WEEKLY BUSINESS ROUNDUP

Global Business Week: Which is the path to highest investment returns?

The state of Financial markets & Economies, Weekly Charts, Business Trends & Statistics

With Q3 earnings season kicking into gear, the three major U.S. stock averages stayed near record highs in the past week with some fluctuations in between. The Dow finished at its first record high since August. All three major indexes closed on weekly gains for the third straight week — Nasdaq rose 1.3% over the past five sessions, the S&P 500 gained 1.6% & the Dow Jones advanced 1.1%. Inflation worries continue to dampen investor sentiment. And on top of that supply chain disruptions and labor shortages are starting to hurt companies.

Fund managers turned bearish on growth prospects for the first time since the depths of the pandemic, according to a Bank of America Securities Survey. The Dow’s record rise was helped by a 5% jump in shares of American Express after it posted gains in travel and entertainment spending. Snap’s tumble in share value and warning about ad sales sparked by changes in Apple’s privacy policies spilled over to other social media giants. Shares of Facebook, Alphabet, and Twitter were all hit. The 10-year Treasury yield starting the week @ 1.58%, ended at ~1.65%, after breaching 1.7% on Thursday.

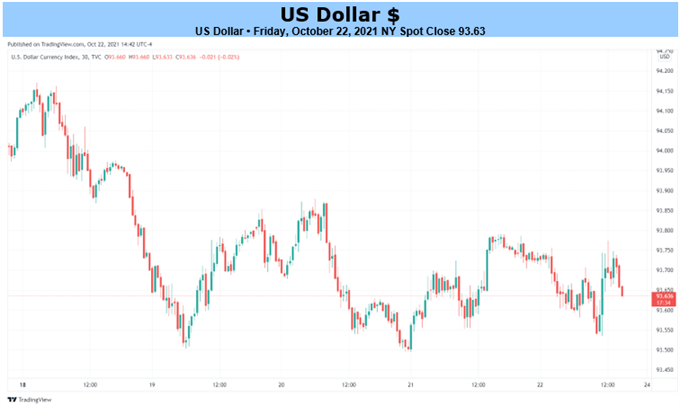

The US Dollar Index (DXY) depreciates for the second week after snapping the opening range for October, and fresh data prints coming out of the US may keep the Greenback under pressure as signs of a slowing recovery undermine speculation for an imminent shift in Federal Reserve policy. For now, the benchmark index is holding near the monthly low of 93.50 — closing the week @ 93.60. The US Dollar may face a larger correction going into the end of the month as the US GDP report is anticipated to show a slowing recovery, but speculation for a shift in Fed policy may keep the Greenback afloat as it lifts longer-dated Treasury yields.

{kind=link}

The Crypto industry celebrated a long-awaited milestone this week as the first exchange-traded fund linked to Bitcoin (BTC-USD) launched on the New York Stock Exchange. The ProShares Bitcoin Strategy ETF (BITO) does not invest directly in Bitcoin, but rather holds futures contracts of the digital currency — meaning it will have a very high correlation with Bitcoin, but won’t mirror the token’s exact value. It will also cost more to own the fund, but some may be willing to pay up for institutional level custody, execution & security.

The news provided strong momentum to the BTC price as it broke through to a new all-time high (ATH) of around $67k, before receding — at the time of writing, it stood just above $61k. Taking a cue from the pioneering digital currency, the Alt. coins pushed ahead too. Ethereum touched the previous ATH, before correcting itself — trading around $4100 at the time of publishing. Overall, the total market cap of the crypto assets whizzed past $2.5 trillion.

