Full Analysis: 54-year-old Couple Wants $12k/mo. in 10 Years & $5M Tax-free to Their Kids

(be sure to checkout the video of this analysis too)

Retirement Goals:

1. Retire in 10 years with $12,000 per month of fixed, guaranteed monthly retirement income

2. Protecting your wealth & creating a tax-free wealth transfer strategy

3. Risk averse — ensure that some of your money is not susceptible the volatility of the market (i.e. safe money)

Financial Info:

Total Retirement Assets = $1,263,000 (not including home equity)

Retirement Asset Breakdown: $183k current 401k (maxing out annually), $438k old 401k #1, $250k old 401k #2, 7k Fidelity IRA, $22k Ameriprise cash, $28k Roth IRA, $65k wife’s IRA, $270k Riversource Variable Universal Life Insurance

Other Assets: social security, home equity (approx. $800k)

Estimated Future Retirement Values: 1,263,000 @ 6% per year = $2,261,000 projected @ retirement (10 years)

($757,800) — income annuity contribution today (see Retirement Income Analysis below)

Leaves Approximately $1,317,906 remaining retirement assets non-annuity in 10 years to spend flexibly

Summary of Safe Money Strategies:

Typically, you want what your age is in “safe money”, or money not tied to the ups-and-downs of the market. So, for example, when you turn 60 years old, you should have about 60% of your money somewhere safe, and about 40% can remain in the market.

1. Indexed, Income Annuity — designed specifically to provide maximum, guaranteed, lifetime income

o Does provide a small amount of growth if the market does well with no risk of loss, but the primary purpose is income generation

o Note: (see Retirement Income Analysis below for recommendations)

2. Indexed, Growth Annuity — designed to allow you to participate in the growth of the market with no risk of losing money if the market goes down

o Not at all designed to provide income, only risk-free growth of your investment

3. Short-term, Fixed Annuity — provides a fixed, guaranteed interest payment annual for whatever period you select (1-year, 3-year, 10-year, etc).

o Just like a CD, just issued by an insurance company rather than a bank

4. Indexed, Universal Life Insurance — designed for either supplemental tax-free retirement income, long-term care protection (without giving up accessibility), or as a way to transfer maximum tax-free wealth to your loved ones, while allowing you to leverage your remaining assets for your own retirement

o Note: (see Tax-free Wealth Transfer Strategy below for recommendations)

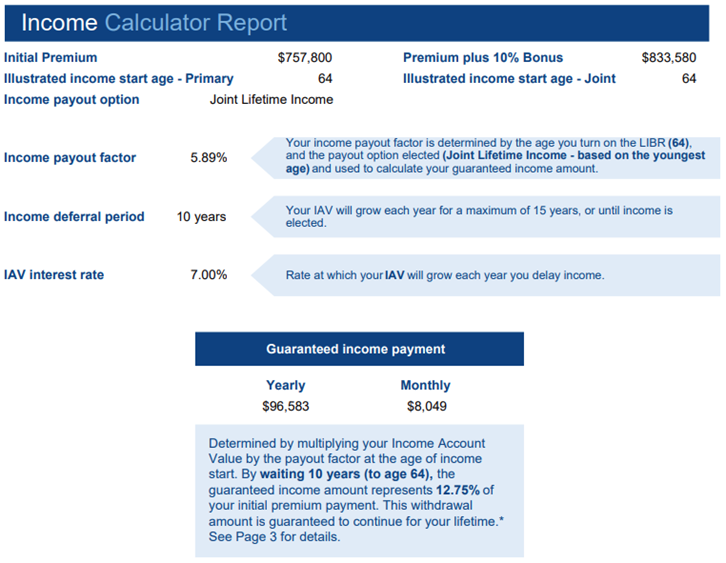

Retirement Income Analysis — Using an Indexed, Income Annuity to create maximum retirement income:

· Using approximately 60% percentage of your current retirement assets to fixed, guaranteed, future income ($757,800)

Highlights of using an income annuity vs. the market for income:

o Safe money not susceptible to fluctuations of the market (+ guaranteed growth)

o Eliminates the sequence-of-return risk for your retirement income (your retirement income is unaffected by what happens in the market now)

o Generates about 47% more income than you can from the market with the 4% rule

o Eliminates the possibility of running out of money in retirement (guaranteed lifetime income)

o Allows much more freedom & flexibility with your remaining assets

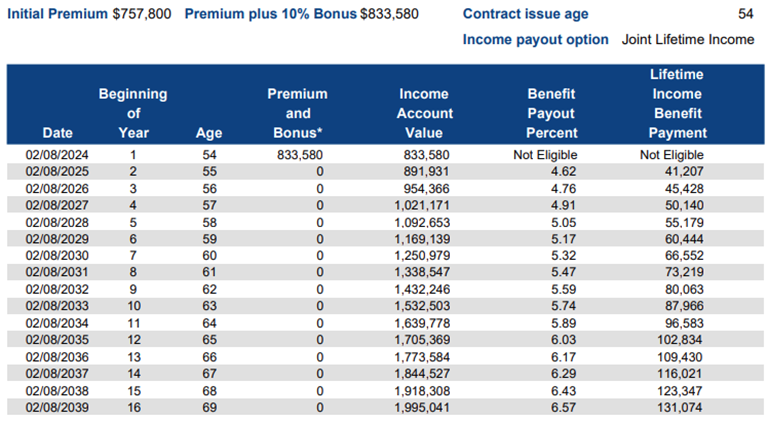

Income Schedule (you decide when to turn the income on):

