How does the stock price of an energy company relate to its commodity prices?

This article discusses the Chevron Company and Oil as a commodity financially. Other topics such as a brief history of both the company and the product are also addressed. Financial trends are followed numerically in parallel with events in the company’s history as well as in world’s history. Stock and Commodity prices follow bullish and bearish trends that vary with factors that are discussed in this article. In short, this is an overview of the Financials of Energy Company and of a commodity such as oil. This article is financial in nature, thus centered on the numerical performance of the company as measured through stock and commodity prices while other scientific contributions are overlooked. This article does not go in depth in paleontology, geology, and different types of engineering such as petroleum and mining.

Even though this article’s focus revolves around one Energy Company and its most essential commodity, it’s important to note the importance of the subject and denote the frame, which this really comes from. By putting things in context, we realize that when we talk about Finance, we are not merely talking about money but the relocation of resources, the creation of value and the realization of society through the market of what it’s worth.

Energy Companies are among the pillars of modern society. Since the invention of fire, the use of combustion, ignition, and electrochemistry of fuels has been essential for human survival and development. Community and the Market reflect the worth of all the value created through continues bullish trends for both commodities that are used for most of our daily needs, as for Energy Companies that are the creators of such.

Chevron is one of the biggest Energy Companies in the world, with business in multiple commodities. Because of this, Chevron was chosen for the article, as well as for personal interest in the company. In this article, oil will be discussed, as it is Chevron’s most crucial commodity and also 21st society’s most important fuel. The company’s value as reflected by stock prices will also be discussed. All topics will be revised under the financial point of view.

Chevron’s origins date from the times of the black gold rush in California. Chevron’s eldest predecessor, the Pacific Coast Oil Co. was founded in 1879 (1). The Pacific Coast Oil Co. had California’s largest and most modern refinery at the time (1). Almost parallel to such foundation, the Standard Oil Company was starting to come into the region under the subsidiary Iowa Standard, as a significant player since their financial parent firm in New York was leveraging them (1). Standard Oil Co. eventually acquired the Pacific Coast Oil Co. in 1910 and started numerous pipelines, refineries and exploration projects in the region (1). In 1911 the Standard Oil Co. was forced to be separated from its parent firm in New York by a Supreme Court decision (1).

Standard Oil Co. California was one of the most important suppliers for the US Army in times of WWII. After the war, the company started exploring offshores (1). After several years the company gained their first contract in the Middle East in 1928, a region that at the time had “ no obvious petroleum prospects,”(1). It was, however, in 1932 when the company made its significant discovery in the Middle East when finding oil fields in Saudi Arabia through its subsidiary, California Arabian Standard Oil Co (1). The company continued with explorations and discoveries in Louisiana and other areas of the U.S. to later expand its operations worldwide under the joint venture with Texaco name of Caltex (1).

In 1941 the company seemed to be having great success becoming the first oil producer in California and the third in the U.S. (1). The company continued making important discoveries through the ’50s, ’60s, and ’70s in South East Asia, Canada and Venezuela (1). In the ’70s after political disruption towards oil companies, the company decided to change its public name to Chevron as it had already sold products with this name during the thirties (1).

By the beginning of the 21st century, Standard Oil Company of California was one of the United States’ most important corporations, owning 50 refineries, and having the capability of producing about three million barrels of oil per day (1). By this point in time, the company had numerous projects worldwide (1). In the ’80s Standard Oil Company merged with Gulf Oil Corp, doubling its worldwide proved oil and gas reserves overnight (1). With the merger, the company utilized the Chevron name for all of its operations (1). In 2001 Texaco merged with Chevron to become the second largest U.S. based Energy Company (1). From 2002 to 2007, Chevron earned close to $ 72 billion and had 42% success in exploration (1). Chevron is currently investing in Alternative Energy sources, for future development even though Oil continues to be the most critical source of fuel (1).

Petroleum has its origins from organisms that died million years ago and which fossils were buried under sediment under the sea in anoxic conditions (2). These sedimentary materials, such as fossils and other minerals mix and get trapped by rock caps such as marble or granite or salt domes in the different type of faults (2).

Oil exploration started in China in 347 A.D. (3). Other Oil wells were developed in Persia and France in the sixteenth century, at this point in time oil was only used for heat and lightning (3). In the nineteenth century, the first modern oil well was created, as well as the distillation of oil (3). The demand for oil was not bullish until the creation of other inventions, such as the light bulb in 1878 by Thomas Alba Edison, or the utilization of oil in steam engines for transportation in 1885 and 1886 (3). From that point in time forward, our civilization entered what some scholars know as the Age of Petroleum, where we depend on the fuel, almost entirely for our survival. Such worth has been recognized by society in the stock and commodity markets and is the driver of technologies that are used for oil exploration, such as the development of 3-D geological maps.