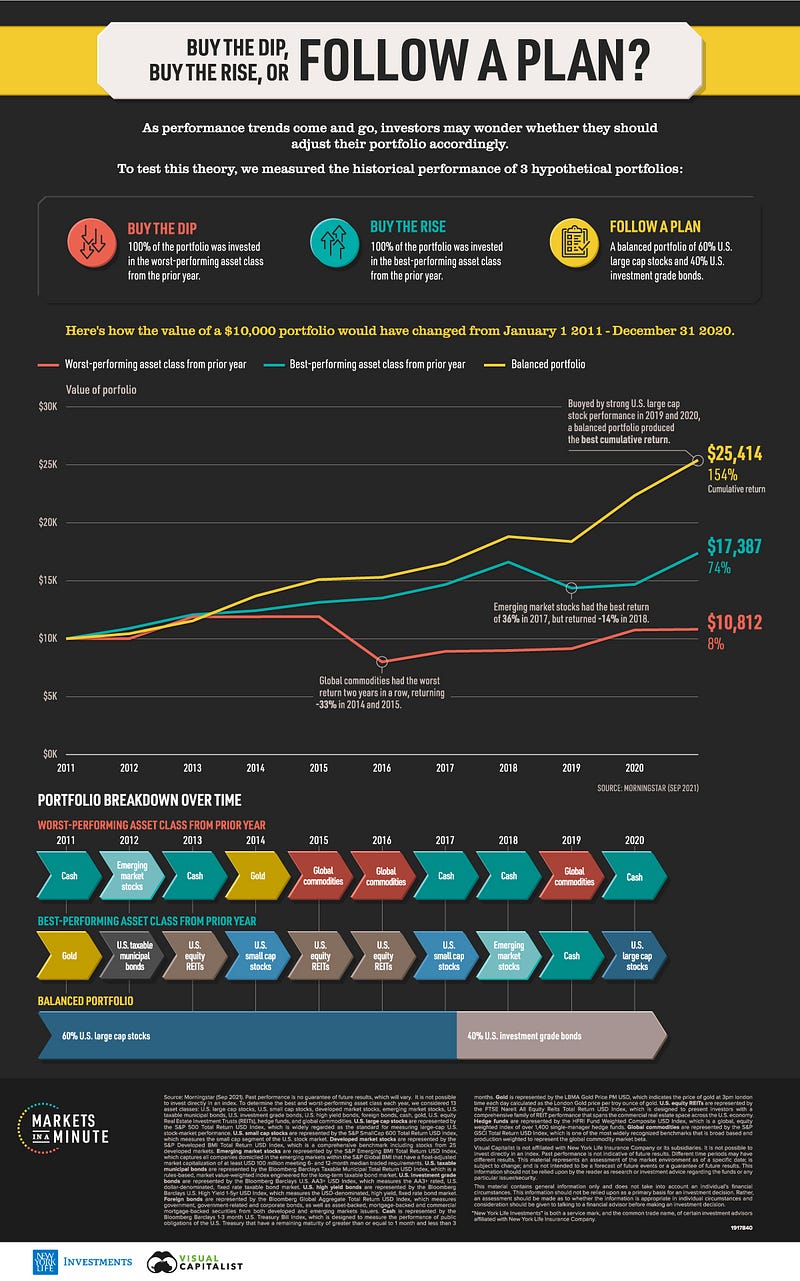

Today’s featured infographic from New York Life Investments compares what investment strategies to adopt for the best possible investment returns on your portfolio.

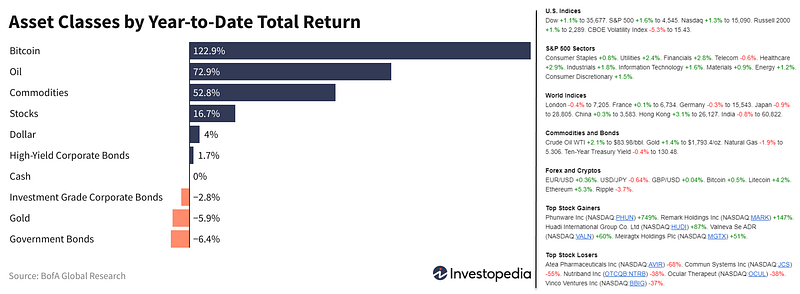

And finally, before moving on to some other statistics, here are the weekly & YTD numbers from various markets and different assets (Figure 1).

