How an Extra $100 of Monthly Income Can Impact Your Future Wealth

Relax, side jobs do not need to become full-time careers to change your life.

What would happen if you made an additional $100 per month?

For starters, you’d technically be an entrepreneur based on a simplified definition: earning money from more than one source. Whether it’s from designing graphics, coding for websites, ridesharing, writing, consulting based on your professional experience, tutoring students, giving musical lessons, selling crafts on Etsy, or whatever side gig you can think of.

It doesn’t have to be a time-consuming activity, especially if it’s an existing skill or ability.

If you can make $50 an hour teaching piano to kids, that’s just a 30-minute lesson once a week. If you can walk a neighbor’s dog five times a week for $10 per walk, you’ll double what you need in a month and get some exercise. A good friend of mine started selling dog bandanas on Etsy and has already broken even.

$100 has more of an impact than you might think, especially when you put that extra Benjamin to good use.

The long-term financial impact of an extra $100

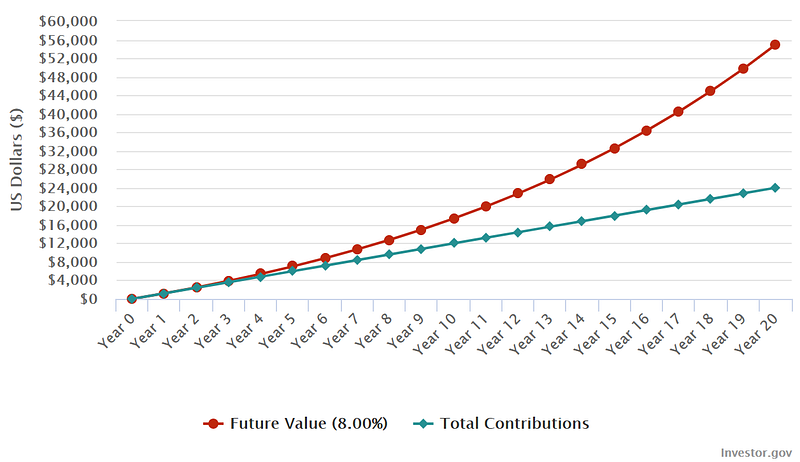

Let’s assume you don’t need this extra $100 to cover any ongoing lifestyle expenses. Instead, you treat it as bonus savings. Each month, you set this $100 aside in a brokerage account that’s scheduled to buy a market index fund — one of the most common and easiest routes to consistent, long-term investing. Accounting for inflation, the market’s average annual return is about 8% historically.

Based on these assumptions, you could realistically expect to contribute $24,000 to your brokerage account over the next 20 years. At an 8% inflation-adjusted annual return, your portfolio of bonus savings could be worth around $55,000.

That’s a downpayment on a pretty solid house, depending on the location. That’s a brand new car — no loan necessary. That’s a helluva travel fund for an assortment of international trips.

Regardless, it’s a significant amount of money for a pretty minimal commitment — a commitment that doesn’t eat into much of your free time.

How much time do you spend mindlessly scrolling through social media? Or rewatching shows and movies on Netflix? You don’t even have to stop doing these activities to make another $100; you just have to be willing to spend a little less time on The Office and a little more time on another source of pleasure and money.

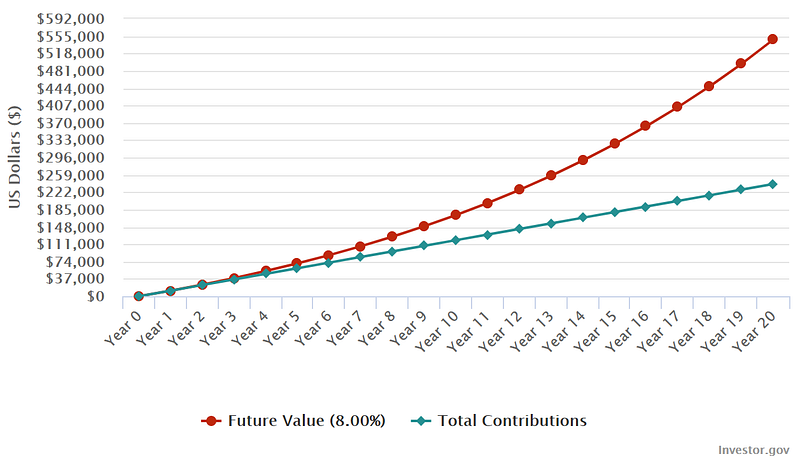

Keep in mind: this $100 is extra savings that you didn’t have before. Based on the average household’s after-tax earnings and expenses (for 25 to 34-year-olds), the typical household saves $897 per month (as of 2019). If we combine the extra side income with the average monthly savings, you could reasonably expect to accumulate almost $550,000 over the next 20 years:

Is that enough to retire? That depends on your desired lifestyle and a slew of other financial factors. But, in this 20-year case study, that side job helps accumulate 10% more wealth.

What is your free time worth to you?

Entrepreneurship doesn’t require you to commit your entire life to work. You don’t have to handcuff yourself to a desk. You don’t have to hustle your way to a six-figure side business to make a financial impact on your life.

Even a few hours a month doing something that you either (a) enjoy or (b) have experience doing can alter your financial future.

If that side gig evolves and replaces your full-time job, congratulations — that’s phenomenal.

If that side gig stays true to its label, congratulations — you’re still reaping the benefits of time well spent.