Chevron is one of the biggest corporations in the United States, so trends in the market will also be clear trends in the stock price. There are numerous speculations and ideas about Energy Companies that will not be discussed in this article. In this article, we’ll stick to facts, events, and numbers.

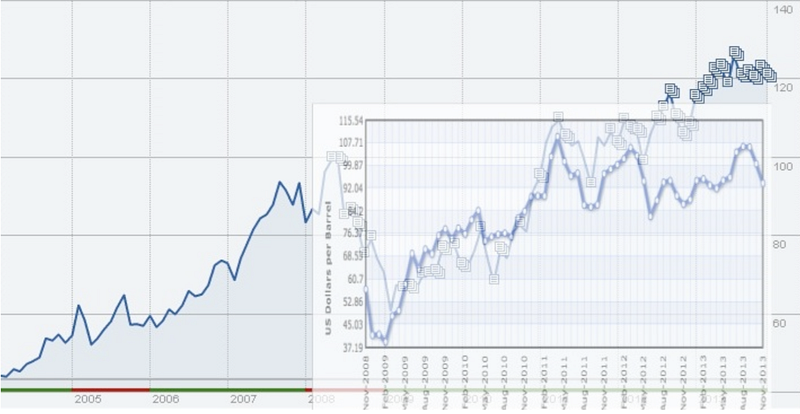

The following graph, taken from the New York Times Website, shows Chevron’s performance for the last five years.

Chevron is a huge multinational company, so it’s hard to denote which events will determine its stock price, but there are definitely some that stand out. In 2008, President Chavez from Venezuela threatened with taking assets from the company, and while Chevron responded logically by taking legal action, this uncertainty was bearish for the stock price of the company (4).

Historically, Chevron has had many subsidiaries worldwide that deal with oil extraction and exploration, and the risk of losing one in Venezuela had the investors anxious about the company. News like this, adding to increasing bad publicity to Energy companies due to climate change and “big oil,” are probably some of the reason why there is a small drop before a spike in 2008.

In the same year, the war in Iraq had already settled down much more, and the Iraqi government was opening for oil concessions to foreign companies. Chevron was among the companies with which the Iraqi government was willing to have contracts for oil exploration and extraction (5). Nevertheless, these contracts never took place because they set the Iraqi government in a very negative public light that at the time could not handle, so they were withdrawn. All of these events explain why even when the company seemed to be heading in the right direction at the beginning of the year there was a sudden massive spike in stock prices.

It is also true that almost parallel to such adverse events the U.S. economy entered a recession, which made things a lot harder and slower for the company. In fact, 2009 was the year when the company reached bottom relative to what the average performance has been in the last five years. In this year the company was struggling with assets in Ecuador, and low margins resulting in small profits. (6) The company was under such pressure from the market with low prices that they were in need of a change. The situation was so harsh that the CEO of the company stepped down and was preceded by former Vice Chairman Mr. Watson (6).

2010 was a financial rollercoaster ride for both the company and the world economy. Because of the crisis in Europe, stock prices were plumbing down worldwide; Chevron was no exception to this (7). The company’s stock went down 1.1% of its value in one single day (7). Nevertheless, there was also good news out there that made the year have its temporary green numbers. Published news such as the signing of oil contracts in Venezuela was beneficial for the company (8). Chevron was the big player in the settlements and even though Venezuela continued to be one of the riskiest for investment its potential for immense oil reserves made it a desirable asset for investors (8).

Even though there was some tough news for Chevron Corporation in 2011, the company pulled through and had a good year, reflected in the stock market price. Chevron was found liable for numerous pollution concerns in Latin America, the biggest one being in Ecuador, where the company had to pay a large sum of money (9). Chevron would have to spend nine billion dollars to Ecuador as a result of the pollution caused by its operations in the area (9). Due to unrest in the Middle East and Africa, with an increase in demand from BRIC (Brazil, Russia, India, and China) nations the company performed well (10). Chevron had first-quarter net income of 6.21 billion USD while the price of a barrel of oil rose to about a 100 USD (10). Even though some analysts and investors expected higher returns, 2011 was a good year when taking into account that the stock price followed a bullish trend despite negative news regarding pollution and lobbying.

