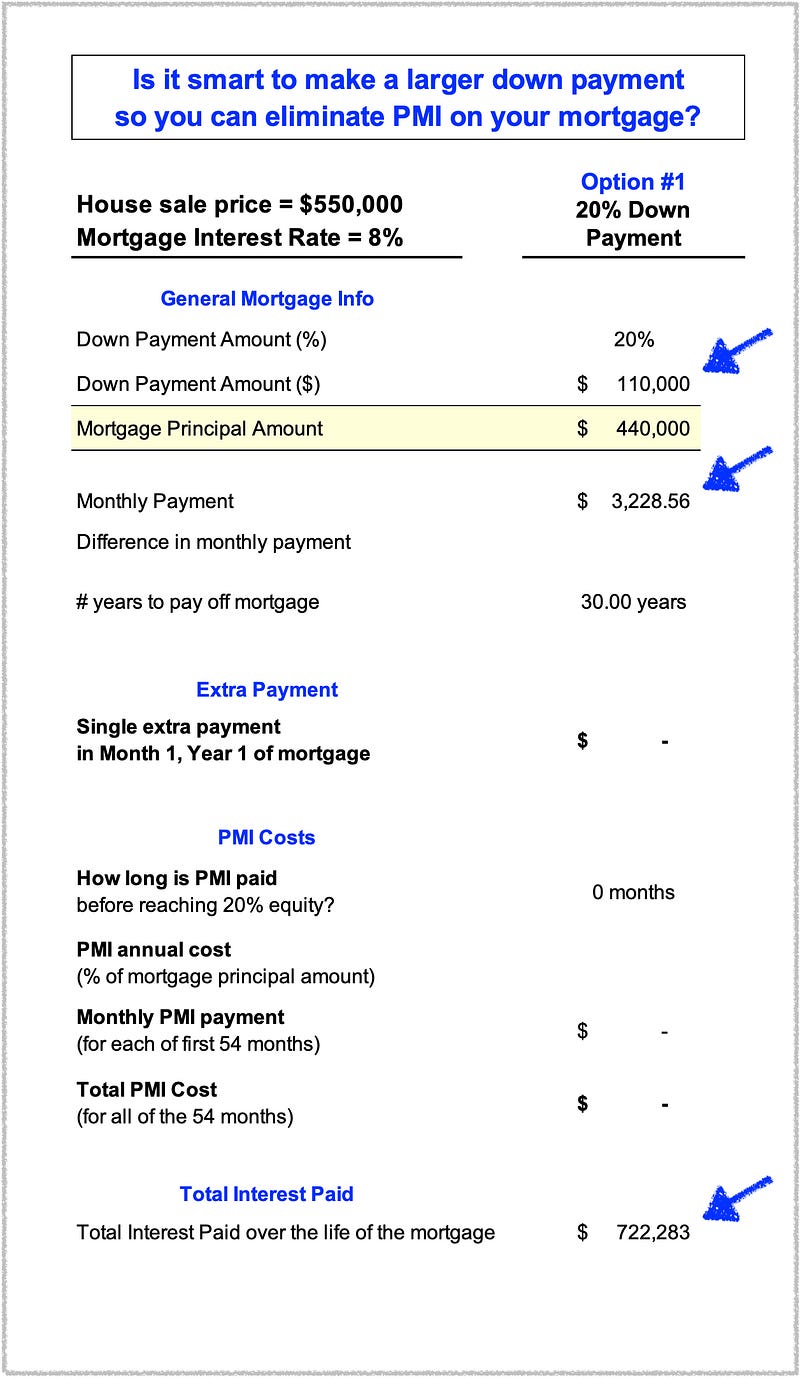

Here’s the base case situation I’m using today:

