How Does a Broke Writer Get a Mortgage?

Some Day You Might Have to Leave the Coffee Shop and Own a Home

If you’re a freelance anything and single, you’re probably renting an apartment and broke.

That might be fine with you and fit perfectly with where you are in life right now. When I was in my 20’s I was ok with being broke (I didn’t even really know that I was), and living in an apartment.

Someday I would like to return to the equivalent of apartment living. I’m not handy and I don’t have time to become handy. Right now with a family that won’t work. Suburbia beckons.

You may be wondering if you will ever be able to buy a house someday and qualify for a mortgage. Some of your friends probably work salaried jobs and own houses right now.

I have good news: you can too, it just takes some planning. It doesn’t have to be complicated. Here are some things you can do to prepare for qualifying for a mortgage:

- Schedule an appointment with a Loan Officer so you can have your credit checked to see where you stand.

2. Hopefully, you have a good CPA. Tell them you want to position yourself to buy a home in the near future.

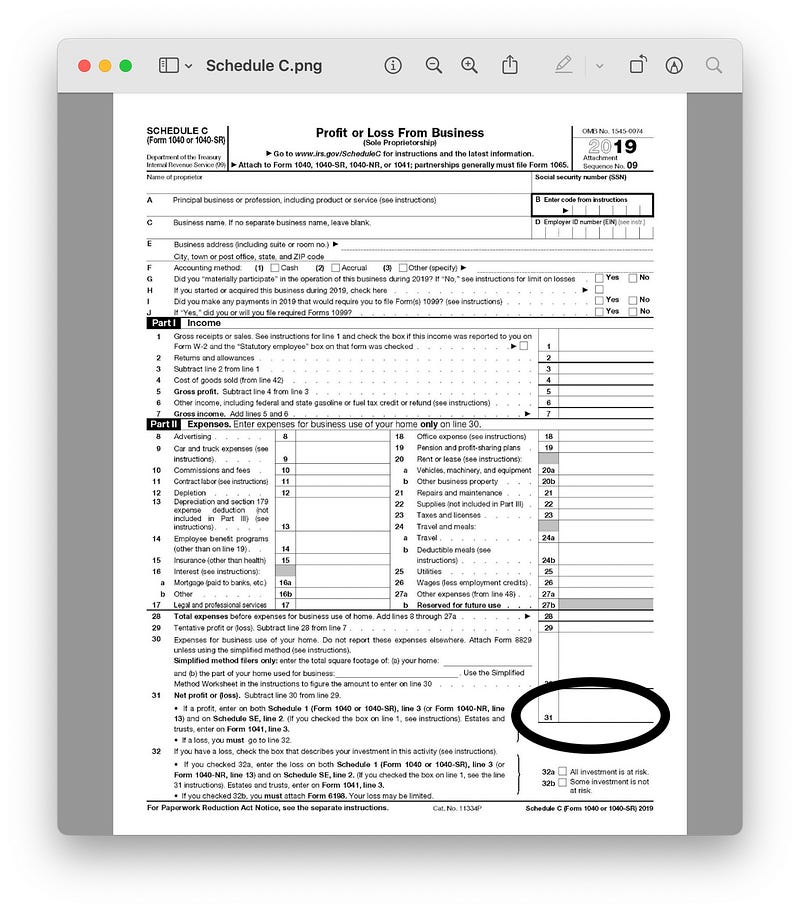

3. Understand your tax returns. Freelancers are “Sole Proprietors”. This means that all of your income and expenses get reported on a “Schedule C”. We will need to see your last two years of tax returns in order to calculate your income.

4. Look at Schedule C below. The number that we use to calculate your income is line 31: net income. We will divide that number by twelve to determine the monthly income that we can use.

4. Begin to keep a monthly Profit and Loss Statement. This doesn’t have to be anything complicated. You just need to track your monthly income and expenses. Basically, a Schedule C is a glorified Profit and Loss statement.

5. Save, save, save for your down payment and closing costs. I tell my borrowers to do some research on the sales prices for the types of homes they are interested in and then multiply that price by 7%. For example, for a $300k home, you will need around $21k.

Again, it just takes a little bit of planning to get ahead of the game. Even though you’re broke now, you might not always be.