Chevron Corporation made some big moves on 2012. Chevron decided to acquire assets from Chesapeake Energy in the Marcellus shale (11). The corporation decided to take a turn for the best by focusing on natural gas and acquiring assets all over Europe and North America. Buying assets in North America from Chesapeake was more of a strategic move for Chevron since it was not the only buyer of the assets (11). Because Natural Gas has been in the climb and its positive image to the public, while still being profitable Chevron’s operations and stock prices rose in 2012. However, in Europe Chevron was a more significant player and took on more risk when buying natural gas assets in Lithuania (12). The corporation already had operations in other eastern European countries, but acquiring exploration rights in Lithuania was a big move for their Europe operations. Because of such good business decisions, the stock price kept bullish through the year, having only one drop, which was more related to the economic crisis in Spain than to the company.

Concerns for climate change have been growing, and pressure over congress members has reached the point where some action needs to be taken. Even though Chevron and other big oil companies have been financing the Republican Party, the time for a carbon tax seems to be around the corner due to public pressure (13). Big oil companies, including Chevron, have had a bullish trend in their stock prices as well as positive profits, but the time has come for more regulation and taxation due to increasing environmental concerns (13). Nevertheless, Chevron seems to be in a good position for taking on the rules due to substantial investment in other assets, which are appeared as more positive by the public, such as investment in alternative energies. Chevron has invested heavily in other resources, even though crude remains its most important commodity, such as natural gas all over the world (14). Natural gas is seen under a positive light by environmentalists and would be affected less by a carbon tax since it has a lower carbon content than crude; therefore the corporation has prepared well, but as always the market is unpredictable and only supply and demand will end up determining the company’s worth.

Oil is one of the most essential commodities traded daily. It is also the most critical commodity of Chevron Corporation. Oil is used as security for times of uncertainty when bought as for an asset itself from which many products from modern living can be extracted including aspirin. Oil prices are tracked under two big general groups, Brent and West Texas Intermediate (WTI), for Chevron we’ll use WTI since its more relevant as an American Corporation.

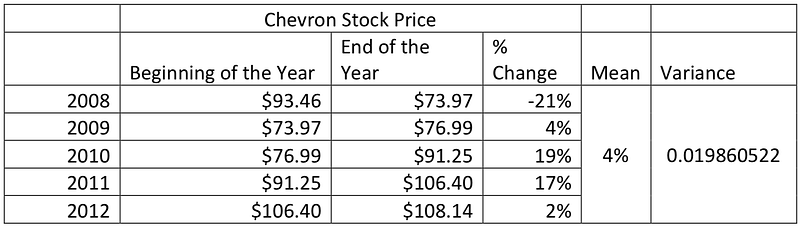

The following graph is taken from index Mundi website the price at which oil (WTI) as a commodity has been traded, displaying its worth to society as reflected in the market in the last five years.

Oil prices had been escalating up until 2008; even after the housing market crashed, the bullish trend continued (16). However, bright analyst expected the bust, which is the first trend we see in the five-year graph to happen due to almost manipulated prices (16). The amount had been managed in the sense that even when demand kept growing in BRIC countries supply was controlled by governments like Venezuela, Russia, and organizations like OPEC (16). On top of that, the uncertainty created by a mediocre economic performance in the US and Europe drove the price down. As predicted, the cost of the commodity plumed from a peak at 138 USD to about 37 USD (16).

Even though oil (WTI) prices hit rock bottom in early 2009, the trend quickly changed to a very bullish one. The fact is that such low oil prices where almost as fake as the record high levels because the commodity is highly needed and demanded in our modern world, and as a fossil fuel its supply is limited. In mid-2009 the prices had already doubled from what they were at the beginning of the year, but the analyst expected a continued increase (17). Oil prices escalated so quickly in 2009 due to inelasticity of the resource and the pushing economies of developing nations such as China (17). This is the year that oil proved to be a needed commodity in the market when even with low demand and high supply prices kept escalating (17).

The 2010 BP oil spill hit the industry very hard and made Energy companies seem almost evil to the public eye due to inaccurate media coverage (18). The market’s almost flat oil price curve displayed how the negative the public was reacting to the incident and how uncertain investors were of the future in the industry (18). In fact, the only reason for the price of oil to be flat and not escalate in 2010 was speculation as the US economy kept recovering and developing nations kept demanding more of the fuel (18). Overreaction to the spill led speculators, which are most of the market, to hold back on oil investment even though there was a massive need for the resource both in the US as overseas (18).

