How an Excel Error Cost JP Morgan $6 Billion

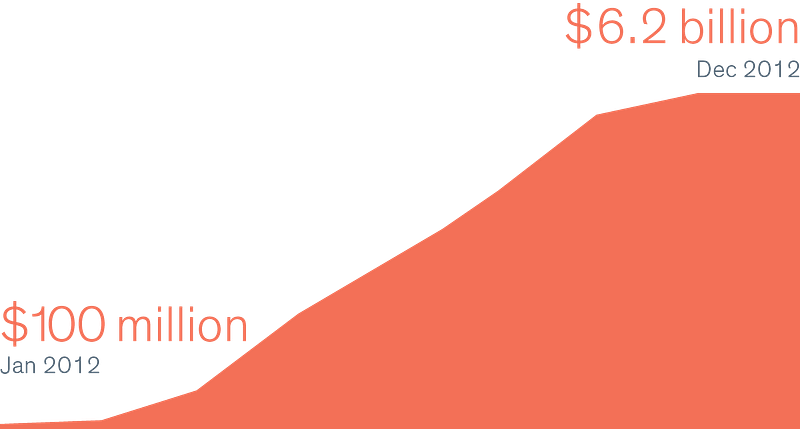

In 2012, JP Morgan Chase, a leading financial services firm, faced a $6 billion loss, due to an Excel error in their Value-at-Risk (VaR) model.

How to Get Rich with Investing (without Getting Lucky)

The incident, known as the London Whale Loss, traces its roots to an unassuming spreadsheet within JP Morgan’s Value-at-Risk (VaR) model, where an employee’s harmless data transfer between spreadsheets snowballed into a multi-billion-dollar catastrophe.

Also, to read:

The Excel Error

At the heart of the debacle was a simple Excel error — an employee, under the duress of accelerating the review process, mistakenly employed a sum total instead of an average during data transfer.

This seemingly trivial mistake in the VaR model rippled through the financial fabric, distorting risk calculations and painting a deceptive picture of the actual perils at hand.

Unraveling Operational Flaws

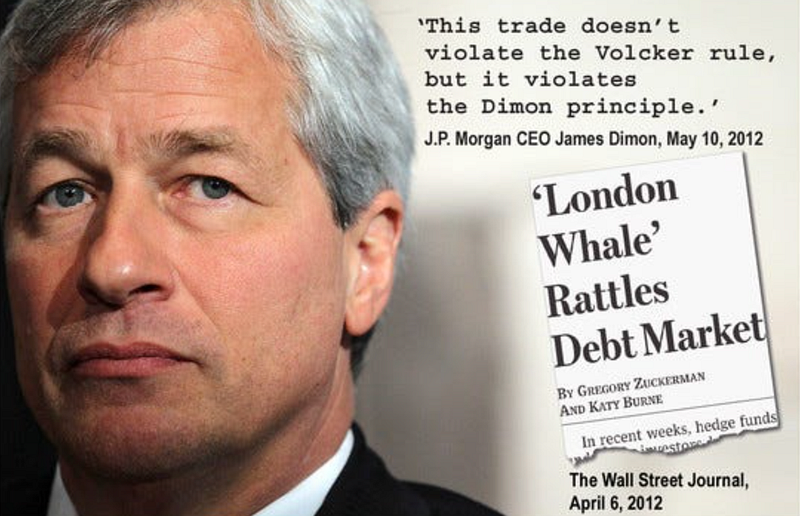

However, the London Whale loss wasn’t solely a consequence of a formula gone astray. Buried within the 129-page report by JP Morgan lies a tale of operational risks and disregard for internal controls.

The Excel model at the center of the storm was never approved for use, and its creator explicitly stated it shouldn’t be deployed. This raises questions not only about the lax approval processes but also about the pressures faced by employees to fast-track critical financial reviews.

VaR Models: Measuring Risk, Not Causing It

It’s crucial to dispel a common misconception: VaR models, while essential in risk management, don’t cause financial losses.

They act as tools to quantify potential losses within a specified confidence level.

In the London Whale case, the VaR model was, in fact, not the harbinger of loss; rather, it was the failure of other risk models, stress tests, and a blatant disregard for known risks.

The JP Morgan report paints a vivid picture of a company aware of the impending storm but choosing to sail into the tempest nonetheless.

Traders, perhaps blinded by short-term gains, turned a blind eye to the red flags raised by risk indicators. The issue wasn’t a lack of information; it was a conscious decision to ignore it.

Lessons Learned: Beyond Excel Woes

As the dust settled and the financial world grappled with the aftermath, the London Whale loss became a case study in risk management.

It’s not just an Excel cautionary tale but a stark reminder that operational flaws, internal control lapses, and willful ignorance can compound even the most sophisticated risk models.

In the wake of such financial tempests, the call for automation echoes loud and clear.

Relying on manual processes, especially in the complex realm of financial modeling, poses substantial risks.

The London Whale incident underscores the need for robust automated systems that not only streamline processes but also mitigate the potential for human error.

Conclusion: Navigating the Financial Seas

The London Whale loss stands as a pivotal moment in the history of finance, a stark reminder of the importance of risk management.

This incident, triggered by a seemingly insignificant error in an Excel spreadsheet, highlights the need for financial institutions to reassess their risk culture, strengthen internal controls, and leverage the power of automation.

Sincerely,

The Pareto Investor

My Book “The Little Principle That Beats the Market” is an essential read for anyone seeking a smarter, more effective way to invest.