- $550,000 house

- 8.00% fixed mortgage rate

- 30-year mortgage

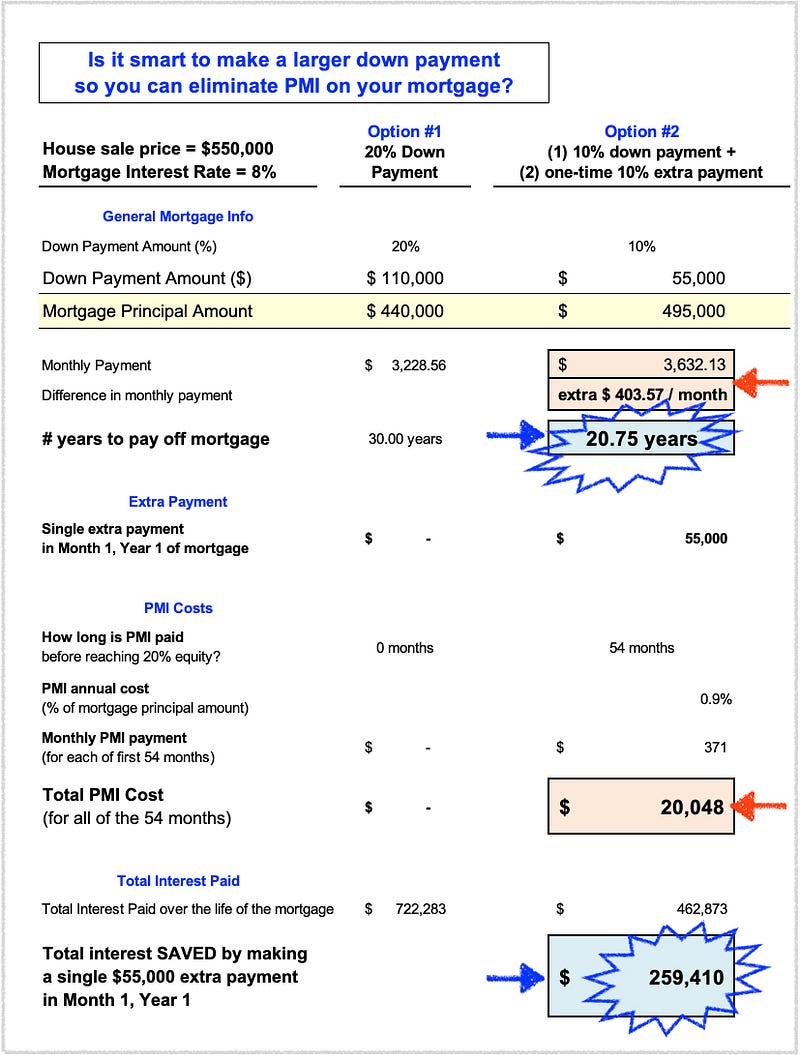

- 10% down payment of $55,000.

- Monthly payment = $3,229.

- PMI annual cost of 0.9% of mortgage principal

- The home buyer will pay PMI of $450 per month for the first four years and six months until equity in the home equals 20%. total amount paid for PMI during this for years and six months will equal about $20,000.

And the homebuyer DOES have an extra $55,000 that he could use to increase his 10% down payment up to $110,000, thereby eliminating the need for PMI.

But he is wondering whether that is actually the smart move.

We have two options for what we might do with an *extra* $55,000 in the bank.

Option 1

Add an extra 10% ($55,000) to our already-planned 10% down payment giving us a total down payment of 20% or $110,000 on our $550,000 house.

This eliminates the need for any PMI payments since the equity level in the house would be 20% from the start. And that means the PMI expense for this house purchase is zero.

Option 2

Stay with the original 10% down payment, but use that extra $55,000 to make one single “monster-sized” extra payment of $55,000 in addition to our first regular monthly mortgage payment in Year 1, Month 1.

This means we *will* have to pay PMI for the first 54 months. That’s how long it takes before we work our way up to 20% equity in the house, and that is the point at which PMI stops being a requirement.

Now let’s do what the pundits NEVER do . . . and actually work through a few numbers to see if the “common wisdom” is actually, well, wise or not.

Option 1. Paying an extra 10% with the down payment — for a total of 20% down payment — so that we don’t have to pay any PMI

Focus on these numbers for now:

- The total down payment amount, which is $110,000.

- The total monthly payment in this case, which is $3,229.

- The Total Interest Paid, which is $722,283.

Nothing complicated so far.

Now let’s add a column for Option 2.

Remember that Option 2 is where we take that extra 10% or $55,000 and instead of using it for additional down payment to eliminate PMI, we just make one monster-sized “extra payment” of $55,000 along with our very first monthly mortgage payment in Year 1, Month 1.

And this is where we are going to see some amazing magic happen for our future bank account balances.

Option 2. Use that extra 10% ($55,000) to mail in a monster-sized extra payment with your first regular monthly mortgage payment.

Quick summary — 4 things to focus on

Let’s start with the positive, actually kind of amazing things that come from taking that extra $55,000 and just making a single monster-sized “extra payment” at the start of the mortgage INSTEAD of using it to get to a 20% down payment.

#1. HUGE Win. Total Interest Saved = $259,410

In the first case earlier where you took the $55,000 and used it to get to a 20% down payment (to eliminate the need for PMI), you were going to pay $722,283 over the life of the mortgage.

By instead using the $55,000 to make a single, one-time extra payment right in Month 1 of Year 1 of your mortgage repayment, you slash your Total Interest Paid over the life of the mortgage all the way down to $462,873. Total interest saved = $259,410. See: “30 Years in 30 Days • Day 1: Starting Strong on the Mortgage Journey” and “30 Years in 30 Days • Year 3: Early Extra Payments Are Magical” for more info.

#2. HUGE Win. Mortgage gets paid off in 20.75 years, not 30 years.

That $55,000 one-time extra payment not only slashes your Total Interest Paid amount down by more than a quarter-million dollars, it also cuts your time to fully pay off your mortgage by over 30%.

You will no longer be paying your mortgage for 30 years — you’ll be done in 20 years and 9 months. See: “30 Years in 30 Days • Year 4: Accelerate Payoff Via Extra Monthly Payments” for more info.