The market proved to rely on basic economics again in 2011 when supply and demand of the resource ended up determining the price for the commodity. With a recovering US economy, the need kept growing and making the price continue a bullish trend, even reaching a new peak. Oil producers got too ambitious with the bullish market and started producing so much that the cost of the resource actually experienced a fall. The United States began to provide so much oil that its exports kept increasing over the year (19). With an increasing supply, applying basic economics, the price was brought back down to 2010 levels (19).

2012 followed a very similar trend to that of 2011. Again the price was kept at relatively high levels due to the inelasticity of the resource and the increasing demands with a recovering US economy and stable developing markets. The news received in this year was however of more effect to the industry than that of previous years. In November of this year, an article was released that expected the United States to become energy independent in the next 10 years and the largest oil producer in the world by 2020 (20). Being such a significant oil producer meant, huge supplies and as basic economics and the speculative market shows us, lower prices creating a flat net change through the year.

The United States has been investing heavily in infrastructure in the past five years as a way to prepare for the future and impulse the economy. All the built and reversed pipelines, as well as an increase in exploration and reserves, has set the country to be an oil giant in the coming years (21). The rise in oil producing capacity and the increase of Energy source diversity has led the company to increase supply and also negotiation power tremendously. (21) This has translated to more stable lower oil prices, which cannot be as easily manipulated as they were before by Russia, Venezuela or OPEC. In fact, falling oil prices are becoming a concern for countries in Africa and the Middle East, which are under unrest and are in need of the money.

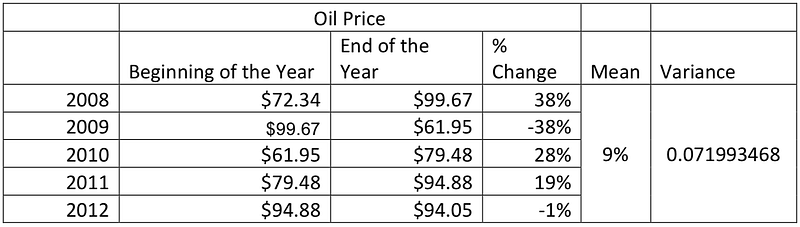

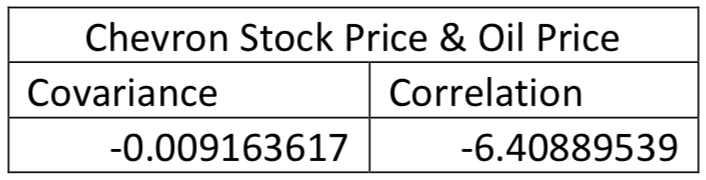

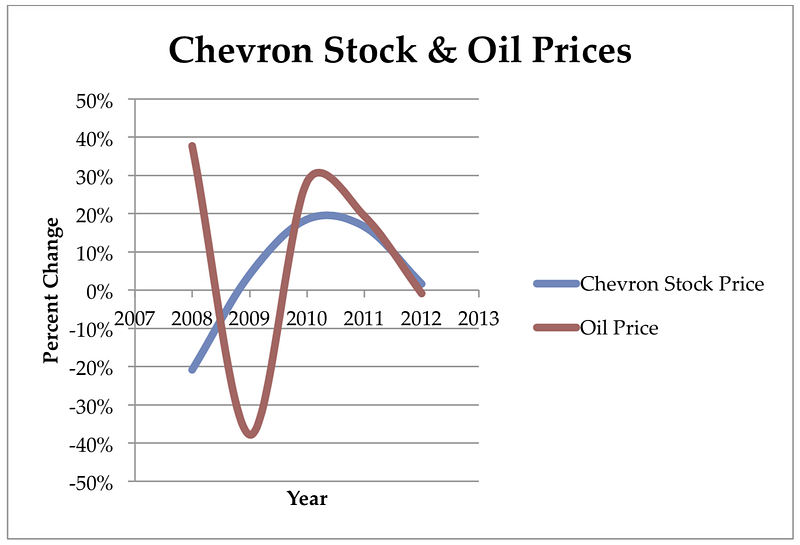

Chevron is one of the biggest Energy companies in the World and its primary assets and products revolve around petroleum and the oil industry. Because of such a close relationship between the company and the commodity, it would be expected that the correlation and covariance between both are really tight, almost the same. The fact is that when we just overlook the trends of both the commodity and the company’s stock rapidly and transpose them, they seem to match and be the same, as seen in the next figure. This, however, might be misleading since the scales are not the same.

