Game Changer: Every American Will Be Able To Buy Bitcoin Through Their Current Bank

U.S. banks are finally ready to incorporate digital currency.

Is the stock market collapsing?

No. Not yet, anyway.

We’re just seeing a minor correction in the stock markets right now.

The S&P500 dropped 2,67% since its all-time highs, but we can’t call it a correction.

A correction is a decline of 10% or more significant in the price of a security, asset, or financial market. Corrections can last anywhere from days to months. A correction can be healthy, adjusting overvalued asset prices and providing buying opportunities.

According to a 2018 CNBC report, the average correction for the S&P 500 lasted only four months and values fell around 13% before recovering.- investopedia.com

The tech companies are having a hard time these days, so is Bitcoin that dropped more than 40% from its all-time highs. Tesla is down more than 35% from its all-time highs too.

Usually, the tech industry is hit hard when corrections come.

Some concerns about oil distribution and inflation made investors take some conservative positions, and leverage speculators are in a selling position while they’re hitten hard.

For long-time investors like me, it’s a buying opportunity.

Yet, I’m going to be honest with you. Last month I wrote an article where I shared why I sold 90% of my portfolio. The financial world is changing dramatically. And after this Covid-19 recovery and things getting to normal, I’m a little concerned about inflation and the bond market.

So, for now, I prefer to watch the game in the comfort of my home, with cash in my pocket, and just buying small portions of Bitcoin and Ethereum every month, but not stocks.

However, astonishing news came this week that will boost the Bitcoin network.

Discontent is the catalyst for change.

Life expectancy is proportional to age- that’s what The Lindy Effect explains.

The Lindy effect proposes that the longer a period something has survived to exist or be used in the present, it is also likely to have a longer remaining life expectancy. Longevity implies a resistance to change, obsolescence, or competition and greater odds of continued existence into the future.- wikipedia.org

One of the best examples is gold. Gold has been around us for more than 5,000 years, and because it has survived as a hard asset for so long, it remains a solid safe haven for the humanity.

Bitcoin has been around only for 12 years. And because of that, it’s a younger survivor. But every year that passes, this digital asset keeps getting more robust and resistant to competition and has more odds of continuing its existence into the future.

Technological revolutions come in cycles. And for these technologies to thrive, they need infrastructures.

Yet, at the beginning of a disruptive era, there is too much innovation for few infrastructures. Meaning, for example, with the car revolution in the 1900s, suddenly there were more than 100 car companies producing vehicles, but there were no roads for them to drive, neither gas stations for them to fill their tanks.

There were no infrastructures to support that new technology.

So, in 1908 there were 253 automobile manufacturers, but it dropped to 44 in 1929.

With the Internet, the same happened. In the 90s, massive innovative companies arrived, with promises of a gigantic revolution, but the system’s speed was slow, the e-commerce was nonexistent, and because of that, the tech bubble burst.

Look what happened to companies like Amazon, Microsoft, or Apple after passing The Lindy Effect and getting matured?

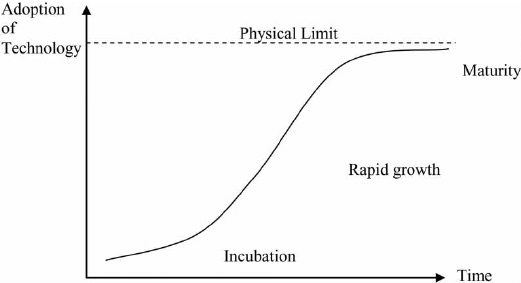

All technologies follow what’s known as the S-curve of diffusion.

The S-curve can also be used to depict the diffusion of innovations in a culture over time. First described by Everett Rogers in the early 1960s, diffusion is the process by which an innovation is communicated and taken up over time.- open.edu

The Bitcoin network is doing its trajectory into a mature technology.

Historically, the Bitcoin has been growing at a 198.72% compounded annual growth rate for the last ten years. If you compare to gold (1.97%), the S&P500 (11.22%), Nasdaq (16.94%), Long Dated US Treasury (4.58%), Amazon (33.5%), or even Tesla (63.8%), obviously nothing is compared with the Bitcoin.

About the S-curve, I believe we’re still between the Incubation phase and the Rapid Growth phase.

Some of the S&P500 companies and funds have already started to buy Bitcoin for their balance sheets. Microstrategy, Tesla, Square, or Ark Invest are the most popular ones. But companies like Palantir are considering holding Bitcoin on their balance sheet too. So, the longer the Bitcoin network proves its resilience, the bigger the adoption.