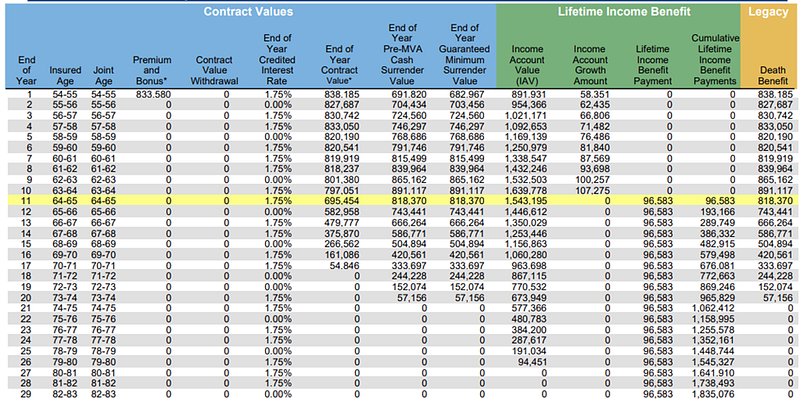

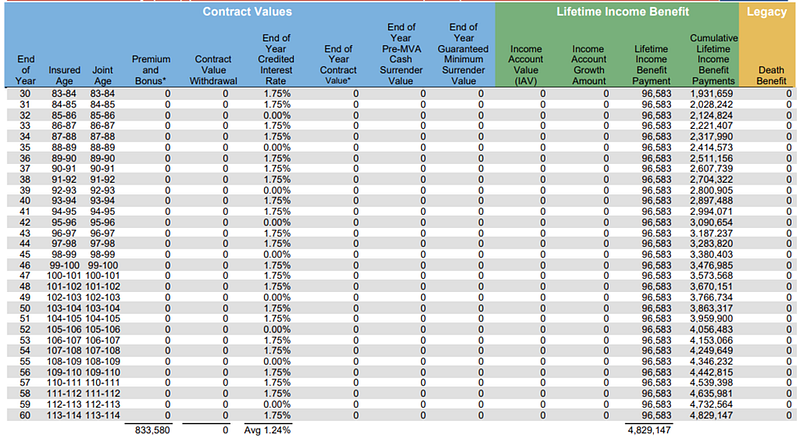

Residual Value of this contract (never less than you put in):

· Review the cumulative income payments received at age 85 (above)

o $2,124,824 received vs. an initial contribution of $757,800 (+ income is still guaranteed)

· Long-term Care Supplement: You can add supplemental long-term care coverage for an annual cost of 0.1% (doesn’t affect the income of this annuity)

o This will double your income value for up to 5 years (with a 2-year waiting period)

Retirement Income Results in 10 years

$8,049/month (income annuity) + $6,100/month (social security) = $14,149/month (guaranteed for life)

Note: you will also have a projected $1,317,906 of additional retirement funds in 10 years that can be used to create additional income, to spend flexibly in retirement, or to reposition for a Tax-free Wealth Transfer (see below).

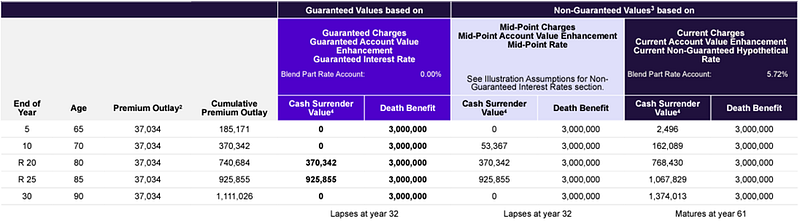

Tax-free Wealth Transfer Strategy

· Example of a $3,000,000 Tax-free Legacy Policy (for a 60-year-old)

o Currently putting $1,219/month into a variable universal life policy that could be redirected as part of a future tax-free wealth transfer strategy, also allowing you to reduce the overall amount of term insurance you have & ensure that you are protecting future wealth for your girls (and giving them all tax-free money)

My Recommendations:

· Approximately $757,800 to an indexed, income annuity based on Retirement Income Analysis for future, guaranteed income (bringing your total income to $14,149/month, guaranteed for life)

· Rollover the Variable Universal Life cash-value into a low-expense, universal life policy based on Tax-free Wealth Transfer Strategy (above)

o Redirect the $1,200/month premiums to the new policy to reposition more money for a tax-free transfer of wealth

o Take the additional $2,149/month of income beyond their income goal & reposition that for a tax-free transfer of wealth

o This will produce somewhere between $4–5 million dollars of tax-free money to leave for your girls

Connect With Me & Access All My Resources Here

Enjoy this blog? You’ll probably enjoy this one as well: 56-year-old Wants $7,000/month of EXTRA income @ 64 (+fully-funded tax-free retirement)

To your success,

Matt