However, as suspected, transposing both graphs is misleading and does not yield accurate and precise comparisons. When calculating the percent change of both the company’s stock prices and oil prices for each year we are able to compare them better. Using the percent change to compare with the use of statistical tools the relation seems actually inverse, which means in fact that at least throughout five years there is no relationship between stock and commodity prices because the number is so small. Calculations are shown in the next tables.

When graphing the data calculated in the previous tables, it becomes more evident that the Stock Price of Chevron trend has little to do with the Oil Commodity Price trend. In fact, if by looking just at numbers it almost seems like if the relationship was actually opposite. Nevertheless, this is not realistic as seen in figure 4, and it is better to say that there is no real relationship between the company’s stock price and the performance of its primary commodity but unto later quarters when low prices have already resulted in lower profits and harmed the company’s finances. The lack of trend relation between price change per year between Energy companies and their primary products can be observed in figure 4.

Chevron is a company that has maintained a bull trend since its existence despite numerous due to pollution accidents and scandalous news due to wrong management decisions. Similarly, oil is a commodity that has kept a bullish trend even when being almost a capital sin for many activists due to pollution and to the results of the profits it has generated. Also though neither Chevron nor Oil has always been the most popular both provide needed value to society, a fact for which both are still in business. In this article we have seen how in the information era news can affect prices almost immediately, making markets more effective but perhaps less accurate regarding the actual valuing of the worth of the good being traded. As suspected, markets proved to be mostly speculative in this article when failing to correlate Chevron, a huge energy company to oil, its primary commodity.

In an ideal world where the actual worth of each resource and company is precisely determined by the market, the relationship between big energy companies and their main commodities would be just the same. It makes perfect logical sense that when prices of the main product of a company change, the cost of the stock of the company would vary by a similar amount since then, its profits are related. Nevertheless, markets are not always logical, and the amount of smart money being traded with hedging is less than that of dumb money, which is mostly speculative. It’s uncertain because investors are deciding in the future worth of both companies and commodities by focusing on many non-variables, including non-quantifiable ones such as news.

Even though finance has become much more automatized with the usage of computers and more accurate through the utilization of such trading with quantifiable trends, most investors remain to be speculative. Most investors are in the finance business for the profit, and there is close to none in perfect trading, even when arbitraging, the rates for the benefit are minimal. Because people in finance will continue being ambitious, they will keep striving for profit and big wins, taking risks and speculating creating market failures that translate into illogical correlations like those between Chevron and Oil. Both, Chevron and oil have bullish trends today and will maintain them at least for the short term but it’s impossible to forecast the price of either accurately, and because they proved to be unrelated, how each will react to the other.

References

- Chevron (2013). Company History. Chevron.com. Retrieved from http://www.chevron.com/about/history/.

- Freudenrich, Ph.D.,Craig and Jonathan Strickland (2013). How Oil Drilling Works. HowStuffWorks.com. Retrieved from http://science.howstuffworks.com/environmental/energy/oil-‐‑drilling1.htm.

- San Joaquin Valley Geology (2011). The History of the Oil Industry. Sjgs.com. Retrieved from http://www.sjgs.com/history.html.

- Simon Romero (Februrary 8,2008). Court Bars Sale of Billions in Oil Assets by Venezuela. The New York Times. Retrieved from http://www.nytimes.com/2008/02/08/business/worldbusiness/08oil.html?ref=chevroncorporation&_r=0.

- Andrew E. Kramer (June 19, 2008). Deals With Iraq Are Set to Bring Oil Giants Back. The New York Times. Retrieved from http://www.nytimes.com/2008/06/19/world/middleeast/19iraq.html?partner=rssnyt&emc=rss.

- Bloomberg News (May 1, 2009). Lower Profit for Chevron. The New York Times. Retrieved from http://www.nytimes.com/2009/05/02/business/02chevron.html?ref=chevroncorporation.

- Bloomberg News (October 1, 2009). Chevron Names Successor As Its Chief Steps Down. The New York Times. Retrieved from http://query.nytimes.com/gst/fullpage.html?res=9E01E3D71F39F932A35753C 1A96F9C8B63&ref=chevroncorporation

- Simon Romero (February 11, 2010). Sealing Shift, Chávez Gives Contracts to Western Oil Companies. The New York Times. Retrieved from http://www.nytimes.com/2010/02/12/world/americas/12venez.html?ref=chevroncorporation.

- Simon Romero and Clifford Krauss (February 14, 2011). Ecuador Judge Orders Chevron to Pay $9 Billion. The New York Times. Retrieved from http://www.nytimes.com/2011/02/15/world/americas/15ecuador.html?ref=chevroncorporation.

