How Can Rachel Not Get Totally Screwed by Her 7% Mortgage Interest Rate?

Part 2. I predict more and more people are going to be doing this with their mortgages now and for at least the next few years.

Related

• 4 Things Smart Homebuyers Do If Their Mortgage Rate Is Over 5% • Part 1: Rachel Bought Her House One Year After Jackie — And Her Personal Financial Results Were So Much Worse than Jackie’s • What Do U.S. Housing Price Predictions for 2023–2024 Look Like and Why? • Q&A on Housing Price Predictions for 2023 and 2024 • Why Are Chinese People Smarter About Mortgages than Americans? • Is the Stock Market Really in a Bear Market? Maybe. Maybe Not. • Mortgage Borrowing for YOUR Benefit: Pay Less Interest

Recent

• When Did this Safeway in San Francisco Turn Into Dangerway? • How the Al Dente App Eliminates the MacBook Battery Life Problem • The Social Contract Broke in the U.S. Years Later Than in Japan • The Ultimate Question for Starting a Conversation Between Two People

Potential to Change the Way You Think

• Life Expectancy vs. Healthcare Costs in the U.S. and Other Countries • Why Should You Vote “Blue No Matter Who” When Centrist Dems Never Play to Win? • Six Behavioral Barriers That Prevent You from Changing the Status Quo — Part 5. Smart Man’s Disease

When we last visited Rachel and Jackie (“Rachel Bought Her House One Year After Jackie — And the Results Were Unbelievably Worse”), they had both purchased a house. Jackie bought hers in October 2021, and Rachel bought hers in October 2022.

Each woman was making the same monthly mortgage payment — $2,866.

But because Jackie bought her house in October 2021, she got a mortgage interest rate of 3.00%.

- Jackie was able to buy a house with a price tag of $680,000.

- And over the 30-year term of the mortgage, she will end up paying $352,000 in total interest to her bank.

By contrast, because Rachel bought her house 12 months later in October 2022, her mortgage interest rate was 7.00%.

- With her $2,866 monthly mortgage payment, Rachel was only able to buy a house with a price tag of $431,000.

- And over the 30 year term of her mortgage, she will end up paying her bank a whopping $601,000 in total interest!

So we ended that article feeling pretty bad for Rachel.

As a matter of fact, one reader could only suggest that, “Rachel should’ve bought her house a year ago as well.”

Ouch. That is cold comfort indeed.

In the absence of a working time machine, though, there is actually something that Rachel can do to improve her situation.

It’s simple — pay at least a little bit more with her monthly payments.

This will save 35–65% — or more — of the $249K in extra interest Rachel will need to pay if she only does what ALL the so-called experts are telling her to do.

Yes, I know I said neither woman could pay a penny more each month. I was doing that mostly for dramatic effect in the prior article. There is almost always something you can do to scrounge up a little extra money each month.

It turns out that 10% additional paid each month makes a huge difference.

Interest

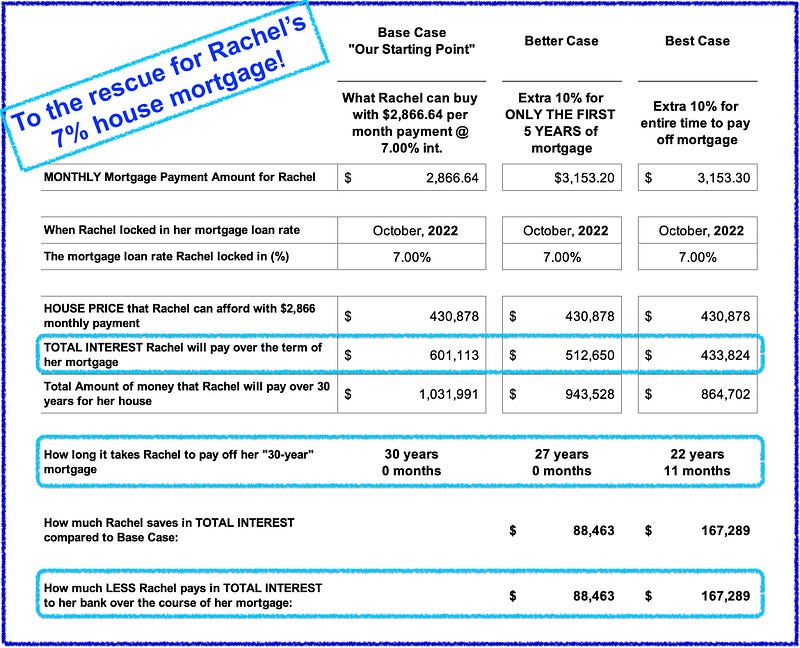

In terms of total interest paid, if Rachel pays an extra 10% with her $2,866 regular monthly payment, that is an extra $287 each month or a new total of $3,153 each month.