Global Inflation Worries

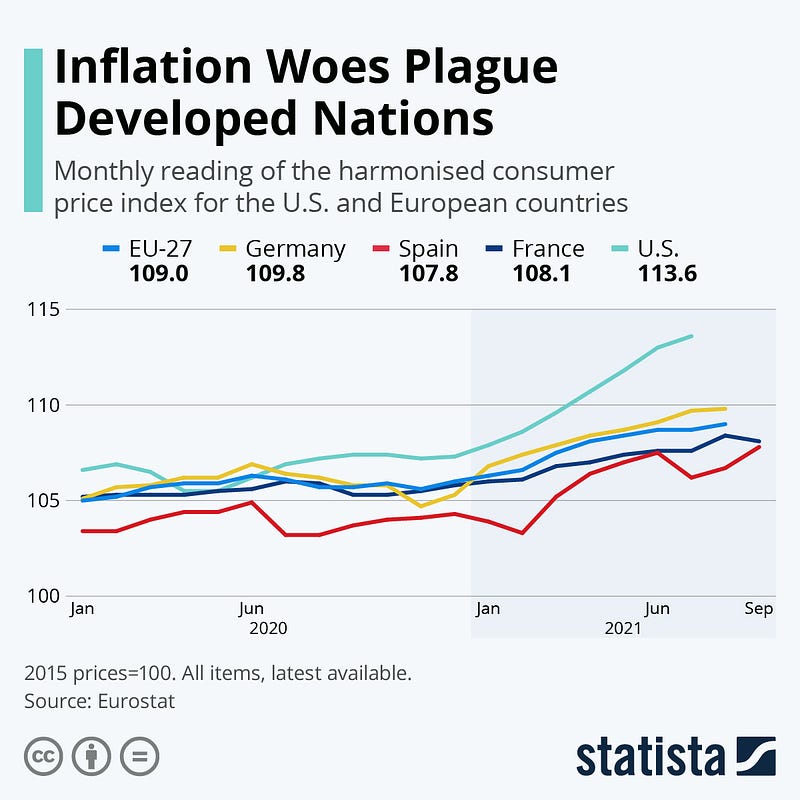

Strong economic recovery following the lockdown era of the coronavirus pandemic has caused the price of goods and services to rise since the start of 2021 in many developed nations. Consumers catching up on spending coupled with persistent stock problems have created a climate of scarcity as pandemic effects continue to influence the global supply chain. In September, the Harmonised Consumer Price Index published monthly by Eurostat rose by 3.6% year-on-year in the European Union and by 6.2% in the United States. Within Europe, some countries like Germany experienced above-average inflation, while in France and Spain, for example, it remained below the European Union figure (Figure 2). In July, Fed chairman Jerome Powell argued that the stronger average inflation in the United States was dragged up by only a few items, like the price of used cars and trucks, which has been rising at an astonishingly quick rate. More strong price increases were registered for gasoline, but the product also experienced some of the biggest price fluctuations in the pandemic.

