How I Prevent Inflation from Pummeling Me

Every penny matters in the long run. Here’s how I’m fighting back against inflation.

The most recent CPI report from July 13th, 2022 places inflation at a staggering 9.1% year-over-year. Despite a positive job report outlook, it appears we are still not over the worst of the inflation spike this year. Another 75-basis point hike by the fed later this month is looking inevitable.

Even more unfortunate is that food and energy are the two leading categories in the inflation spike this year.

We all need to eat and consume energy for our homes and vehicles–it’s all part of everyday life, and it can be harder to make drastic cuts in those essential categories.

Where inflation hurts the most

When inflation is out of control, we all feel the pinch. The greatest pain point is felt when holding cash in savings and when buying things we need, like food and gas.

I’m as guilty as the next person for letting inflation creep up on me. I set price anchors in my mind about what something should cost.

In my mind, gas should cost $2.25 or less a gallon, that’s what I was paying during the pandemic.

In my mind, a gallon of milk should be about three bucks.

In my mind, a pound of chicken breasts should be $3–4.

Imagine my surprise at the pump or in the checkout lane when real prices have blown past the price anchor points set in my head. That costs HOW much?!

All that cash I have squirreled away in my rainy day/emergency expense fund starts looking a lot less significant when I check my account balance.

The safety and comfort of having an emergency rainy day fund are crucial for me and my family. It means that during a period of hardship, I won’t have to dip into my investment accounts and sell holdings that I want to keep for years to come.

Having some cash on hand also means I can be better positioned to invest on the fly if I identify a good investment opportunity that I want to take part in. Regular, consistent investments matter, but being able to dig in and add a little extra over my typical monthly investments has made a big difference in my investing so far.

There are clear advantages to having cash on hand, yet inflation is always threatening to reduce the spending power of my cash. What do you do when it feels like there is nowhere safe to park your capital?

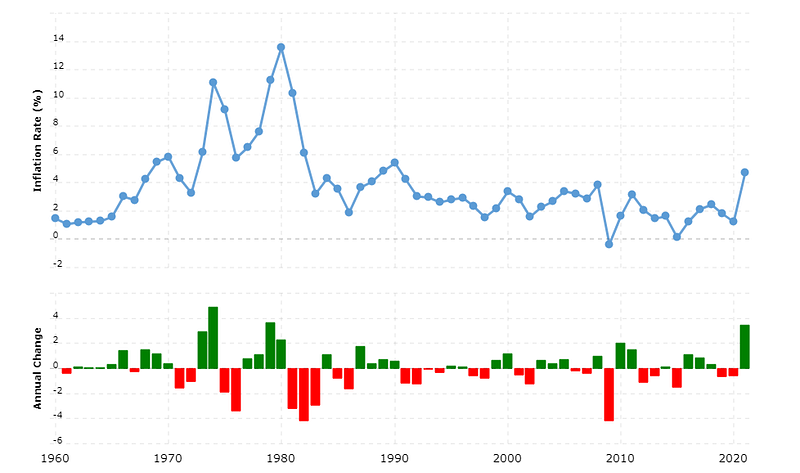

“The Federal Reserve has not established a formal inflation target, but policymakers generally believe that an acceptable inflation rate is around 2 percent or a bit below.” Source.

What is ‘acceptable’ is far from the harsh reality we face today.

This graph does not include 2022. When it does, we’ll see another drastic spike similar to what occurred in the 70’s and 80’s. A painful momento of how absurd some prices have become this year.

How I’m easing the pain of inflation

Dividends help. The S&P 500 has averaged a 6.08% yearly increase in dividend payouts since 1989, even including major financial catastrophes like the dot-com bubble and 2008 financial crises. In 2022, dividend payments for the S&P 500 are up almost 11%.

Qualified dividends (those paid out by eligible firms in the US that are not REITs) are also subject to lower, more favorable taxation rates for individuals than ordinary income.

One of the only drawbacks to dividend income is that it takes a lot of capital to build up–capital that may be better put toward growth-oriented stocks and funds that target capital appreciation over a longer investing time horizon.

While my dividends are not all qualified, I’m still earning almost $2,000 of extra income a year just from the stocks in my brokerage account that pay dividends. With inflation at almost 10%, every bit helps. I currently reinvest all of my dividends back into my portfolio.

