Good debt vs. Bad debt: What’s the difference?-Bright

Weigh the balance, and monitor your debt-to-income ratio.

Since the dawn of debt, we’ve always been advised to live within our means. But sensible advice today can still cause problems down the road.

Learn the difference between good debt and bad debt, and then manage it wisely. Handling debt responsibly helps build a good credit score, which can profoundly impact your future, from the kind of car you afford to the house you can buy.

Good debt adds to your wealth

Good debt is money borrowed for things that can add to your wealth in the future or increase your income. Some great examples of good debts:

- Student loans. The money you’re borrowing to attend college will help you land a well-paying job.

- Mortgages. These are usually long-term loans with interest payments that are tax-deductible Home values generally rise over the long term, which can build wealth for you.

- Small business loans. Borrowing to fund a business can help grow regular revenue, which can also add to your future income.

Bad debt only benefits the here and now

Bad debt contributes little or nothing to improve your wealth or income. A few examples of bad debt:

- Credit card debt. It’s probably one of the worst. The interest rates are higher than the rates on other loans, and payment schedules are set to maximize costs for you.

- Auto loans. Cars are an investment you won’t get back. Vehicles depreciate quickly, so to borrow against them is a losing deal. Most auto loans also have high-interest rates.

- Lifestyle spending. Spending on things like vacations or major extravagances are commonly outside monthly budgets. They can bring a lot of joy in the here and now, but they don’t usually improve your wealth or income.

Calculate your DTI (debt-to-income) ratio

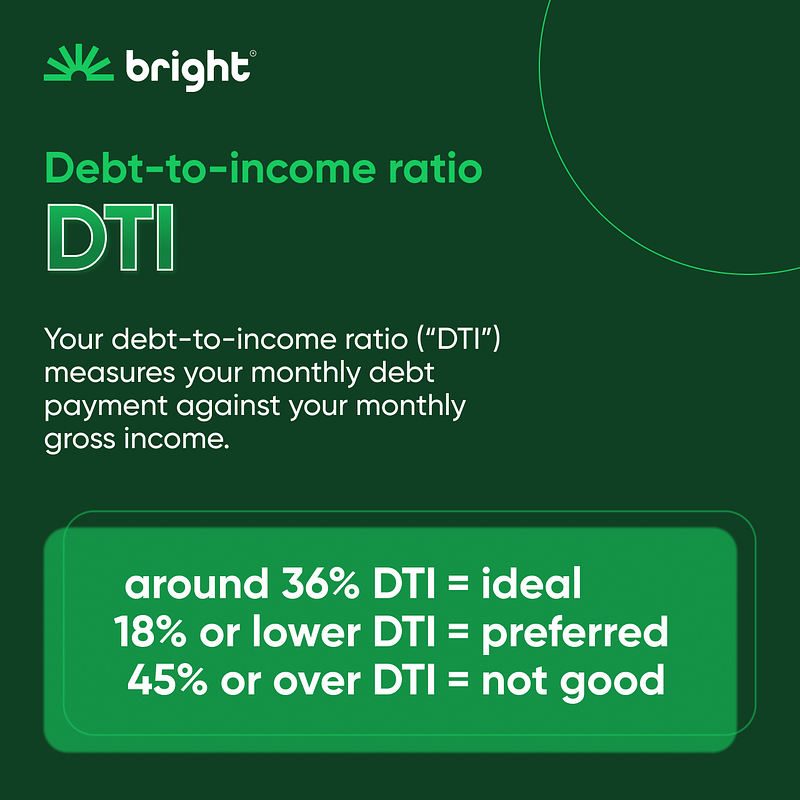

Your debt-to-income ratio (or “DTI”) measures your monthly debt payment against your monthly income (before taxes or before other deductions have been made).

To calculate your DTI, add your total monthly debt payments and divide them by your total pre-tax monthly income. For example, if you pay $200 a month towards your car loan and another $800 towards your mortgage, your monthly debt payments are $1000. If your pre-tax monthly income is $4000, your DTI is 25%.

Understanding your DTI will help you know your debt limit. For example, a DTI of 36% is generally considered ideal, while a DTI of 18% or lower is preferred. Keep in mind that a DTI over 45% can be considered bad debt.

Lenders use your DTI ratio to measure your ability to manage debt — so having a low DTI is vital.

Bright can lower your debt

Your personal Bright Plan learns about your spending habits, understands what you can afford, then makes payments for you to all kinds of debt.

Bright identifies the cards and loans costing you the most interest, then makes sure you’re paying them off at the right time, at a level you can afford.

Recommended Readings:

5 Ways to Pay Off Debts Comfortably

The Benefits of Living Debt Free

Originally published at https://www.brightmoney.co.

{kind=link}