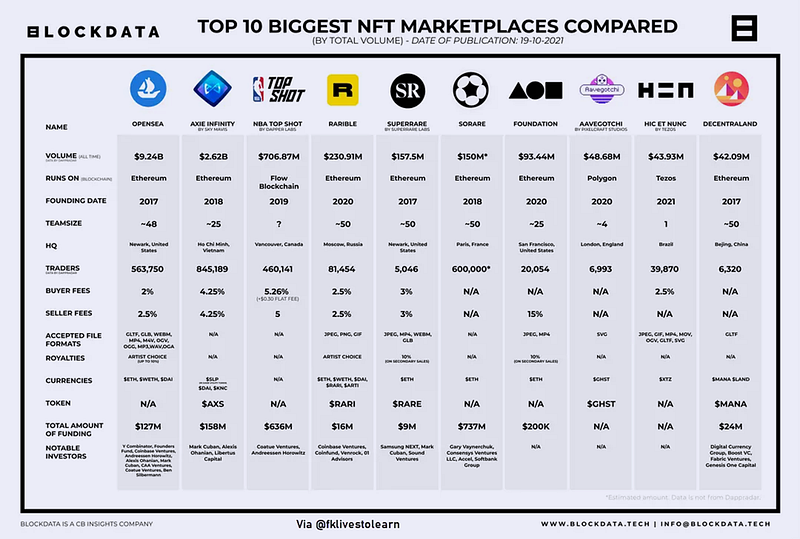

Top 10 NFT Marketplaces

Coinbase recently announced they are going to launch a peer-to-peer NFT marketplace this year and has already opened a waiting list for it. Household industry names like FTX and Binance also launched their NFT marketplaces not long ago. It’s now clear that the biggest crypto players are going to fight for NFT market share and it’s interesting to see what unique characteristics and USPs will make up for the success. NFT sales volume surged to $10.7 billion in the third quarter of 2021, up more than eightfold from Q2, according to data from market tracker DappRadar. The top 10 marketplaces by volume represent over 90% of the total volume by NFT marketplaces (Figure 3).

Energy Prices Moderation

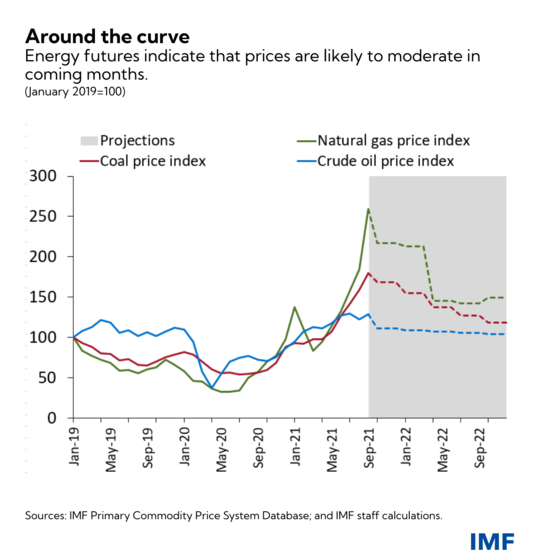

While supply disruptions and price pressures pose unprecedented challenges for a world already grappling with an uneven pandemic recovery, the silver lining for policymakers is that the situation doesn’t compare to the early 1970s energy shock. Back then, oil prices quadrupled, directly hitting household and business purchasing power and, eventually, causing a global recession. Nearly a half-century later, given the less dominant role that coal and natural gas play in the world’s economy, energy prices would need to rise much more significantly to cause such a dramatic shock. Moreover, we expect natural gas prices to normalize by the second quarter as the end of winter in Europe and Asia eases seasonal pressures, as futures markets also indicate (Figure 4). Coal and crude oil prices are also likely to decline. However, uncertainty remains high & small demand shocks could trigger fresh price spikes.

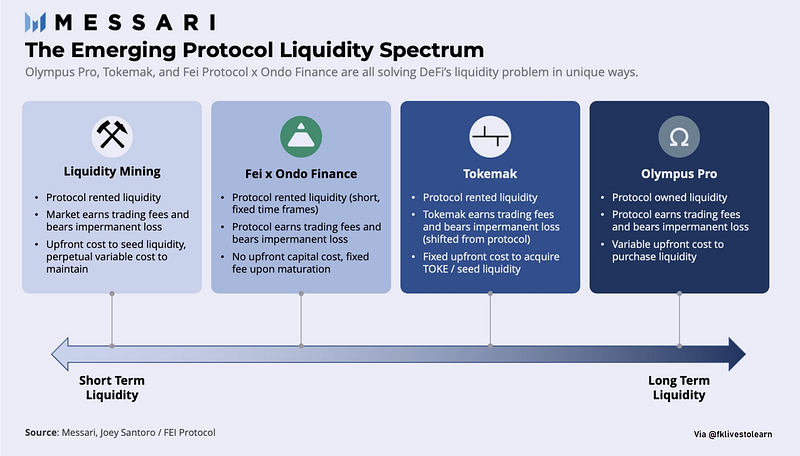

Emerging Protocol Liquidity Spectrum

After a prolonged stagnation, DeFi has once again resurfaced among crypto’s leading narratives. The resurgence is primarily being led by the contentious term “DeFi 2.0”, coined by the pseudonymous developer of Alchemix Finance, Scoopy Trooples. In a recent Twitter thread, Scoopy highlighted a number of second-generation protocols (Figure 5) building upon the 0 to 1 innovations created by the first generation of DeFi protocols such as MakerDAO, Uniswap, Compound, and Yearn. This classification sparked infighting over the categorization of DeFi protocols and pulled the attention away from the actual shifts occurring under the hood. Twitter timelines have been left in constant confusion with everyone asking the same question about their favorite OlympusDAO fork.