Infrastructure is the foundation of economic development.

After demand, new technologies need infrastructures to get access and ease of use to a large group of people.

New technologies also need regulation and mandates, meaning, if funds and financial institutions want to buy Bitcoin for their balance sheets, they have to have mandatory instruments that allow them to do so.

Also, about custody- with multi-billion dollar funds, who’s going to secure their wallets? For you and me, we can and should secure our private keys in cold wallets, but funds and institutions need another kind of infrastructure to do so.

Even Tesla recently sold 272 million dollars of Bitcoin to prove the liquidity of Bitcoin as an alternative to holding cash on their balance sheet.

Significant infrastructure is coming.

In a recent announcement, crypto custody firm NYDIG made public that Bitcoin is coming to hundreds of US banks this year.

The company, a subsidiary of $10 billion New York-based asset manager Stone Ridge, has partnered with fintech giant Fidelity National Information Services to enable US banks to offer bitcoin in coming months, according to the two firms.- cnbc.com

The banking industry is eager for Bitcoin because they can see their customers sending dollars to Coinbase, Binance, and other crypto exchanges.

So, shortly, you and I will be able to have in our bank apps, next to other banking deposits and savings, also cryptocurrencies.

What we’re doing is making it simple for everyday Americans and corporations to be able to buy bitcoin through their existing bank relationships,” Sells said. “If I’m using my mobile application to do all of my banking, now I have the ability to buy, sell and hold bitcoin.- Patrick Sells, head of bank solutions at NYDIG

The ordinary citizen will start to understand when they’ll access the Bitcoin network the basic concept of debasement currency. Meaning, they will get access to a financial tool, the Bitcoin and crypto network, that will balance the increasing loss of purchasing power that the western world has been seeing, with an unprecedented political strategy of printing dollars and euros.

The Bitcoin network provides each individual more financial sovereignty, putting pressure on central banks and governments to manage debt better, but also to provide a more efficient and egalitarian system.

NYDIG plans on other services, including debit card rewards paid in bitcoin and a new type of bank account called Federal Deposit Insurance Corporation (FDIC) insured but pays interest in bitcoin.- Hugh Son from cnbc.com

Bitcoin inside the banking system and secured by the FDIC, a governmental institution, means the regulation is taking place, and the US government is embracing the Bitcoin network.

Final Thoughts

The Bitcoin network is working like a black hole. Because it’s a finite hard asset and a digital invention, it will eventually suck all the old financial systems into a new layer, the blockchain.

Bridgewater CFO Dalby Leaving for Bitcoin Services Firm.- bloomberg.com

News like this, with valuable human resources migrating to the Bitcoin network, will be more frequent because the new financial system is faster, more efficient, cheaper, and creates individual sovereignty. And those who have jobs in the old financial system have already identified the main differences between the two systems.

Every individual who will access the Bitcoin network and the blockchain will use a system that doesn’t manipulate their time, money, and energy.

You can read the brilliant work of Robert Breedlove about the sovereign individual, or Michael Saylor, Jeff Booth, and Preston Pysh, about the genuine concept of money, time, and energy.

If you’d look at a photo of the 5th avenue in the year 1910, you’d see dozens of horses and one single car. Thirteen years later, in 1923, in the same place, another photo would show you a single horse and dozens of vehicles.

It took only thirteen years for New York to go from an all-horse to an all-car landscape.

This example is the very definition of technology disruption.

And after the digitization of the front stores by Amazon, the social network by Facebook, the mobile devices by Apple, and the electric vehicles by Tesla, the Bitcoin and the blockchain are disrupting the financial industry.

Most recently, Li Bo, deputy governor of the People’s Bank of China (PBOC), called Bitcoin an “investment alternative.” Although, this week, China warned investors against speculative crypto trading, and Beijing banned banks and payment firms from providing services related to cryptocurrency transactions.

In these turbulent times, where governments want to take precautions to keep control of their currencies and keep the economy stable, the technological pressure of the Bitcoin network is forcing everyone, with no exceptions, to regulate, embrace, and keep the pace to make this innovation a tool to serve us all, globally.

This article presents my own learnings based on personal experience. It should not be considered Financial or Legal Advice. Consult a financial professional before making any major financial decisions.

Sign up for my email list and join the happiest readers on Medium. (This is where you get exclusive access to my daily activities, experiences, and daily thoughts)