Like many other real assets, real estate is also an awesome hedge against inflation and stock market downturns. Until I’m ready to buy my first physical real estate investment property, I invest in real estate with Fundrise.

In general, the more income I’m earning, the less inflation hurts me in my day-to-day, so long as I can also avoid lifestyle inflation to the best of my ability.

I’m always working toward increasing my market value, working hard to perform well at work, hustling on the side, and saving and investing more money.

Inflation pummels those who hold cash in traditional bank accounts while the same banks that tell us “investing is risky” invest our money and lend it out to other people for much greater returns than the interest rates they pay us. It’s the reality of the situation, and the reason why we can get great banking services for “free” and not have to pay any monthly fees to own an account. In this case, I want to identify some ways to perform damage control on my emergency rainy day fund and minimize the impact of inflation.

Tried-and-true personal finance wisdom tells us that we should keep anywhere between 3–6 months of our non-discretionary expenses on hand in the case of a rainy day.

If I can reduce my monthly expenses for essentials, that means I will need to keep less cash on hand that is exposed to inflation.

If my essential monthly expenses are $4,000, on the high end I would want to have $24,000 saved in cash. At a 9.1% inflation rate, that $24,000 sitting in a 0% APY bank account for a year will only have the spending power of $21,816 in today’s dollars. Inflation effectively took away $2,184 dollars from me in this model.

If my essential monthly expenses are $2,000, on the high end I would want to have $12,000 saved in cash. At a 9.1% inflation rate, that $12,000 sitting in a 0% APY bank account for a year will only have the spending power of $10,908 in today’s dollars. Inflation took away $1,092 dollars from me in this model.

Cut spending = cutting how much cash to keep on hand = less spending power lost from holding cash, even if the overall percentage is the sam

CDs offer upwards of 2% returns (at zero risk) at terms as low as one year. Meanwhile, I could comfortably invest in the total bond market index (BND) and cash in a roughly 3% annual yield and still be able to cash out my investment at any time–for the additional cost of having some risk exposure than a zero-risk bank account.

For my age and risk tolerance, I have yet to invest in a CD versus just keeping cash on hand or increasing my investments into my brokerage account once my tax-advantaged accounts have been maxed out for the year. Right now, CDs just don’t fit into my investment strategy.

Banking matters.

I ditched my old-school credit union as my primary checking and savings account provider since I wasn’t using the vast majority of the services offered in their brick-and-mortar locations.

A lot of savings accounts with ‘digital’ banking experiences offer variable interest. The higher interest rates are in general, the more APY they’ll pay on my savings balance.

Currently, I’m earning 1.5% APY on my FDIC-insured savings and checking account balances with SOFI. It’s nowhere near enough to overcome the impact of inflation right now, but any extra interest income from cash I need to keep on hand for financial security and peace of mind is a huge benefit. $24,000 in cash will generate an additional $360 of interest income per year at current rates.

I also enjoy earning the same APY on my checking account balance with SOFI. While I usually try to keep my checking balance just high enough to cover my planned and budgeted expenses, it’s a little extra money in my pocket every year from funds that typically wouldn’t earn anything.

Another great FDIC-insured savings account is Current. Current pays out 4% APY on up to $6,000 of balance. I don’t mind having an extra savings account when it means I can earn 4% on that portion of my emergency rainy day fund. 4% is more than enough to top inflation most years. $6,000 at 4% APY equates to an additional $240 of passive interest income for zero work other than spending five minutes setting up an account. Current doesn’t pay any interest on balances above $6,000 so once a month I’ll remove my excess funds and put them to work elsewhere.

I wrote an entire article on how I’m responsibly using my credit card to earn extra ‘income’ every year. with rewards between 1–4% and many great benefits, putting all my expenses on my credit card and always paying my full monthly balance is another way I can keep mitigating inflation’s impact.

Rampant inflation sucks, but I hope this article illustrated some easy things I do to reduce its impact and keep it from pummeling me and the cash I keep on hand.

Join me on my path to financial independence

I hope you’ll join me on my journey to Financial Independence. Sign up for a free account right here to follow my story.

You can also connect with me on Twitter or LinkedIn, I’d love to hear from you!

Subscribe to DDIntel Here.

Join our network here: https://datadriveninvestor.com/collaborate