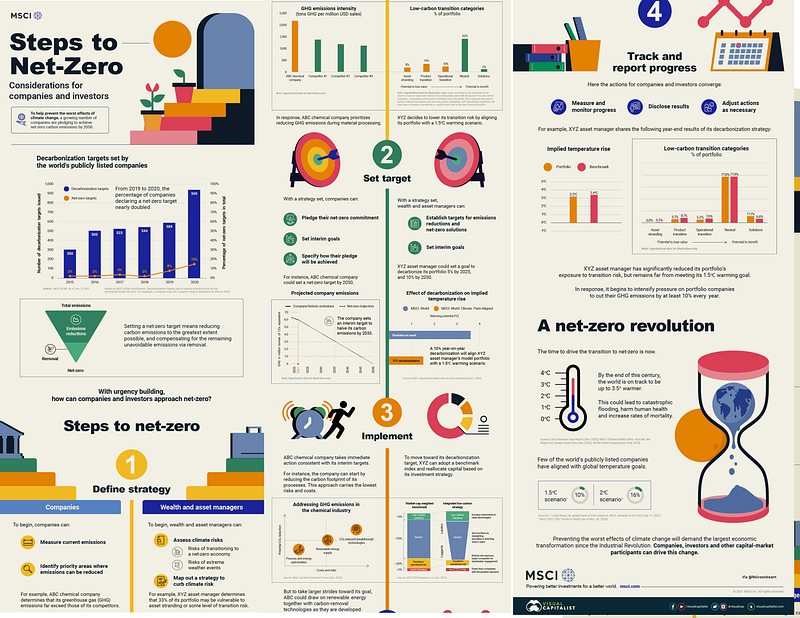

Net-Zero Emissions by Companies

To help prevent the worst effects of climate change, a growing number of companies are pledging to achieve net-zero emissions by 2050. In fact, the percentage of companies declaring a net-zero target nearly doubled from 2019 to 2020. With urgency building, how can companies and investors approach net-zero emissions? The above infographic from MSCI (Figure 6) highlights the steps these two groups can take, from defining a strategy to reporting progress.