- Bloomberg News (April 30, 2011). Chevron Profit Rises as Unrest Lifts Oil Prices. The New York Times. Retrieved from http://query.nytimes.com/gst/fullpage.html?res=9A04E5D7103BF933A05757C0A9679D8B63&ref=chevroncorporation.

- Michael J. De la Merced (September 12, 2012). Chesapeake Energy to Sell Assets for $6.9 Billion. DealB%k. Retrieved from http://dealbook.nytimes.com/2012/09/12/chesapeake-‐‑to-‐‑sell-‐‑assets-‐‑for-‐‑6-‐‑9-‐‑ billion/?ref=chevroncorporation.

- Stanley Reed (October 25, 2012). Chevron, Intent on European Shale Gas, Buys Lithuanian Stake. The New York Times. Retrieved from http://www.nytimes.com/2012/10/26/business/energy-‐‑environment/chevron-‐‑ intent-‐‑on-‐‑european-‐‑shale-‐‑gas-‐‑buys-‐‑lithuanian-‐‑ stake.html?ref=chevroncorporation.

- Coral Davenport (December 5, 2013). Large Companies Prepared to Pay Price on Carbon. The New York Times. Retrieved from http://www.nytimes.com/2013/12/05/business/energy-‐‑environment/large-‐‑ companies-‐‑prepared-‐‑to-‐‑pay-‐‑price-‐‑on-‐‑carbon.html?ref=chevroncorporation.

- Stanley Reed (July 23, 2013). Chevron to Spend $844 Million on Remote Projects. The New York Times. Retrieved from http://www.nytimes.com/2013/07/24/business/energy- ‑environment/chevron-‐‑ to-‐‑spend-‐‑770-‐‑million-‐‑on-‐‑remote-‐‑projects.html?ref=chevroncorporation.

- Index Mundi (2013). Index Mundi.com. Retrieved from http://www.indexmundi.com/commodities/?commodity=crude-‐‑oil-‐‑west-‐‑ texas-‐‑intermediate&months=60.

- Shawn Tully (July 15, 2008). Why oil prices will tank. CNN Money. Retrieved from http://money.cnn.com/2008/06/06/news/economy/tully_oil_bust.fortune/.

- Brian O’Keefe (June 16, 2009). Why oil is on the rise again. CNN Money. Retrieved from http://money.cnn.com/2009/06/16/news/economy/oil_on_rise_again.fortune/.

- Steve Hargreaves (December 5, 2011). Gasoline: The new big U.S. export. CNN Money. Retrieved from http://money.cnn.com/2011/12/05/news/economy/gasoline_export/.

- Mark Thompson (November 12, 2012). U.S. to become biggest oil producer — IEA. CNN Money. Retrieved from http://money.cnn.com/2012/11/12/news/economy/us-‐‑oil-‐‑production-‐‑energy/.

- The Economist (December 14, 2013). Spreading disarray. The Economist. Retrieved from http://www.economist.com/news/finance-‐‑and-‐‑ economics/21591630-‐‑why-‐‑price-‐‑crude-‐‑america-‐‑out-‐‑whack-‐‑ rest?zid=298&ah=0bc99f9da8f185b2964b6cef412227be.

- The New York Times (2013). Analysis Tools. The New York Times. Retrieved from http://markets.on.nytimes.com/research/stocks/tools/analysis_tools.asp?symbol=CVX.

- Allan Sloan (June 22, 2010). Overreaction: The real damage from the BP oil spill. CNN Money. Retrieved from http://money.cnn.com/2010/06/22/news/companies/oil_spill_reaction.fortune/.

- U.S. Energy Information Administration (December 14, 2013). Spot Prices. eia.gov. Retrieved from http://www.eia.gov/dnav/pet/pet_pri_spt_s1_a.htm.

- Chevron (2013). Historical Price Lookup. Chevron.com. Retrieved from http://investor.chevron.com/phoenix.zhtml?c=130102&p=irol-‐‑ stocklookup&t=HistQuote&control_firstdatereturned=.

- Dow Jones Newswires (Thursday, July 19, 2012). Chevron Reliance Sign Preliminary Kurdistan Oil Deal. Rigzone. Retrieved from http://www.rigzone.com/news/oil_gas/a/119436/Chevron_Reliance_Sign_Prel iminary_Kurdistan_Oil_Deal.

Please follow up with any feedback or doubts about this article, thanks.

~Roberto Baldizon