How much of a difference does this make?

A lot.

She will pay $167,300 LESS in total interest to the bank over the full term of her mortgage.

Let the weeping at the bank begin!

But wait — that’s not all. There’s another upside for Rachel.

Total time to pay off the mortgage

Instead of it taking the standard 30 years to pay off her “30-year fixed-rate” mortgage, Rachel will pay it off in only 22 years, 11 months!

That means she finishes her 30-year mortgage more than 7 years early!

So for those last 7 years and 1 month, Rachel will have NO monthly mortgage payment.

And that’s all because she paid an extra 10% each month.

It makes that big a difference when you start having a higher and higher interest rate on your loan.

But what if — no matter how much she wants to — Rachel just can’t commit to paying an extra 10% each month for almost 23 years?

In that case, just pay the extra amount for the first 5 years.

Doing this will still shave $88,000 off the $249,000 Rachel would otherwise pay in “extra” interest vs. what Jackie is paying.

Most of the bang for buck you get by paying early happens with the extra payments in the first few years of a long-term mortgage.

Here’s what paying extra will do for Rachel…and what it WON’T do for Rachel.

It does decrease the total interest she will pay, just as I detailed above.

However, if we are cutting the amount of interest she will pay by the amount described, then that means that we aren’t increasing the overall price of the house that Rachel can afford to buy.

We COULD keep the total interest amount constant — at $249,000 more than Jackie’s total interest — and then “increase” the price tag of the house Rachel can afford.

That works.

Or we could do a combination of the two — somewhat raise the price of the house Rachel can afford AND also somewhat decrease the total amount of interest Rachel pays.

That will work, too.

Bottom line, Rachel DOES have some options.

The question that I will leave readers with to ponder is this:

“Why do NONE of the housing and property and mortgage experts that get interviewed on CNBC and FOXBusiness and MSNBC, etc. EVER talk seriously about extra monthly payments as an option?

On this particular option, there is a deafening silence coming from all of these experts. Or they always have a “good reason” why it doesn’t make sense. (Spoiler alert: they are either flat-out wrong or incredibly shallow in their reasoning and justifications for this bad advice.)

Why might that be?”

Your thoughts . . . ?

Related

• 4 Things Smart Homebuyers Do If Their Mortgage Rate Is Over 5% • Part 1: Rachel Bought Her House One Year After Jackie — And Her Personal Financial Results Were So Much Worse than Jackie’s • What Do U.S. Housing Price Predictions for 2023–2024 Look Like and Why? • Q&A on Housing Price Predictions for 2023 and 2024 • Why Are Chinese People Smarter About Mortgages than Americans? • Is the Stock Market Really in a Bear Market? Maybe. Maybe Not. • Mortgage Borrowing for YOUR Benefit: Pay Less Interest

Recent

• When Did this Safeway in San Francisco Turn Into Dangerway? • How the Al Dente App Eliminates the MacBook Battery Life Problem • The Social Contract Broke in the U.S. Years Later Than in Japan • The Ultimate Question for Starting a Conversation Between Two People

Potential to Change the Way You Think

• Life Expectancy vs. Healthcare Costs in the U.S. and Other Countries • Why Should You Vote “Blue No Matter Who” When Centrist Dems Never Play to Win? • Six Behavioral Barriers That Prevent You from Changing the Status Quo — Part 5. Smart Man’s Disease

Want unlimited access to all Medium articles? Become a member!

Would you like me to cover a topic? Please post suggestions in the comments, and I’ll use your input to help prioritize my writing and research.

If you appreciate my writing, please share it on social media.

Again, thank you for reading, subscribing, clapping, and sharing — your time and attention are deeply appreciated!