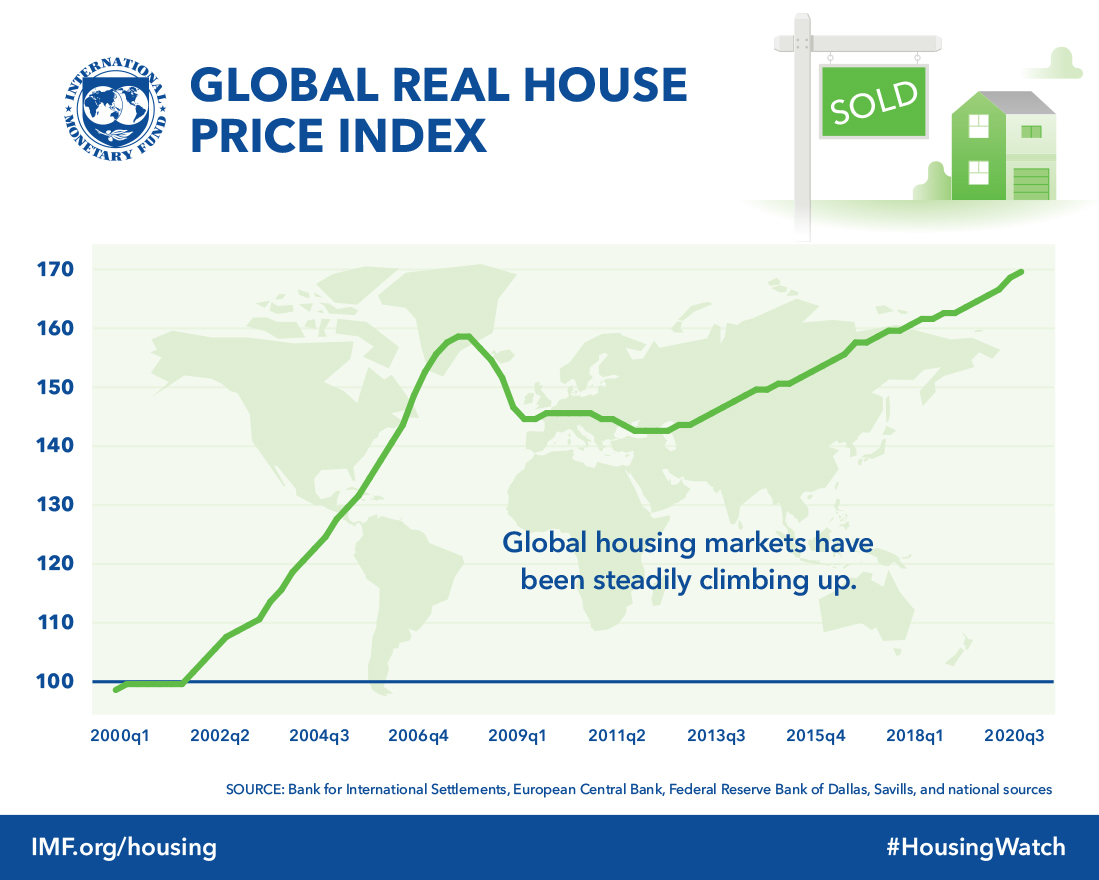

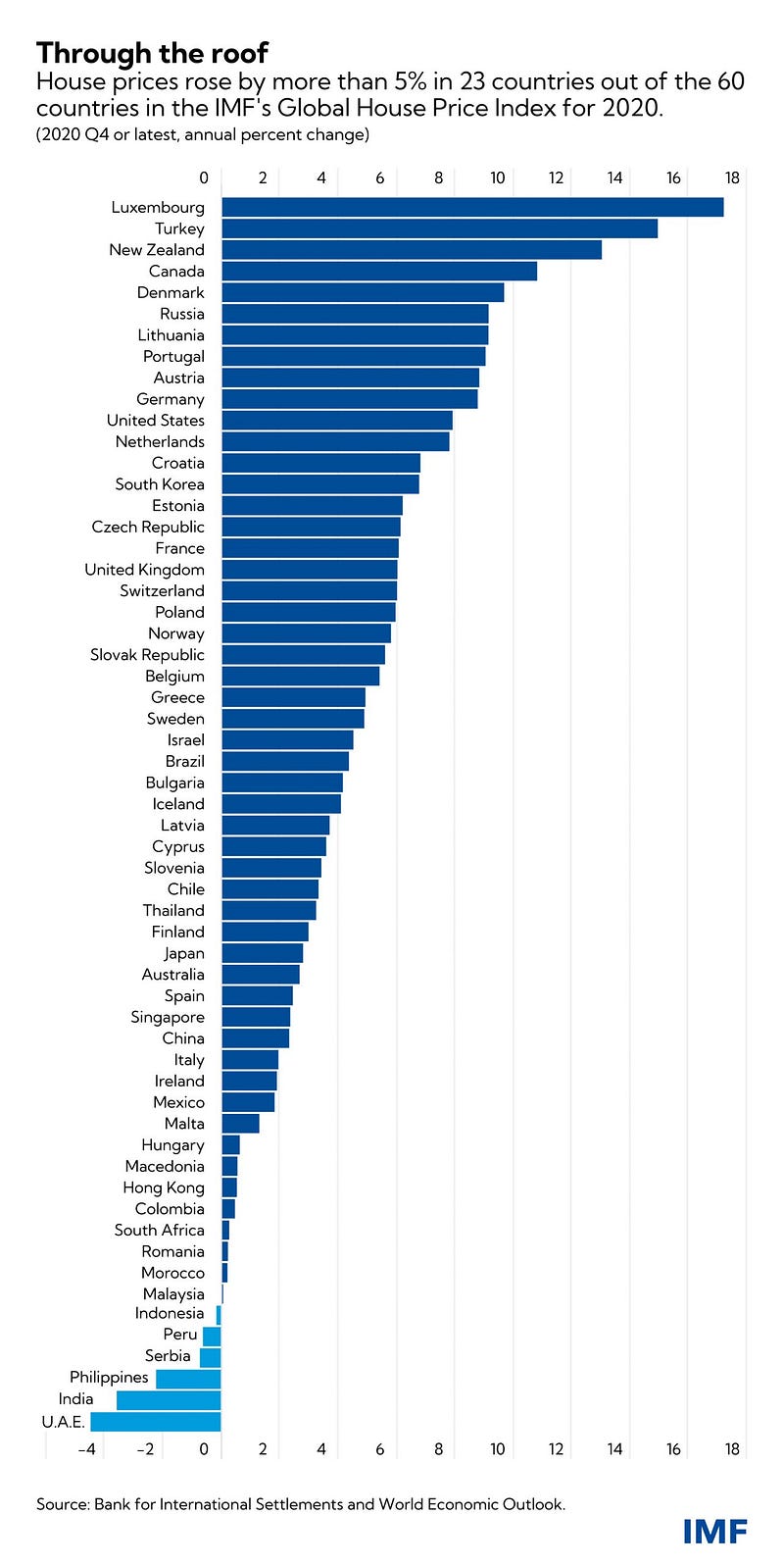

Global House Prices

While most economic indicators deteriorated last year, house prices largely shrugged off the effects of the pandemic. Of the over 60 countries that enter into the IMF’s Global House Price Index, three-quarters saw increases in house prices during 2020 (Figure 7), and this trend has largely continued in countries with more recent data. IMF research indicates that low-interest rates contributed to the boom in house prices, as did policy support provided by governments and workers’ greater need to be able to work from home. In many countries, including the United States, online searches for homes reached record levels. Along with these demand factors, house prices also increased as supply chain disruptions raised the costs of several inputs into the construction process.