Ok, but what about the costs or downsides? There HAS to be some catch, right?

Sort of. There are indeed 2 costs — details below — but in my opinion, they are relatively small; probably manageable for most people. And if you can handle them, (1) you stand to get a giant-sized return for these small “investments,” and (2) you have $240,000 more in your bank account at the end of the 20 years and 9 months than you were going to have back in Option 1 where you did the “smart” (but not smart) thing of avoiding PMI.

#3. Small-to-medium cost. Your monthly mortgage payment increases by about $400 per month, going from $3,229 to $3,632.

That works out to a 12.5% increase on your monthly payment. Not tiny, but not huge, either.

And this is because you are now “only” making a 10% down payment of $55,000 instead of the 20% down payment we were assuming in Option 1 in the above spreadsheet table.

To be fair, when you factor in the other costs of the house, though — like property taxes, utilities, home maintenance & repairs, HOA dues, furnishing & decorations, landscaping/gardening, and a home-specific emergency fund — the earlier 12.5% estimate for the monthly payment increase drops down to probably somewhere in the 5–7% range.

#4. Small-to-medium cost. You will also have to make PMI payments for the first 54 months (4 years, 6 months) of your 30-year mortgage.

The monthly PMI cost will be $371, and the total amount paid over those 54 months will be $20,048.

This extra $371 payment for PMI amounts to about 11.5% of the $3,229 original monthly payment in Option 1.

Keep in mind, though, that this PMI payment happens only for the first 4 years and 6 months. After that, it goes away.

Discussion and Takeaways

- When we net out the $20K cost of PMI and the $259K gain due to savings on Total Interest Paid, you get a $239K gain in terms of how much money you can have left in YOUR bank account at the end of the mortgage. This is $239K that won’t have gone to your mortgage lender or to whatever investor owns your mortgage. It won’t go to paying quarterly investment banker bonuses. It won’t go toward paying Jamie Dimon’s annual bonus at JP Morgan Chase. It will stay in your bank account where it can be part of your retirement money or your kids’ college fund or whatever you want to use it for.

- I think the upsides of (1) the $239K extra in your bank account at the end of the mortgage and (2) paying your mortgage off in less than 21 years instead of the original 30 years MORE THAN justify the extra costs, but that is a decision you’ll have to make for yourself in terms of the tradeoff. As noted above, on top of the original $3,229 monthly mortgage payment, you will have to pay (1) $775 extra each month ($371 PMI + $404 due to lower down payment amount) for the first 4 years and 6 months and then (2) just an extra $404 each month for the remainder of the mortgage once you are done paying PMI.

- Kind of wild isn’t it? The pundits have you focused on saving what would in this case be $20,000 but are either too incompetent, too dumb, or too dishonest/self-interested to mention to you that you’re missing out on a chance to instead save $239,000. They. never. even. mention. it.

Comments? Thoughts?

I would love to hear your feedback on this article.

Is this indeed a doable way for most people to claw back at least $100K or $200K by being more strategically smart about their mortgage?

Thank you for reading, subscribing, clapping, and sharing — I appreciate your time and attention.

Related and recent articles

• 30Y in 30D, Y16: The Total Cost of Ownership of Your House • 30Y in 30D, Y15: Simple Question, Complex Answer — The True Purchase Price of Your Home • 30Y in 30D, Y14: What Kind of People Are Getting Loans for Houses Right Now? • 30Y in 30D, Y13: What Does It Take to Pay Off a 30-Year Mortgage in 15 Years? • 30Y in 30D, Year 12: CBS News’ Version of (Not) Helping You Save on Mortgage Interest • 30Y in 30D, Year 11: Dream Home or Financial Freedom? Rethinking the True Cost of Stretching • 30Y in 30D • Year 10: A Tale of Two Eras — Home Buying in 1972 and 2023 • 30Y in 30D • Year 9: Visualizing Savings — Mortgage Charts that Matter • 30Y in 30D • Year 8: The Mechanics of Mortgage Interest — What Really Matters • 30Y in 30D • Year 7: The Big Payoff of Early Extra Payments • 30Y in 30D • Year 6: Mortgage Power Play with a Single $100 Extra Payment • 30Y in 30D • Year 5: Are Car Buyers Smarter than Homebuyers? • 30Y in 30D • Year 4: Accelerate Payoff Via Extra Monthly Payments • 30Y in 30D • Year 3: Early Extra Payments Are Magical • 30Y in 30D • Year 2: Rapid Progress on the 30-Year Mortgage •30Y in 30D • Year 1: Starting Strong on the Mortgage Journey • Kickstarting “30 Years in 30 Days” — Decades of Mortgage Wisdom in 1 Month • A Friend Texted to Ask “Who I Favored” for 2024 but Hated My Answer • Has U.S. Healthcare Really Become a Mob Protection Racket?

(Subscribe to receive email notifications when I post new articles in this series and on other topics.)