{kind=link}

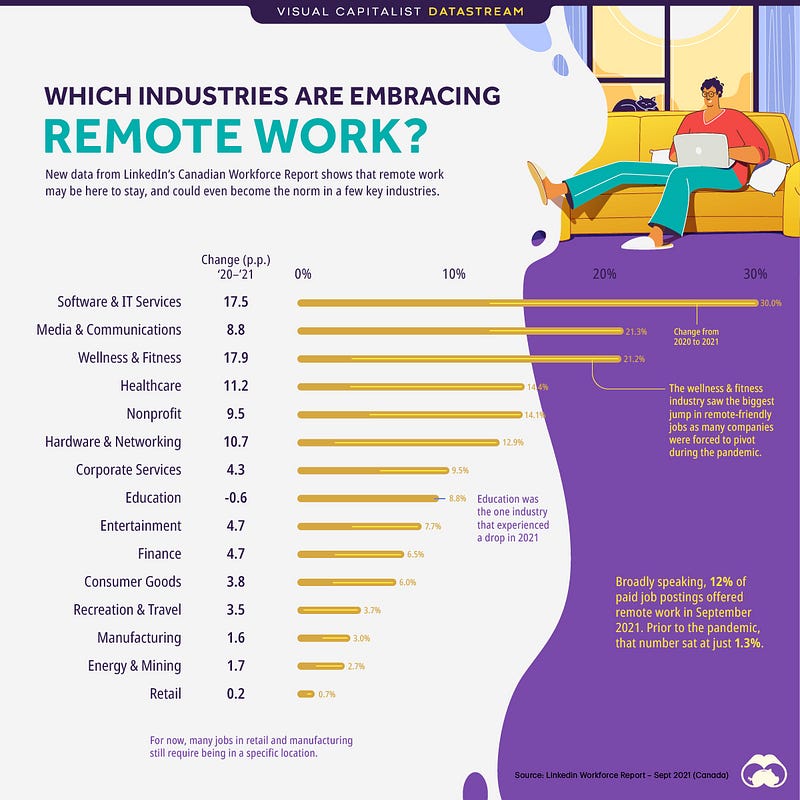

Shift to Remote Work

When the pandemic first took hold in 2020, and many workplaces around the world closed their doors, a grand experiment in work-from-home began. Today, well over a year after the first lockdown measures were put in place, there are still lingering questions about whether remote work would now become a commonplace option, or whether things would generally return to the status quo in offices around the world. New data from LinkedIn’s Workforce Report shows (Figure 8) that remote work may be here to stay, and could even become the norm in a few key industries. Broadly speaking, 12% of all Canadian paid job postings on LinkedIn offered remote work in September 2021. Prior to the pandemic, that number sat at just 1.3%. While this data was specific to Canada, the country’s similarity to the U.S. means that these trends are likely being seen across the border as well.

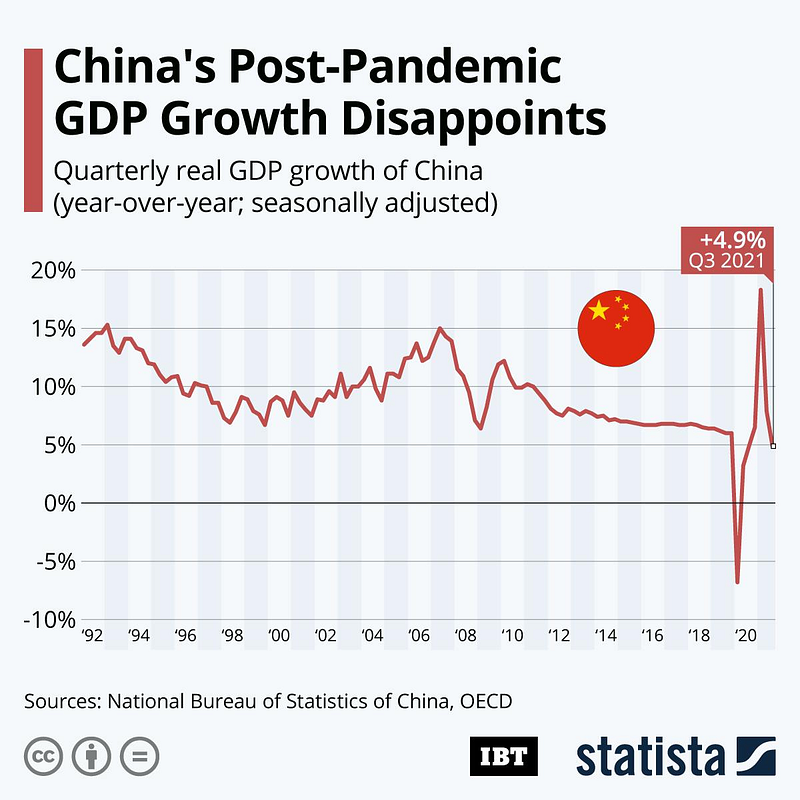

China’s post-pandemic GDP Slows

The Q3 GDP growth of China, published recently, can be seen as the first real post-pandemic reading by the country. Despite the effects of the coronavirus crisis not affecting the year-over-year figures anymore, the results nevertheless turned out disappointing at just 4.9% growth (Figure 9). Experts had expected a growth of 5.2% YOY. While Q1 and Q2 GDP growth in 2021 were calculated against the pandemic quarters of 2020 and seemed sky-high for that reason, Q3 of 2021 is using Q3 of 2020 as a reference. By that time, the pandemic was virtually over in China and GDP growth had normalized. Yet, the coronavirus plagued the rest of the world for longer, affecting the global economy and in extension China.

Market Humor: Bitcoin Takes Wall Street By Storm As ETF Launch Powers Record-Breaking Rally!

Previous Edition of GBW